This week, Mastercard and Visa reached a multi-billion dollar settlement that may bring an end to 20-year legal battle between the two financial giants and merchants.

Merchants have long complained that the two card companies charge them excessive interchange or “swipe” fees when customers pay for purchases with cards. If the judge approves the proposed settlement, Visa and Mastercard will reduce those fees and cap them for five years — a move that will reportedly save merchants an estimated $30 billion.

Some trade groups said the settlement was a step in the right direction. The National Federation of Independent Business (NFIB) issued a statement saying that while the settlement will “provide a limited amount of short-term relief to small businesses, it does not solve the long-term anti-competitive rate-setting practices that are the root of this problem.”

One aspect of the settlement that has captured less attention is how it might impact card users. As CPI, a PYMNTS company, noted this week, “fees play a pivotal role in funding credit card rewards programs, including cash back incentives, travel points or miles, as well as purchase protection and trip insurance.”

If the two card companies agree to scale back on interchange fees, it may degrade existing credit card reward programs — programs that are popular with both consumers and small business owners.

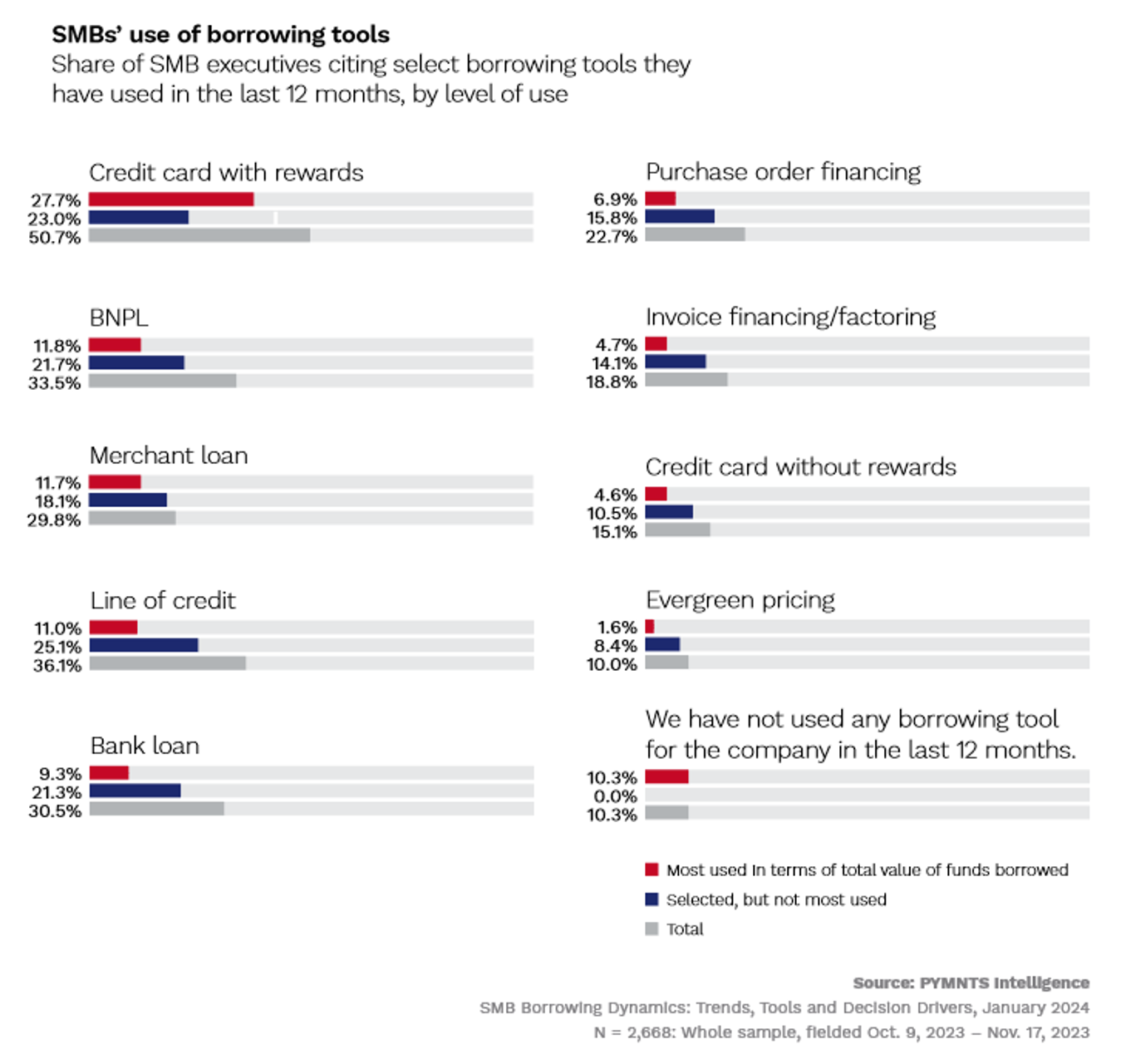

According to “SMB Borrowing Dynamics: Trends, Tools and Decision Drivers,” a PYMNTS Intelligence report completed in collaboration with U.S. Bank, reward-earning credit cards are the borrowing tool of choice for many small and medium-sized businesses (SMBs) needing short-term capital.

The report, which draws on insights from more than 2,600 U.S.-based SMB executives, found 51% of respondents in need of flexible funding options turn to credit cards offering rewards. And for 28% of them, reward-earning credit cards are the primary source of that short-term funding.

As the accompanying chart illustrates, the popularity of reward-earning cards surpassed other borrowing options over a 12-month period. Those other options include buy now, pay later (BNPL), which was used by 34% of SMB executives; merchant loans (30%), lines of credit (37%), bank loans (31%) and — most significantly — non-reward earning credit cards, which were used by only 15% of surveyed executives.

The preference for reward-earning cards over cards offering no rewards makes sense. Cards with rewards mean cardholders can earn rebates and bonuses in exchanges for purchases. Interestingly, when PYMNTS Intelligence asked survey respondents their preferred method to manage planned and unplanned expenses, reward-earning cards topped the list for both types of expenditures.

PYMNTS Intelligence also found reward-earning cards to be the primary borrowing tool for one-third of low-revenue businesses (in the study, those earning less than $1 million annually). Twenty-five percent of middle-revenue SMBs (earning between $1 million and $10 million each year) also favor credit cards with rewards, as do 23% of high-revenue firms ($10 million or more).

The appeal of reward-earning credit and debit cards among low-revenue SMBs suggests those businesses place a premium on the immediate and tangible benefits those cards can provide. It’s common for cards to offer cash-back rewards and points that can be applied to travel, both of which can be useful to entrepreneurs fighting to get ahead.

As appealing as the terms of the proposed Visa and Mastercard settlement might sound to merchants frustrated by exchange fees, it’s possible that the deal — which is intended to benefit SMBs — could undercut some of the perks they now earn.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More