It’s a truism that as the U.S. consumer goes, so goes the economy. And consumers are still opening their wallets and purses, tapping to pay, clicking to pay, swiping their cards; by extension, gross domestic product continues its upward trajectory, though at a pace slowing from previous readings.

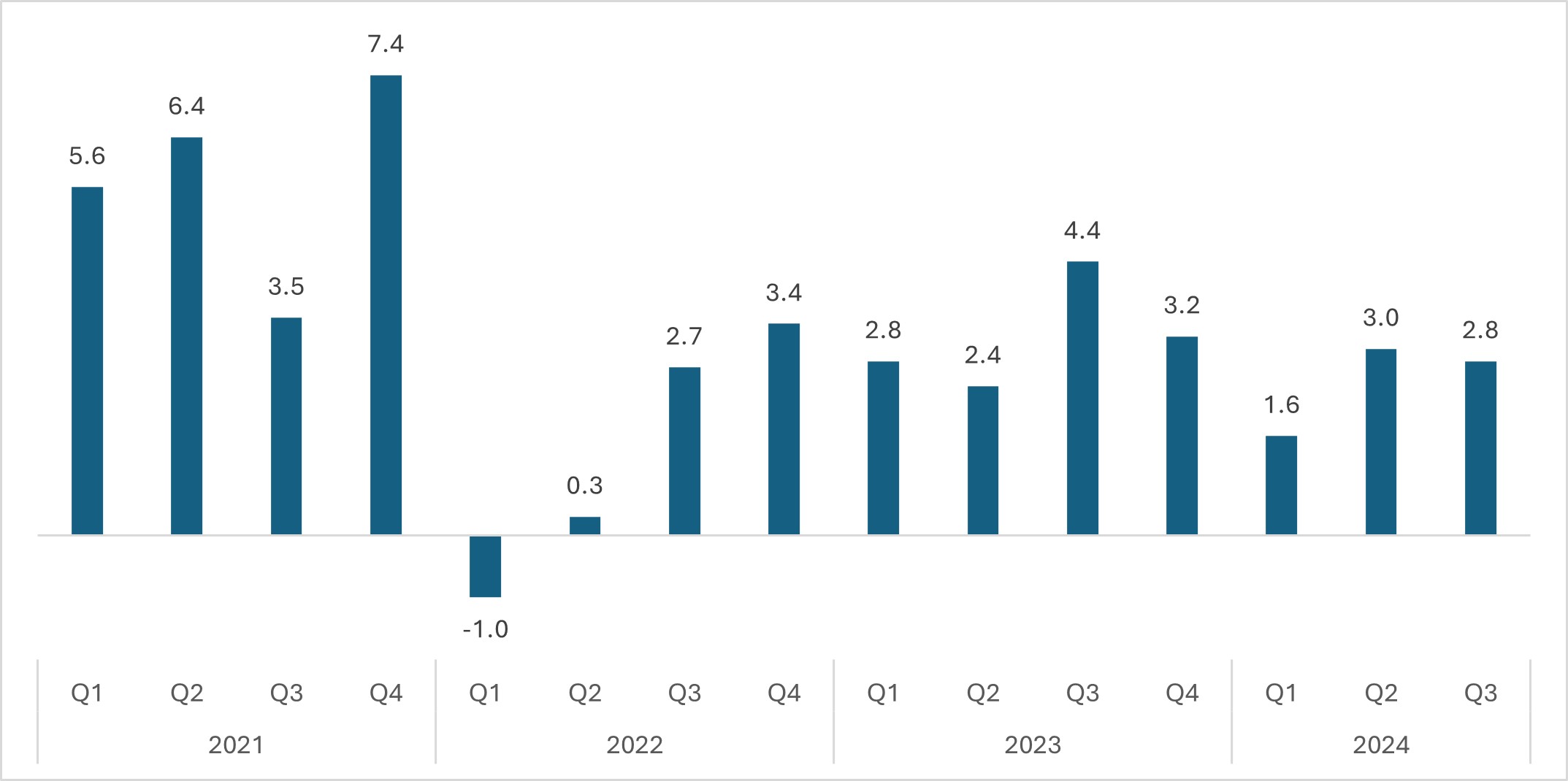

The Commerce Department’s Bureau of Economic Analysis said on Wednesday that GDP expanded at a 2.8% pace, as measured in preliminary results for the third quarter. That’s a slowdown, a bit, from the 3% pace seen in the second quarter.

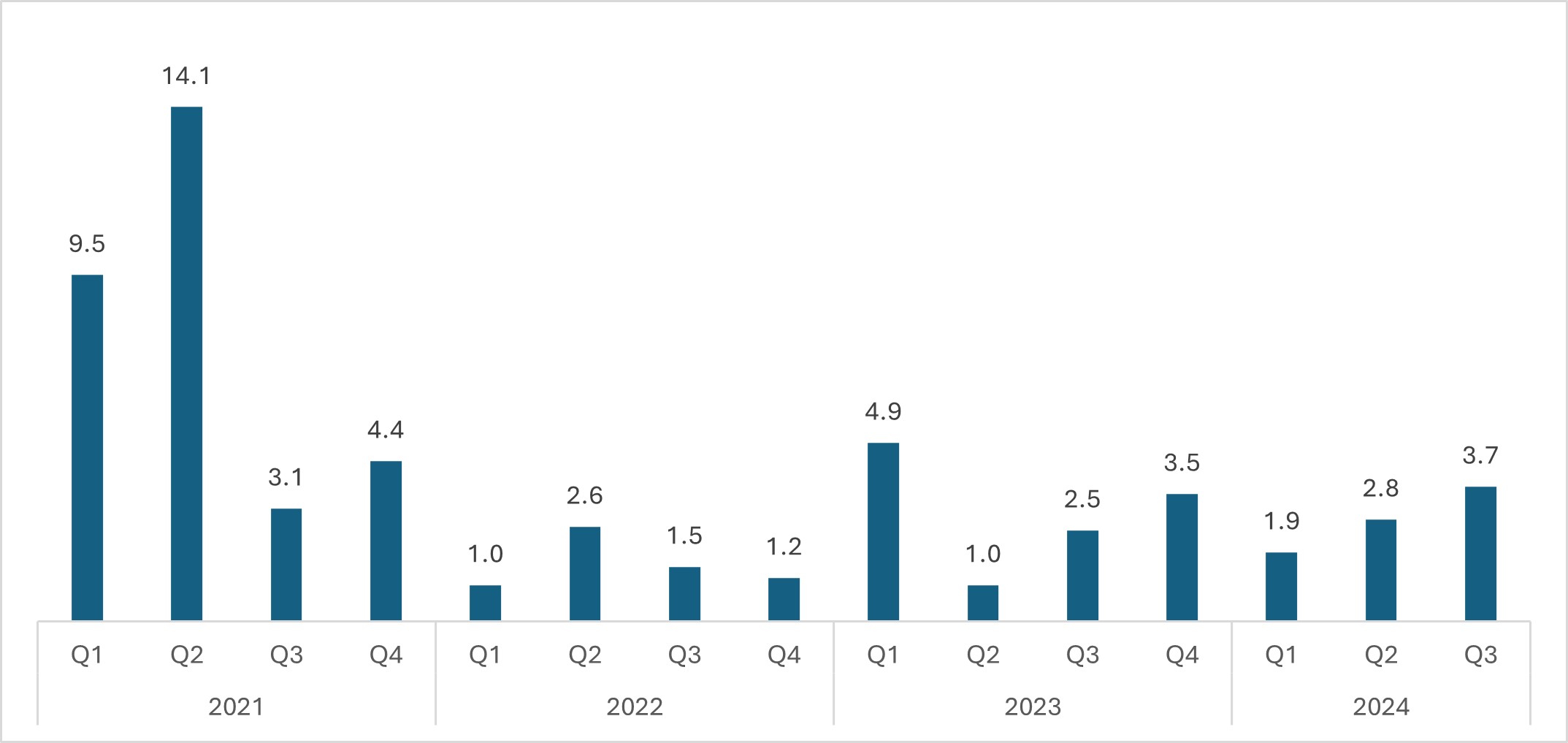

Consumer spending grew at a 3.7% pace, adjusted for inflation, while prices were up 1.5% on an annualized basis. Consumer spending accounts for two-thirds of GDP. Consumer expenditures rose across nondurable goods, notably in prescription drugs, and services, with notable spending on healthcare and accommodations.

Source: Bureau of Economic Analysis

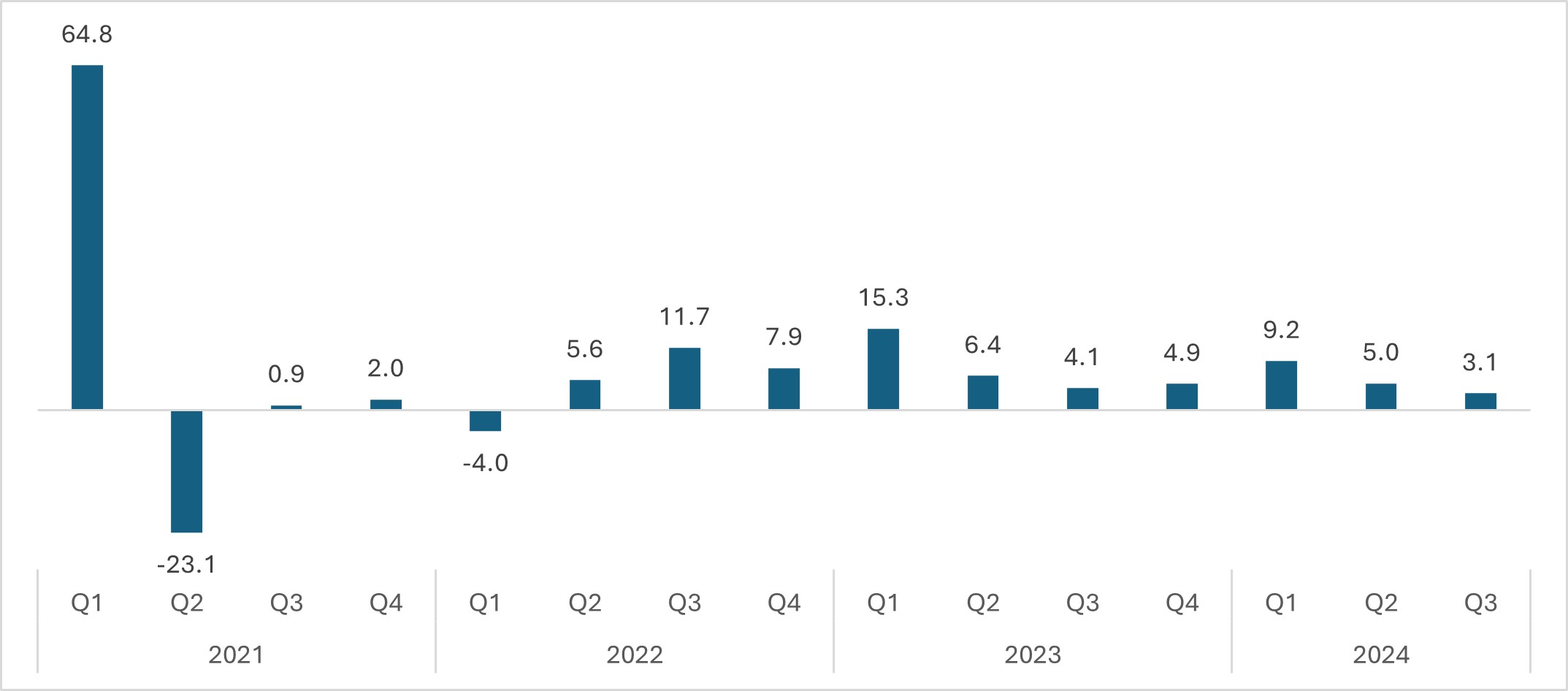

Source: Bureau of Economic AnalysisAt the same time, the third quarter report offered evidence that personal income growth slowed, with disposable income rising by 3.1% compared to 5% gains in the second quarter. The personal savings rate dropped slightly to 4.8%.

Once again, out of the subitems that comprise the index, it was services (including housing and utilities, healthcare and transportation) which drove the bulk of the increase, at a 3% annualized rate.

All in all, PYMNTS Intelligence finds that the latest data reflects a stable but cautious economic environment amid GDP growth. Consumer spending remains a crucial growth driver, yet the decline in disposable income growth and the savings rate may signal future constraints on spending capacity.

Separate PYMNTS Intelligence data indicate that as of September — right as the quarter was ending — a full 66% of consumers lived paycheck to paycheck, up 3% from a year ago. Savings might help supplement slowing disposable income, but as savings rates dip a bit, replenishing those cash coffers takes time. The latest paycheck-to-paycheck-related data have detailed that consumers who struggle to pay their monthly bills find ways to hold on to the savings they have. In fact, struggling paycheck-to-paycheck consumers average $2,447 in savings, while those living without difficulty average $7,558.

But there are also some mixed signals coming out of earnings season. By and large, most of the payment networks and the banks have noted that consumer spending is resilient overall. But there are some pockets of volatility. In one example, Synchrony CEO Brian Doubles said “both new accounts and purchase volume growth continued to be impacted by a modest pullback in consumer spending,” adding that “our customers continue to be discerning in our discretionary purchases.” Discover Financial Services’ management has observed, as well, that as payments volumes were down by the low single digits, year over year, “cautious consumer behavior” has been observed.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More