The pandemic has markedly accelerated the move to online shopping, with a PYMNTS report indicating that 47 percent of U.S. consumers living in urban areas have shifted to digital rather than brick-and-mortar retail shopping.

It also identified a sharp uptick in the number of consumers using digital wallets or other contactless payment options when they do venture into stores, with 64 percent of bridge millennials — consumers ages 33 to 43 — saying they use digital wallets and 24 percent reporting they use contactless credit or debit cards to make in-person payments, for example.

Merchants are being pulled along for this new payment ride, with many businesses working quickly to accommodate consumers’ shifting brick-and-mortar and eCommerce shopping preferences. Companies are thus carefully monitoring which payment methods and technologies are seeing increased adoption and popularity in both channels. One study found that 44 percent of small- to medium-sized businesses (SMBs) consider contactless or mobile payment support as integral to keeping customers satisfied, while 36 percent said the same about new methods, such as buy now, pay later (BNPL) tools.

Merchants must therefore determine how to support these payment methods with the speed and security necessary to keep customers engaged. Making use of numerous standard and emerging payment rails, including recently developed services like the RTP network, could allow savvy merchants to seamlessly accept the growing variety of payment methods consumers crave across every channel.

The following Deep Dive analyzes how the pandemic is affecting the spread and use of established and emerging payment rails, and it explores how connecting with these rails can give merchants key customer engagement and satisfaction benefits. It also examines how leveraging various rails can give these businesses the speed and security they need to compete both domestically and internationally.

Consumer Behavior And Payment Rails Usage

Connecting to one or more payment rails is typically the first step merchants take when setting up their businesses, so they may assume these offerings bear no closer examination. The vanishingly rare number of U.S. retailers that accept only cash are at a particularly steep competitive disadvantage, as debit and credit card payments had begun supplanting cash use even before the pandemic began.

Cash payments now represent just 28 percent of total U.S. transaction volume, for example, whereas they accounted for 51 percent in 2010. Carefully monitoring how their payment rails are working, however, could give merchants a leg up once the pandemic ends as consumers continue to experiment with payment methods that have moved beyond the scope of traditional plastic cards.

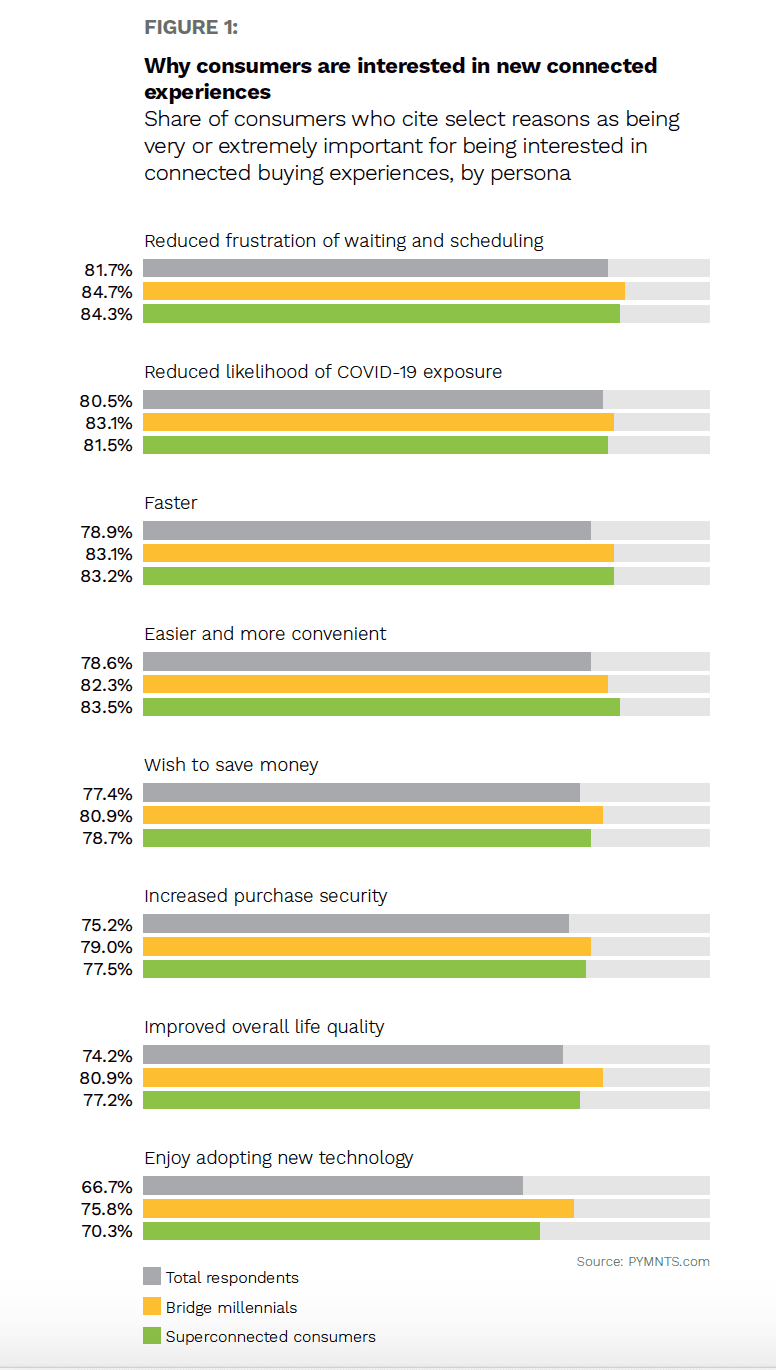

One PYMNTS study found that consumers are reporting greater overall interest in payments, with 75 percent of U.S. customers in large urban areas stating they determine which merchants to purchase from based on their digital payment offerings. These consumers also indicate much greater interest in a large variety of so-called connected payments experiences, which pair more familiar tools such as debit or credit cards with mobile applications or connected devices that enable users to pay both online and in stores. There are several reasons for this increased interest, including health or public safety concerns and the speed at which these transactions are finalized. Eighty-two percent of consumers in one PYMNTS study indicated that decreasing the frustrations attached to waiting for or scheduling payments was the main draw of connected experiences.

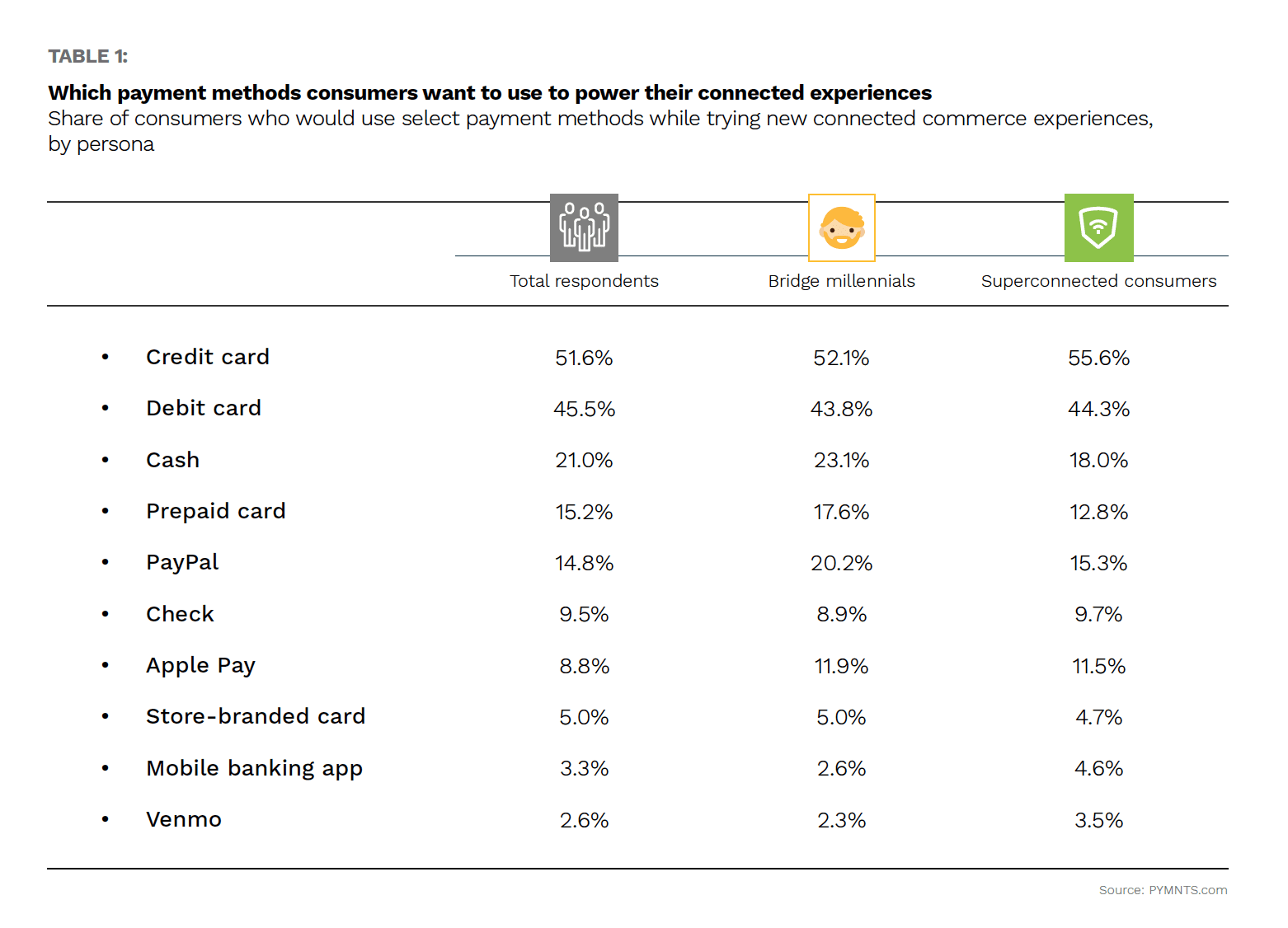

Multiple factors make it advantageous for merchants to stay abreast of consumers’ growing preferences for connected payments, especially in relation to how they dovetail with payment rail use. Consumers are looking to pair not only debit and credit cards with their connected devices but also digital wallets such as PayPal or peer-to-peer (P2P) mobile apps like Venmo. One PYMNTS study found that 15 percent of consumers want to leverage PayPal to power their connected payments, for example.

Most of these tools can currently connect to multiple credit payment rails as well as ACH or other networks that pull funds directly from customers’ accounts. That means consumers are already expecting their favored merchants to accept payments via these rails, making it essential for companies to examine how their rail usage is affecting customer satisfaction. Retailers must also stay informed on how payment rails themselves are changing as more consumers begin to expect their funds in real time.

The Future Of Real-Time Payment Rails

Real-time payments’ emergence has captured the payments industry’s attention, and the ongoing pandemic appears to be shedding even more light on how merchants can tap these networks to benefit their consumers. Customers are eager to use real-time payments for everything from retail purchases to bills, for example, with one study finding that more than 75 percent of U.S. consumers who are currently struggling to pay their bills would use real-time payments to make those transactions if such payments were available. Real-time payment networks are proliferating globally, and more than 40 countries are now developing rails for their own markets. The Federal Reserve and The Clearing House (TCH) are currently working on individual networks within the U.S., for example.

Keeping an eye on payment rail developments will prove essential for merchants once the pandemic has passed, especially as more and more consumers seek out real-time payment solutions. This new retail environment will ultimately require merchants to connect strategically with existing and emerging payment rails to keep consumers satisfied.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More