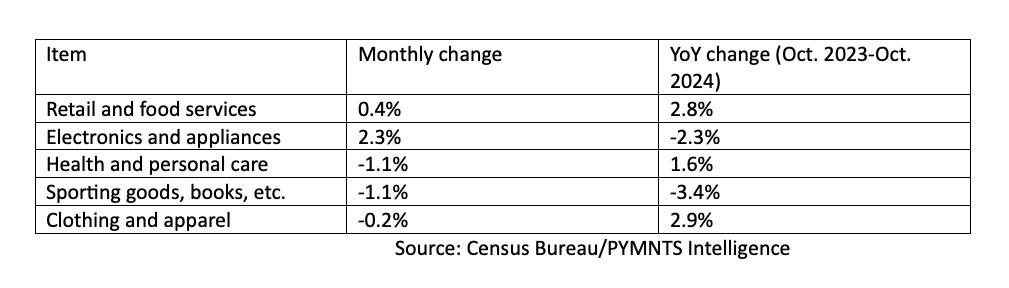

October retail sales were up 0.4%, according to data from the U.S. Census Bureau.

Although U.S. consumers keep opening their wallets, auto-related sales boosted results, while some key categories of discretionary spending dipped. Online sales slowed, indicating a potential lull before the holiday shopping season begins.

The data pointed to flagging momentum — at least temporarily. Spending on automobiles and parts surged by 1.6% while spending on electronics and appliances gained 2.3%. Spending on building materials and garden-related items gathered 0.5%. These are, arguably, big-ticket items.

The data (adjusted for seasonal variation but not price changes), represented a slowing from the now-upwardly revised retail sales gain of 0.8% in September.

As for discretionary spending, categories that slipped month over month were sporting goods, hobby, musical instrument and book stores, as well as health and personal care — by 1.1% each. Spending on apparel was down by 0.2%.

Non-store retailers, a category generally used as a shorthand designation for online retail (although it is not limited to that group of merchants and platforms) saw sales grow by 0.3% month over month, down from the 1.7% leap seen in September versus August.

November’s data will mark a critical point for retailers, as we’re only a few weeks away from Thanksgiving, Black Friday and a likely relentless pace of promotions that will determine whether consumers are ready, willing and able to keep spending. Cyber Monday falls on Dec. 2 this year, so sales that day will be included with December’s data.

Consumers are optimistic about what’s on the horizon, as detailed by The Conference Board’s latest reading of its Consumer Confidence Index. Headed into last week’s elections, the overall reading of the index surged to 138 for current conditions, up from 99.2 in September. That’s the biggest leap since March 2021.

The “expectations” index of future conditions was up 8% to 89.1

At the same time, The Conference Board said the share of consumers expecting higher interest rates over the next 12 months increased to 47.5% after declining for four consecutive months. Average 12-month inflation expectations rose to 5.3% in October from 5.2% in September, as food and services prices continued to increase.

Separate data this week from the Federal Reserve, in its own survey of consumer expectations, showed that consumers see inflation easing from previous estimates. Looking ahead one year, they see inflation touching 2.9%, where the previous pace was thought to be 3%. Three years out, they expect inflation to fall to 2.5%, down from the previous 2.7%.

Overall spending over the one-year timeframe was unchanged at 4.9%, which would leave an implied gap of about 1.9% when measured against the 3% estimate of wage growth.

Credit has been a lifeline, and the November PYMMTS Intelligence report “Average Credit Debt Hits More Than $7,000 for Financially Struggling Cardholders” showed that balances on credit cards are still on the rise, particularly among paycheck-to-paycheck consumers, which make up about two-thirds of the population.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More