A survey of companies across Latin and North America found that more than half paid regulatory fines or otherwise suffered financially in the past year due to unmitigated compliance risks.

Between fines and fraud, which 71% reported experiencing issues with, respondents saw average profit losses of 1% in the last year. Sixty percent of companies surveyed expect greater compliance risk in the coming year, with anticipated regulatory increases attributing to much of this heightened risk. Forty-six percent of respondents expect greater compliance requirements related to labor, and 41% expect more aggressive regulatory enforcement across the board.

Even as companies expect compliance to become more challenging, just 22% said they follow international best practices for anti-money laundering (AML), and just 18% said the same about anti-corruption compliance. Fifty-five percent acknowledged fines or financial losses related to compliance violations in the past year, and 32% reported having gone through compliance-related investigations.

Forty-four percent of respondents said they believe their companies will increase compliance-related spending in the future, and their expectations surrounding increased requirements and more aggressive enforcement could influence that. More than 70% of companies surveyed said their corporate leaders respond to increased regulatory burdens and enforcement by paying greater attention to compliance, but upholding their reputations plays an even bigger role.

This month, PYMNTS examines the difficulties and costs of ensuring regulatory compliance when making disbursements and how working with third parties could help companies better mitigate risk.

Keeping Money Clean

In addition to combating fraud and other online retail security challenges, a report found that 80 institutions across the industry dealt with 2.5 billion euros ($2.5 billion) in AML fines in 2021. International sanctions can further complicate guarding against money laundering. As the list of sanctioned countries changes — or even as the level of sanctions changes — companies must remain aware of how this could alter when and where they do business to prevent exploitation by those wanting to avoid sanctions.

There are risks involved in failing to comply with regulations and legislation, but heavy-handed approaches meant to ensure compliance have their own financial risks. The monetary value of lost transactions due to false positives in 2021 was nearly four times the value of losses to direct fraud for those same companies.

Even companies that are well-versed in finance often struggle to stay compliant. Money laundering is one of the primary areas in which financial institutions (FIs) face backlash from regulatory bodies. Issues such as failing to provide proper governance or ensuring that the FI has collected all necessary information from individual or business clients can result in harsh penalties that may even include prison time.

Crossing Borders Without Crossing Regulations

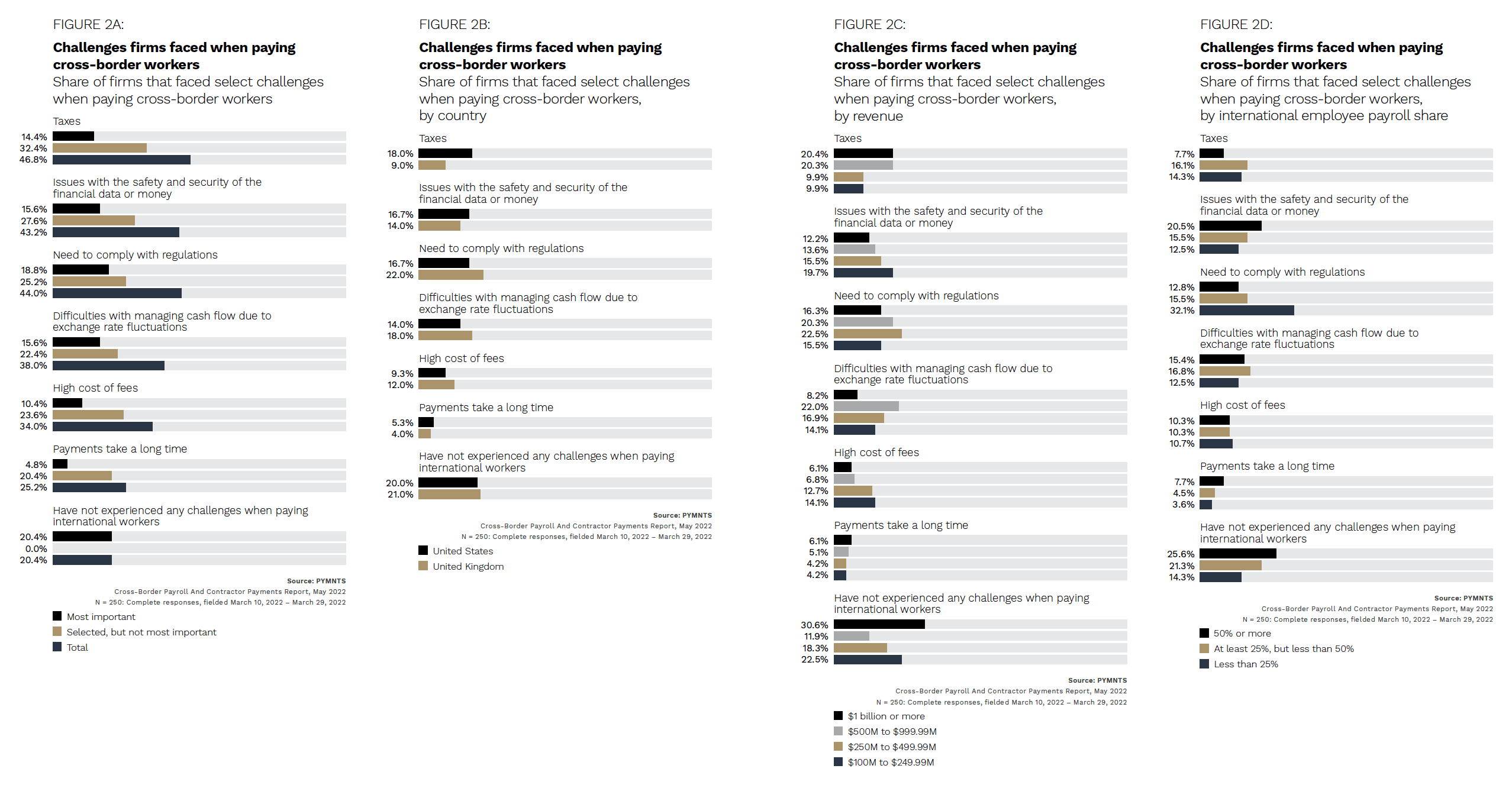

International trade complicates regulatory compliance for payroll as well. Nineteen percent of surveyed firms cited regulatory compliance as their most critical challenge when paying international workers. The less companies spend on international workers, the greater the challenge. Thirty-two percent of companies that spend less than one-quarter of their budgets on international workers said compliance is a critical issue, compared to just 12% of firms that spend 50% or more of their budgets on these employees. Managing payroll taxes and regulatory compliance when paying international workers figures just as large as fluctuating exchange rates and financial data security for these companies.

Among U.S. firms, 18% cited taxes as their biggest challenge for international payments — double the share of United Kingdom firms that said the same. This potentially indicates that firms that employ international workers are less likely to struggle with compliance. At the same time, 20% of firms generating revenues of more than $500 million said taxes were a challenge, compared to 10% of those generating less than $500 million.

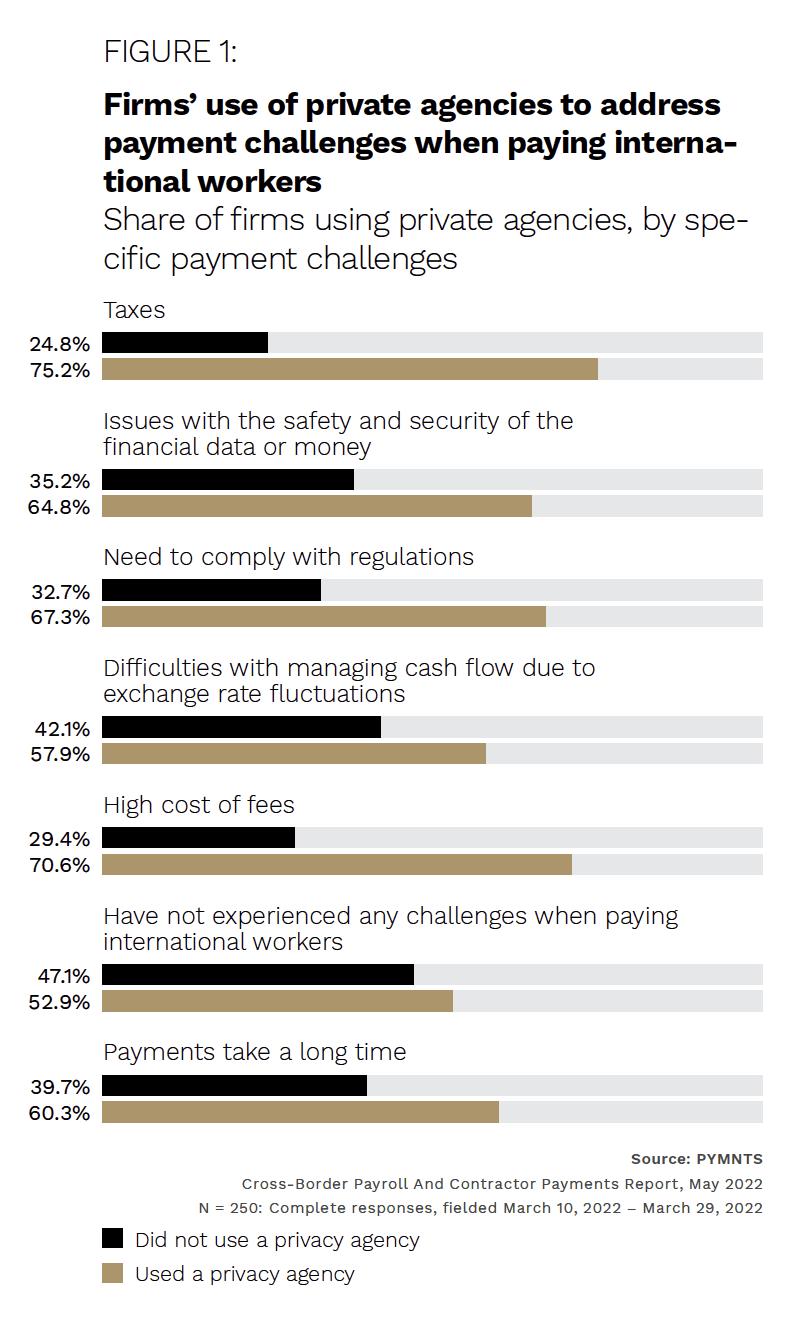

For many of these companies, the answer lies in working with third parties. Sixty-seven percent of companies using private agencies to ensure compliance said they had experienced challenges when paying international workers. Across the board, from taxes to regulatory compliance, companies that had experienced difficulties paying international workers were significantly more likely to turn to a private agency for help than those who had not.

Prepackaged Payment Solutions

Whether internationally or domestically disbursing funds, many firms are now turning to prepackaged solutions that address both the complexity of modern payment rails and the challenges of regulatory compliance. The right third-party application programming interfaces (APIs) enable true any-to-any transactions, such as transferring funds between customers’ accounts or paying third parties. They should also have fraud management and regulatory compliance features baked in. This not only saves firms time and money on development but also makes it easier to keep up with a payments landscape that changes almost daily.