The question is: Was the decline in revolving credit (such as credit cards) and nonrevolving lines (fixed-term loans like auto loans), heading into the holiday season, a sign of things to come, when consumers will trim balances?

Or was it simply a pause that refreshed some spending power (on the cards, we mean — overall spending at retailers was up 0.7% in November, as noted here) as the season of gift giving alighted full force into the final weeks of the year?

PYMNTS Intelligence has reported through the past few months a bit of a shift: Consumers have been moving toward installment options, which include card-linked installments and buy now, pay later plans. And elsewhere, in a recent “Paycheck-to-Paycheck” report, as of last fall, 75% of consumers carried at least some card debt.

The entire sample, across income levels, financial profiles (whether they lived paycheck to paycheck, for example, or not), carried card debt of more than $5,000, on average. Households living paycheck to paycheck, with issues paying bills, held even more credit card debt, at $7,000.

Revolving Debt’s Decline

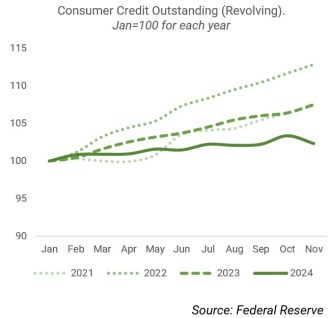

The Fed’s data, released Wednesday (Jan. 8), showed that overall credit fell at a seasonally adjusted annual rate of 1.8%. Revolving credit saw a 12% decline (the strongest slide of the post-COVID era) while nonrevolving lines grew at an annualized 2%. This means that overall borrowing across all lending tranches was negative at $7.5 billion in October, with nearly $14 billion in outflows from revolving lines.

Advertisement: Scroll to Continue

This nearly offsets the $17 billion revised uptick in October, when revolving lending grew by $15 billion on seasonally adjusted terms.

The dip in revolving balances relative to a month prior is the steepest in 50 months (balances fell by 12.5% in August 2020) and constitutes the third decrease of the year.

A seemingly straightforward explanation for the lackluster performance of borrowing throughout 2024 is the unusually high cost of borrowing. The estimated average APR across credit card plans stood in November at 21.4%, down a bit from rates than had been seen at the end of the third quarter of this year.

Those rates are well above the mid-teens percentage points seen before the pandemic. A similar situation is evidenced with personal loans, with the average interest rate for 24-month loans standing at 12.3% versus the 2023 average of 11.8%.

Against that backdrop, the decline in outstanding balances means that paying down debt, at least variable rate debt, had become a priority for consumers. Price sensitivity also should not be ruled out — higher interest rates have made debt more expensive even when paying for items and services that have yet to fully shake off the impact of lingering inflation, as interest rate cuts take time to fully impact the economy.

The trimming of revolving credit debt, including the cards, in November was notable, but we’ll see whether it was a blip or a trend a month from now, when December’s data comes out via the next Fed report.