As businesses seek cost reductions at a time of high inflation and with the COVID-19 recovery still very real and ongoing, more companies are looking to options like virtual cards.

For the study “Accelerating The Time To Realized Revenue: The Virtual Card Edition,” a PYMNTS and Mastercard collaboration, we surveyed 400 executives in the manufacturing, healthcare and transportation/logistics/shipping sectors in the U.S. and Canada, finding that as awareness of virtual cards spreads, so too does their adoption in a variety of industries and use cases.

The survey found that “businesses using virtual cards report a wide range of operational benefits, including lower transaction costs, tighter security, enhanced cash flow management and greater access to both rebates and credit,” and many partnering to get these benefits.

Get the study: Accelerating The Time To Realized Revenue: The Virtual Card Edition

File it under “what do they know that we don’t,” but our survey finds mid-market and larger firms using virtual cards to a greater degree than smaller competitors, and that’s worth a look.

We found this especially true in healthcare. As the study states, “Large-market healthcare firms are nearly twice as likely as their mid-market counterparts to use virtual cards to both make and receive B2B payments,” with 48% of large-market firms in the healthcare sector use virtual cards to make payments, and 52% using them to receive payments. By comparison, only 24% of mid-market firms use virtual cards for payments, though 27% use them for real-time payments.

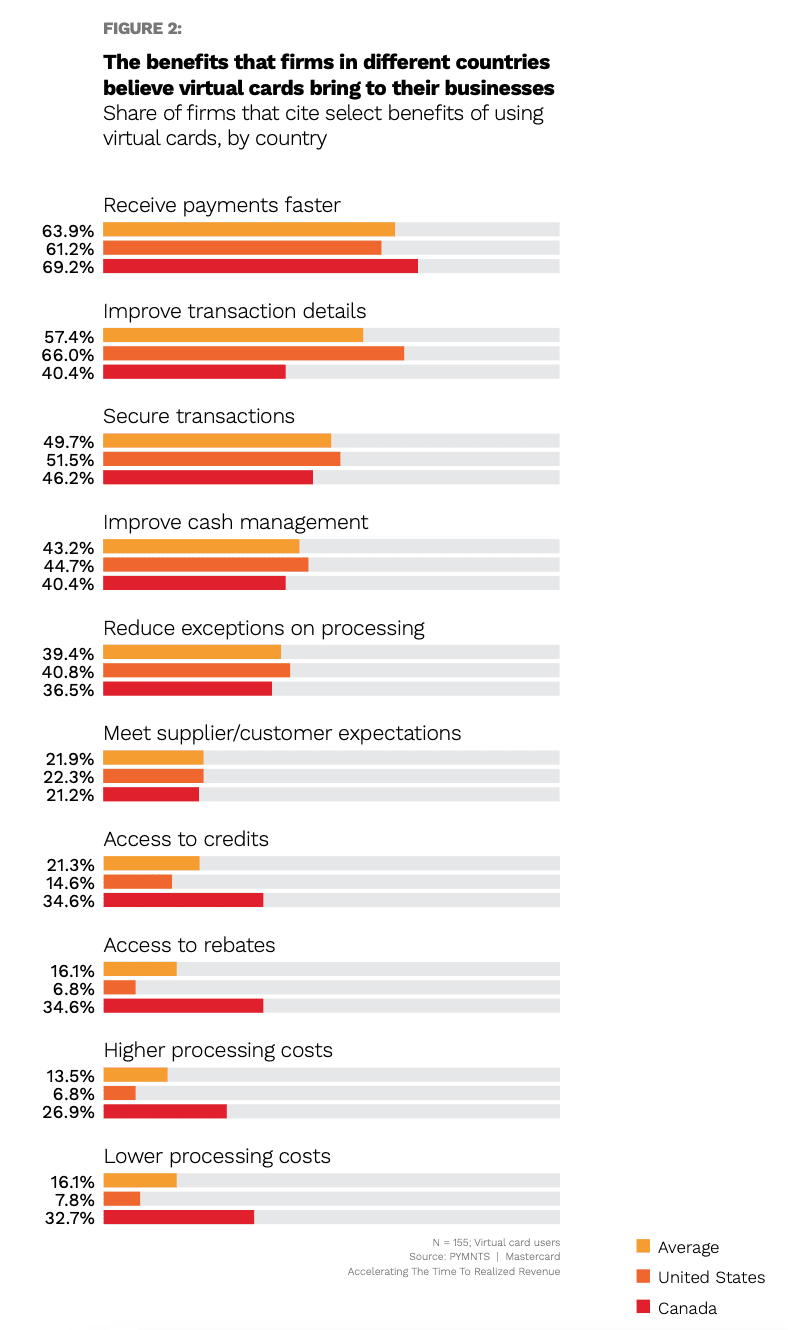

U.S. firms are further along in their adoption of virtual cards, making the gains of Canadian companies adopting the technology stand out even more with some staggering numbers.

Per the study, “Canadian firms that use virtual cards cite more benefits from using them than their counterparts in the U.S. They are 137% likelier to say they have benefited from increased access to credit and 409% likelier to say they have benefited from added rebates, for example. Canadian firms that use virtual cards to make payments are 319% likelier than U.S. firms to cite lower processing costs as a benefit.”

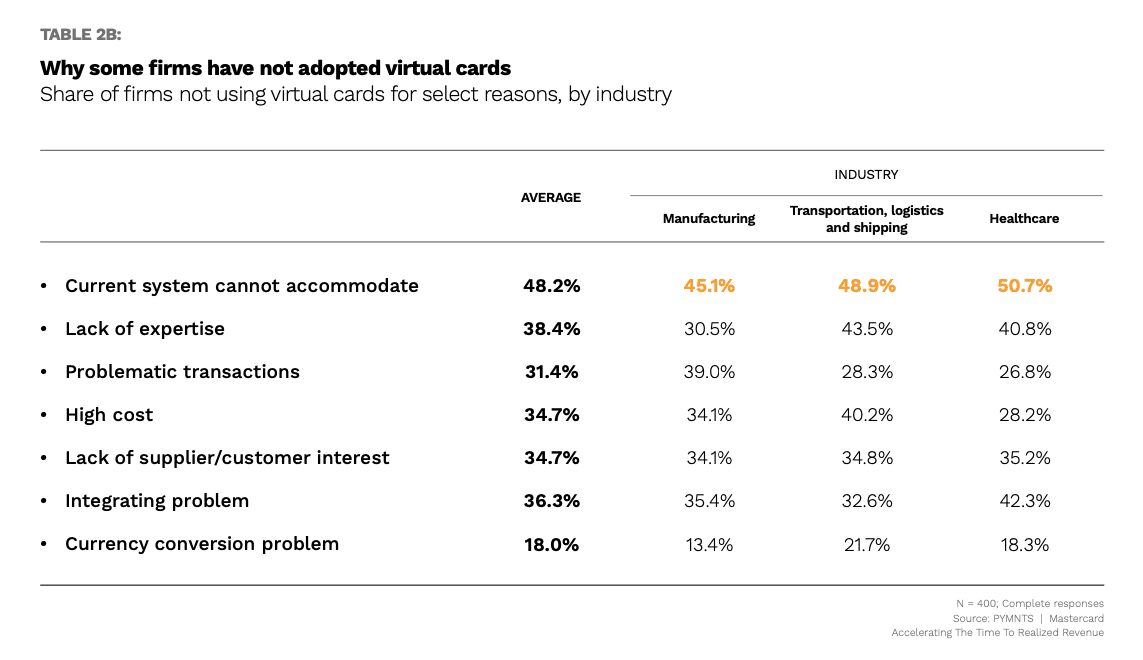

Our research identified the biggest obstacle to virtual card use as companies believing their payments processing infrastructure are not capable of handling this form factor.

However, the study notes, “Businesses can often address these barriers by enlisting help from third-party providers. Outsourcing virtual card operations to trusted third parties can not only grant businesses access to the subject matter expertise they are lacking in-house, but these vendors can also work with businesses to find solutions compatible with IT systems.”

Get your copy: Accelerating The Time To Realized Revenue: The Virtual Card Edition