Payments preference calls the tune these days — and to mix metaphors, you’re either the steamroller or the road when it comes to offering the optimal payments mix.

For credit unions (CUs), the issue is somewhat more critical, as card networks and competing financial institutions (FIs) threaten to poach customers with enticing card offers.

Per the August 2021 Credit Union Innovation Playbook: Portfolio Leakage Edition, a PSCU collaboration, “Attractive credit card offers from other financial institutions (FIs) pose important brand and downside revenue risks to credit unions. PYMNTS’ latest research reveals that 100% of CU executives say that losing credit card portfolios to competitors would have anywhere from a ‘very’ to ‘extremely’ detrimental impact on their revenues.”

Researchers surveyed a census-balanced panel of nearly 5,240 U.S. consumers to gauge how many non-CU financial products and services consumers are using — and perhaps more importantly, “what percentage of members could be convinced to have their primary FIs be their sole providers of financial products and services.”

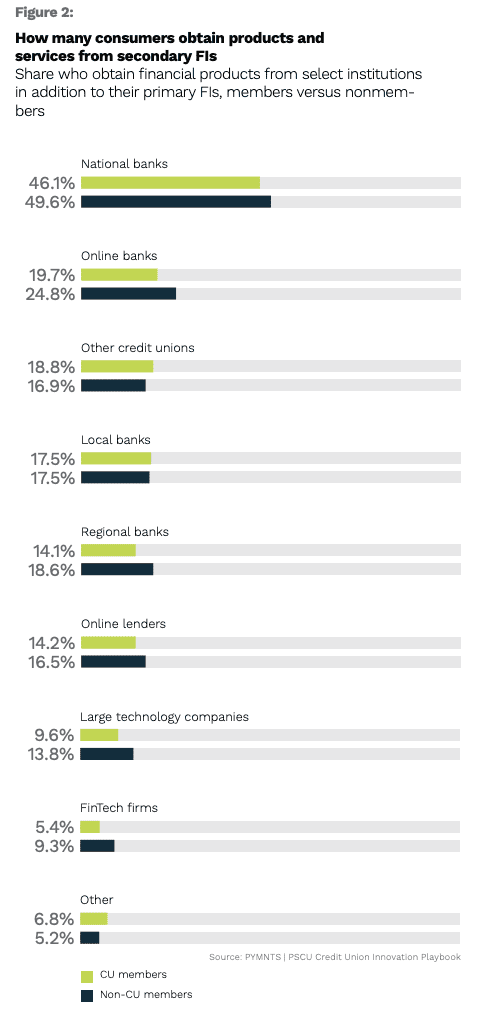

Finding that 55% of members currently use at least one product or service from another FI, the new Credit Union Innovation Playbook adds that 46% of CU members who use non-CU financial services “obtain them from national banks — more than twice as many who do so from any other type of secondary FI. Online banks are a distant second, accounting for 20% of members who get financial products from other FIs.”

With credit cards, first-time home mortgages, mortgage refinancing and auto loans standing out as high-risk for portfolio leakage, CUs have some work to do on this front.

Advertisement: Scroll to Continue

See also: The Credit Union Innovation Playbook ‑ Portfolio Leakage Edition

National Banks Knocking on CUs’ Doors

Digging into the data, national banks stand head-and-shoulders above other CU rivals.

“National banks are by far the most common type of institution from which both CU members and non-CU members obtain products and services outside their primary FIs, but they are not CUs’ only competition for portfolio originations,” per the latest study.

For example, 46% of CU members and 50% of nonmembers who bank with two or more FIs use national banks in addition to their primary FIs. “Online banks are a distant second, with 20% of CU members and 25% of non-CU members with multiple FIs saying they obtain at least one financial product through online banks. Local banks, regional banks, online lenders and technology firms make up the tail end of this ecosystem,” per the Playbook.

The good news is that CUs are wise to the lures of competitors — and they’re retooling offers.

The new Playbook states that “48% of members who currently use credit cards from other FIs would be willing to drop those FIs if their CUs offered more innovative credit cards, for example, and 49% of those who have taken out auto loans with secondary FIs would do the same for that product. This share is 59% for personal loans.”

Learn more: The Credit Union Innovation Playbook ‑ Portfolio Leakage Edition

Members Will Drop Competitors if CUs up Their Game

With fully 100% of CUs willing to innovate credit card and loan products to keep members away from competitors, timing is good for part two of the digital shift.

The August Playbook notes that 66% of members holding business lines of credit “with FIs other than their primary CUs say they would be willing to drop those business credit lines if their CUs could offer more innovative alternatives.”

In a weird disconnect, however, less than half (45%) of CUs said they are “willing to innovate business credit products to alleviate portfolio leakage.” It’s an odd stalemate that’s unlikely to last.

“CUs appear to lack a clear understanding of their members’ motives for banking at other FIs, which should be an essential basis for attacking the portfolio leakage problem,” per the Playbook. “Nearly all credit union decision-makers believe that members bank with competitors to obtain products they do not have access to at the CU,” it states, adding that 90% of CUs with members who obtain financial products from competitors “believe this is at least one reason why their members seek out secondary FIs.”

Read more: The Credit Union Innovation Playbook ‑ Portfolio Leakage Edition