Consumers are leaning on credit monitoring features to manage their finances — and they may switch providers for these tools.

Inflation may be slowing down somewhat, but consumers are still scraping by as the cost of essentials such as groceries remains 7.1% higher than a year ago. In an effort to manage spending that in some cases is outpacing personal resources, some are seeking out tools to better monitor their finances. One feature consumers are using is their credit card’s monitoring features, as illustrated in PYMNTS’ collaboration with Elan Credit Card, “Credit Card Use During Economic Turbulence.”

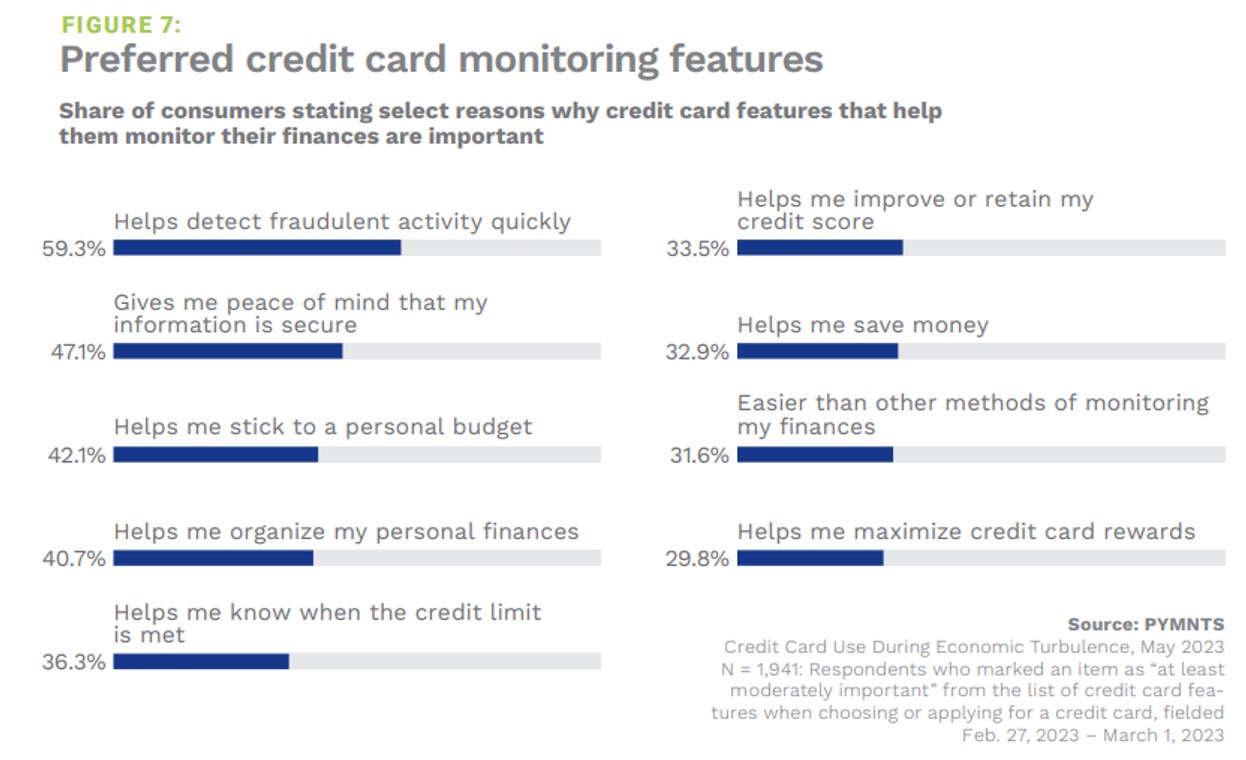

Although consumers rate fraud monitoring as the most important of the selected features they seek out in a card, more than a 30% share of consumers marked each of the six options that directly involve financial wellness as “at least moderately important.” Clearly, this widespread popularity indicates there is a desire — perhaps bordering on a need — for these budgeting and money management tools to help consumers navigate the rocky economic landscape.

Providing these tools presents an opportunity for card-issuing financial institutions (FIs), which may be seeing spend drop off as consumers rein in charging to avoid rising percentage rates. Indeed, previous PYMNTS’ research finds that personalized financial wellness tools appeal strongly to Gen Z and millennial consumers seeking digital-first methods of building and managing their wealth. For 29% of consumers overall, interest in these innovative products is enough for them to switch or consider switching FIs. In this way, this isn’t just an opportunity: it’s a customer mandate, and issuers must take notice or risk their base.

In an interview with PYMNTS, Ali Niknam, CEO of Amsterdam-based neobank Bunq, explained how the need for FIs to provide customers with budgeting tools has never been greater. This is because for some, money only monitored electronically may be harder to track than physical cash.

“Digital money just doesn’t have the same feel to it as physical money,” he said. “We’ve been trying to re-create that same type of experience digitally [and have] always expanded on ways to make [money] more tangible and more intuitive.”

Card-issuing institutions scrambling for share of consumer spend may want to consider offering, and promoting, budget monitoring features. Otherwise, they may see their customers searching for providers that do.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More