Digital banking has become the way of the world.

More consumers than ever are banking on their financial institutions’ (FIs’) mobile-optimized websites and apps amid the ongoing pandemic, making digital innovation a top priority for credit unions (CUs), banks and FinTechs alike. But what types of innovations will go the farthest to deliver the digital banking experiences that bank customers want?

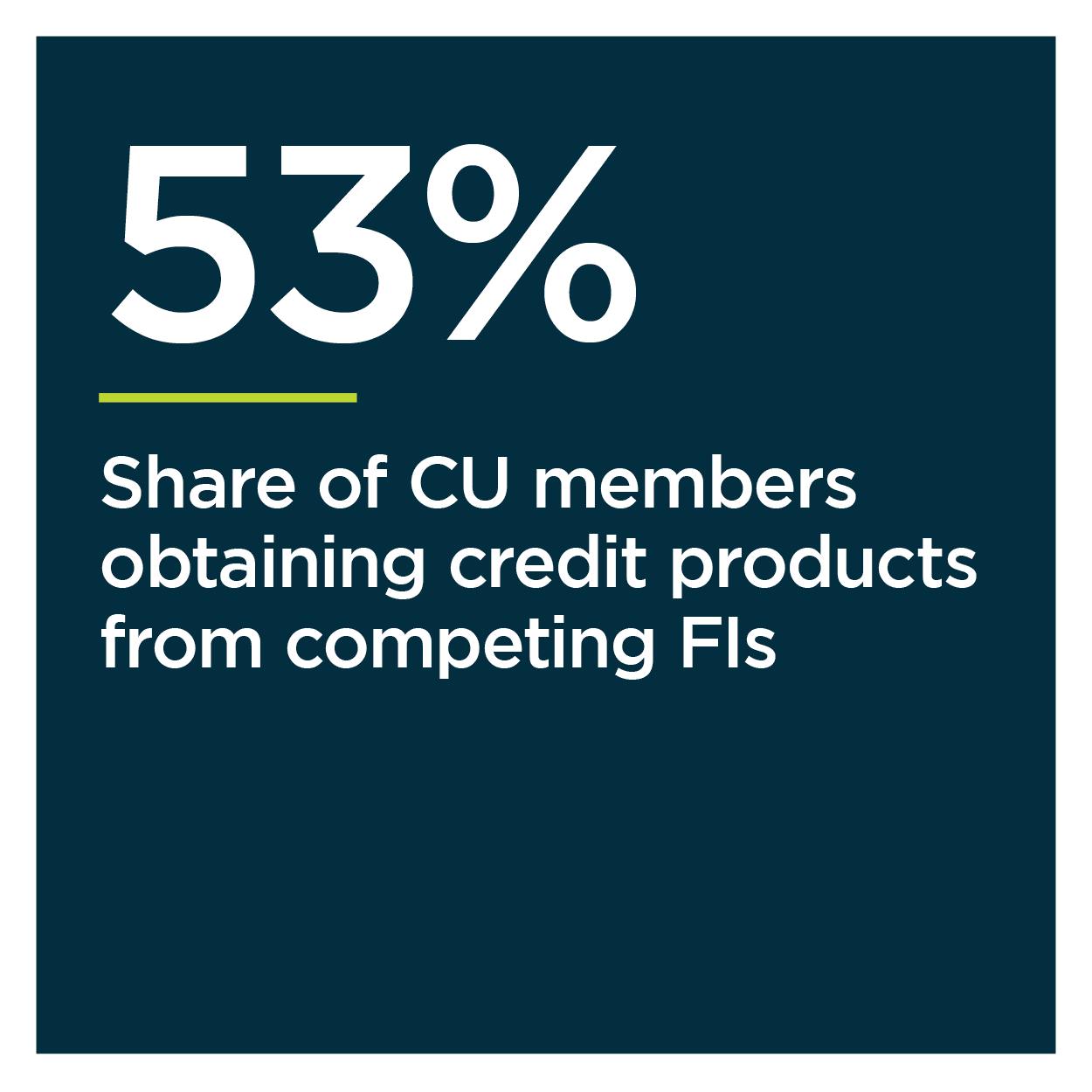

Choosing the right digital products and services to develop is especially important for CUs. Members tend to be more satisfied with their CUs than other banking customers are with their primary FIs, but dissatisfied CU members are twice as likely to feel like their CUs’ online banking options are coming up short. They are also three times as likely as dissatisfied non-CU members to be unhappy with their CUs’ mobile banking options. This strongly suggests that many CUs are not meeting their members’ expectations when it comes to enabling the digital banking experiences they see as central to their financial lives. How should these CUs change their approach to innovation to better suit their members’ needs?

Choosing the right digital products and services to develop is especially important for CUs. Members tend to be more satisfied with their CUs than other banking customers are with their primary FIs, but dissatisfied CU members are twice as likely to feel like their CUs’ online banking options are coming up short. They are also three times as likely as dissatisfied non-CU members to be unhappy with their CUs’ mobile banking options. This strongly suggests that many CUs are not meeting their members’ expectations when it comes to enabling the digital banking experiences they see as central to their financial lives. How should these CUs change their approach to innovation to better suit their members’ needs?

The Credit Union Innovation Study, a PYMNTS and PSCU collaboration, provides a first-hand account of what CUs need to prioritize to gain — or keep — their competitive edge. We surveyed a census-balanced panel of 4,817 U.S. consumers to discover how the mounting need for digital-first banking options is changing the types of innovations CUs are prioritizing. We also surveyed 101 CU decision-makers and 50 FinTech executives to learn how both t ypes of organizations’ innovation plans compare against what their members and customers want.

ypes of organizations’ innovation plans compare against what their members and customers want.

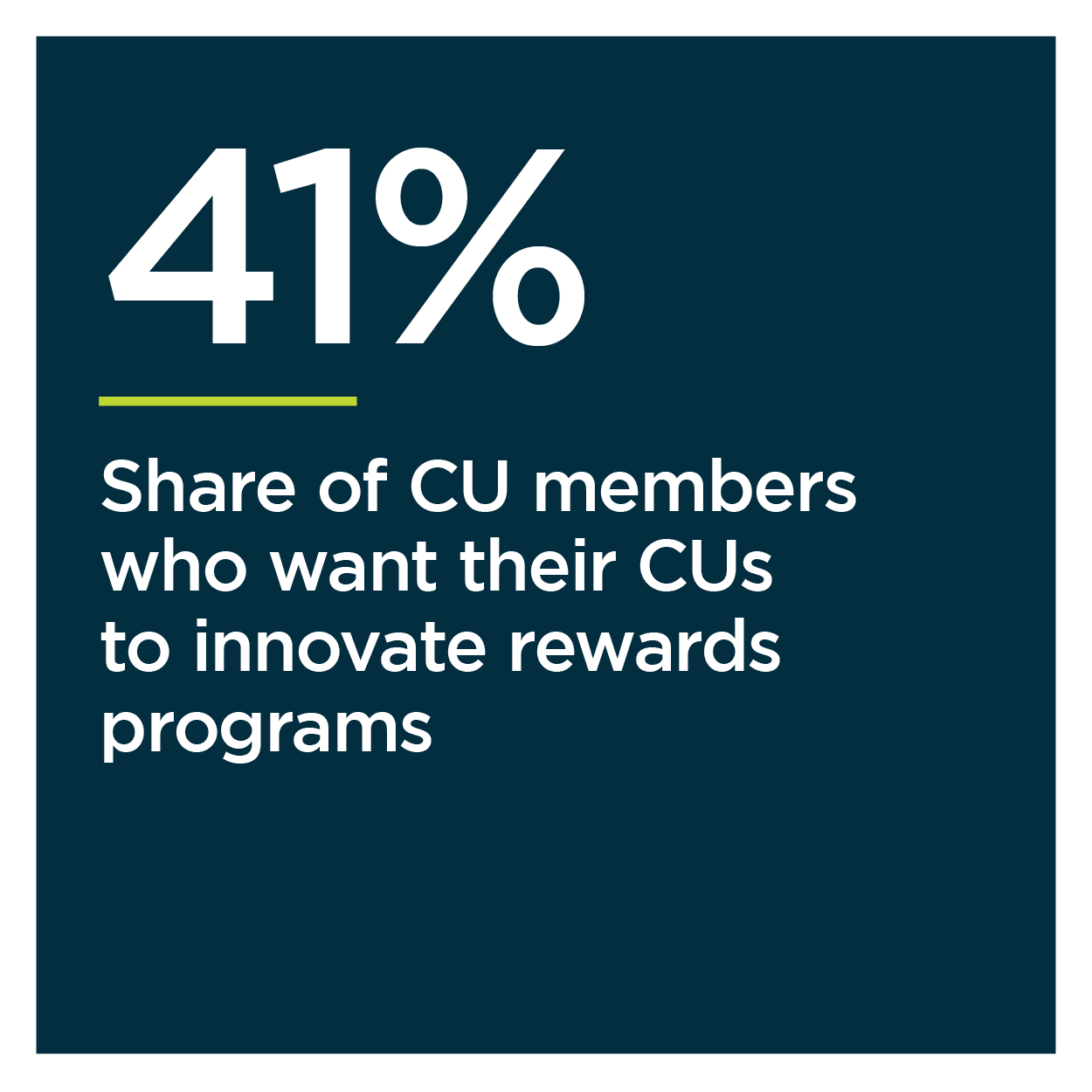

PYMNTS research shows that although investing in these digital banking features is necessary, it is often not enough for CUs to meet their members’ expectations. Certain digital banking features, like mobile wallets, have become so common that CU members rarely see them as innovative at all. CU members are therefore less interested in seeing CU innovation in areas such as mobile wallets as they are in seeing loyalty and rewards innovation and anti-fraud solutions. Only 17 percent of CU members want their CUs to innovate mobile wallet capabilities, while 41 percent want them to develop new loyalty and rewards programs, for example.

Despite this, mobile wallet innovation is actually the most common area in which CUs have invested in recent years. Eighty-six percent of CUs report investing in mobile wallets, in  fact, even while only 42 percent are investing in the anti-fraud capabilities that more of their members want.

fact, even while only 42 percent are investing in the anti-fraud capabilities that more of their members want.

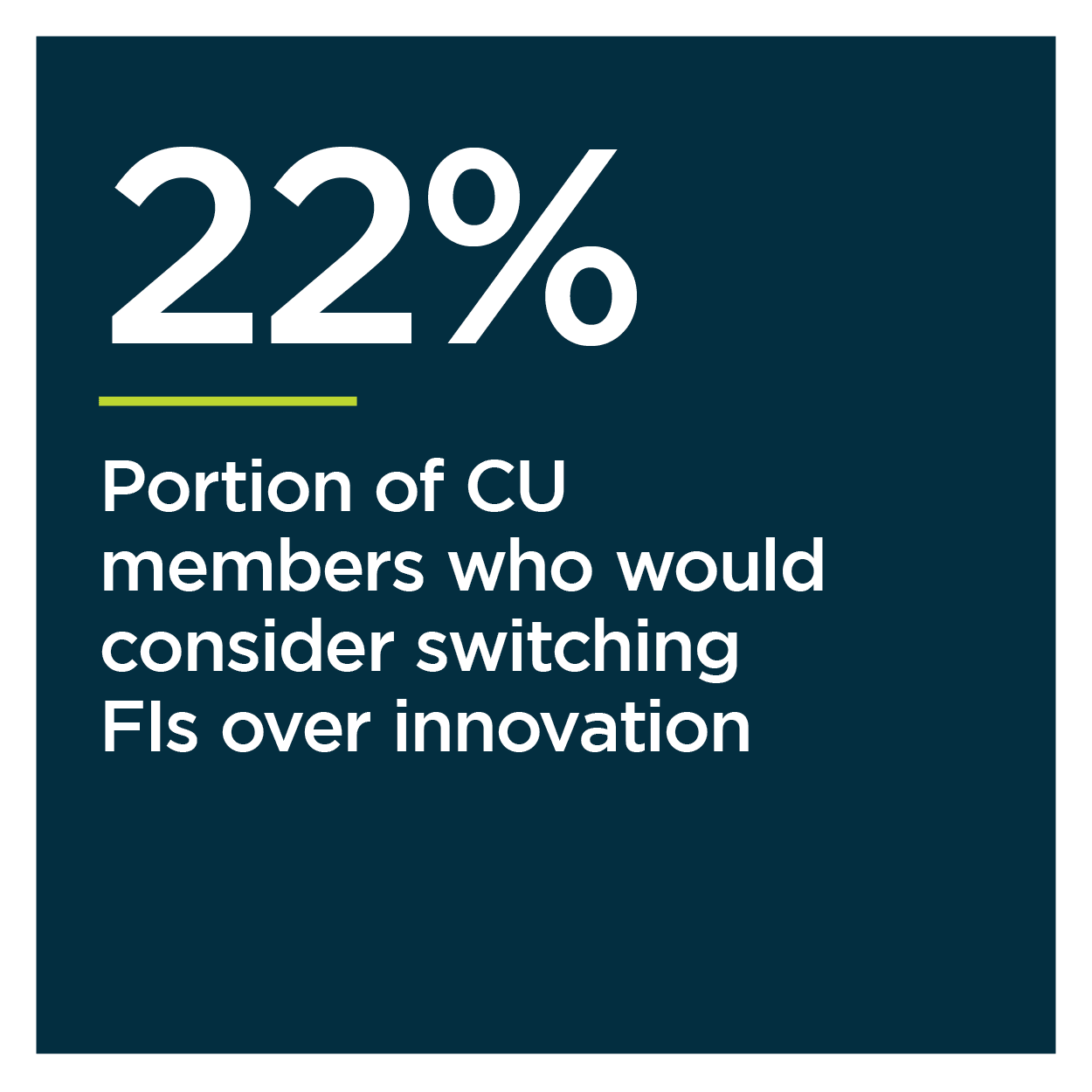

This disconnect between the types of innovations in which CUs are investing and the types that their members would like them to prioritize only scratches the surface of the complex ways in which rapid shifts in CU member demand have changed their relationships with their CUs.

To learn more about the root causes of this disconnect, how CUs can close the innovation gap and what could happen if they do not, download the study.