It doesn’t take a FinTech to make banking digital. In fact, it doesn’t even require a big bank. Credit unions (CUs) can be perfectly adept at extending the digital-first payment technologies that have defined the pandemic — and hopefully the post-pandemic era.

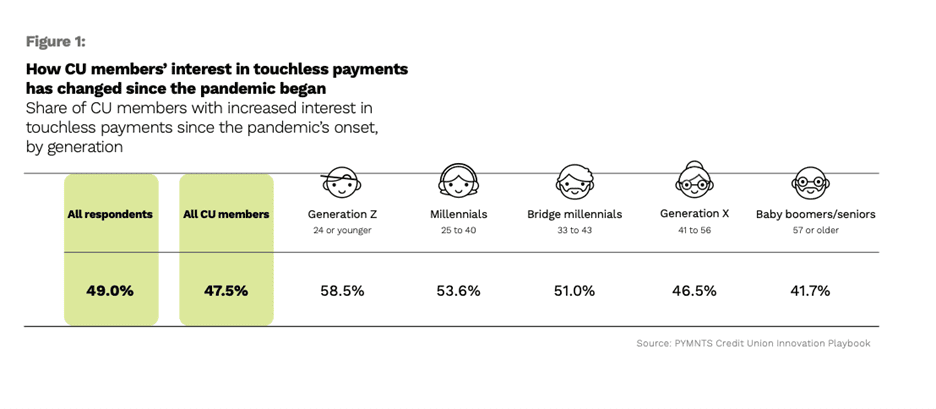

PYMNTS’ latest research shows that half of all CU members in the United States are more interested in touchless technologies like contactless cards, mobile wallets, card-on-file options and QR code-enabled payments than they were before the pandemic began. As stated in the Credit Union Innovation Playbook, CU members are so invested in being able to make touch-free payments that one in five would leave their current CUs for financial institutions (FIs) that enable touchless payments access.

Extending those digital-first innovations is a key focus for PSCU, the nation’s largest credit union service organization. As Denise Stevens, senior vice president and chief product officer at PSCU, told PYMNTS, FinTechs do not necessarily offer more than CUs, particularly when it comes to touchless products. In fact, she said, CUs — contrary to conventional wisdom — can be fairly tech-savvy. Even a few years ago, CUs were quick to embrace digital wallets, although those initiatives were stymied (before the pandemic) by the fact that merchants were not quite ready to wholeheartedly embrace the wallets (Google Pay, Apple Pay and others).

Like any FI, CUs have had to pivot during the pandemic and step back to reevaluate their digital strategy. They’ve had to examine what they’ve been missing, what they need to do more of and what worked well. Increasingly, said Stevens, “CUs are all-in on digital. If they were ‘average,’ they are going to be better because they understand how important the digital channel is. If they were good, they are going to be great.”

That comes as CUs have been eyeing new products and services, such as contactless options and payment forms. Forty-eight percent of all CU members say their interest in touchless payments technologies has increased since the pandemic began, underscoring the degree to which the crisis has shifted their payment preferences.

Interest in touchless payments is even higher among digital-first banking generations, like millennials and Generation Z members, who have grown up using connected devices to shop, pay and manage their finances. Fifty-four percent and 59 percent of millennial and Gen Z CU members, respectively, said they are more interested in using touchless payments for in-store purchases now than they were prior to March 2020. This signals that touchless payments capabilities will be key to attracting and retaining these digitally savvy members going forward.

At present, Stevens said, contactless card adoption is on the rise. PSCU has issued over 6.8 million contactless cards in the last year.

“They’re reaching members’ hands,” she said of those cards, adding that “when you really lay out the feature functionality of a progressive credit union against a FinTech, there isn’t a lot of difference with the actual offering.”

No Single Solution

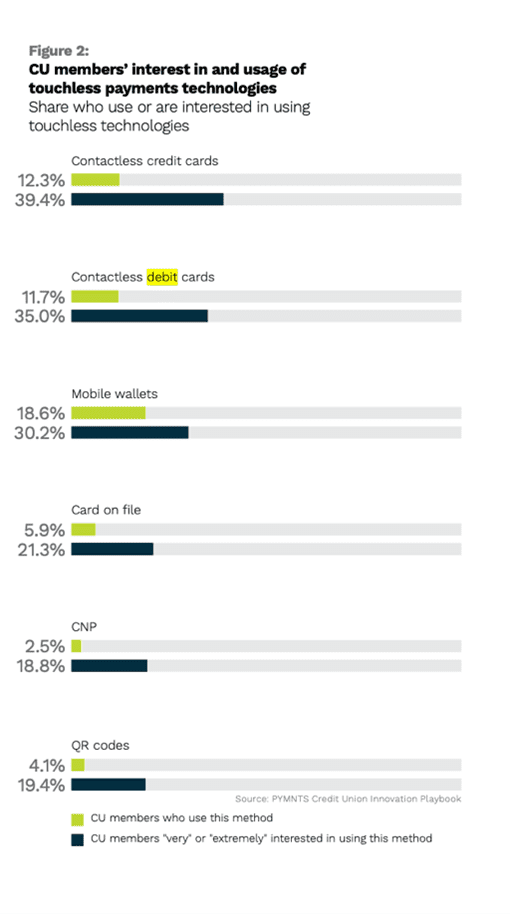

There is no one-size-fits-all solution for a CU, noted Stevens, although contactless cards may be focused on debit products right now, as debit payments are growing more quickly than credit payments. CU members express interest in all types of touchless payment options, but their interest in contactless credit and debit cards is unmatched. Thirty-nine percent of all CU members are either “very” or “extremely” interested in using contactless credit cards, while 35 percent are “very” or “extremely” interested in using contactless debit cards. This makes contactless cards the first- and second-most in-demand touchless payments options among CU members. Only 19 percent of all CU members have expressed similar levels of interest in QR code-enabled payments and card-not-present (CNP) capabilities, by contrast.

CUs generally recognize the importance of touchless payment options in meeting their members’ demands, but few of their members have access to the touchless payment methods they want to use. CU members are three times as likely to be interested in contactless credit cards as they are to report using them, for example. They are also twice as likely to want to use contactless debit cards as they are to use them. Closing the gap between CU member interest in contactless cards and access to them will therefore be critical for CUs aiming to meet their members’ touchless payment demands.

CUs generally recognize the importance of touchless payment options in meeting their members’ demands, but few of their members have access to the touchless payment methods they want to use. CU members are three times as likely to be interested in contactless credit cards as they are to report using them, for example. They are also twice as likely to want to use contactless debit cards as they are to use them. Closing the gap between CU member interest in contactless cards and access to them will therefore be critical for CUs aiming to meet their members’ touchless payment demands.

“If we look at our statistics at an aggregate level here at PSCU, debit is really outpacing credit at this point, which is normal against the [financial services] industry itself,” said Stevens. “CUs must mull which parts of their portfolios to reissue. Then you have the next decision: ‘How am I going to reissue it?’ because there are really two approaches. A CU can decide to replace every card in a given portfolio, or it can simply wait for a card to be reissued upon expiration, damage or loss.”

The FinTech Factor

The situation for CUs is urgent. They could lose their members if they don’t begin investing in touchless payments innovations. PYMNTS research shows that 15 percent of all CU members would be “very” or “extremely” likely to leave their current CUs if competitors offered touchless payments options. It also found that 21 percent of members would be “somewhat” likely to switch FIs for touchless payments.

This is especially notable because many FinTechs are innovating those touchless payments to steal members from CUs. Sixty-four percent of FinTech executives said they would go around their partner CUs and banks if it meant selling directly to end users. CUs are thus in a race to roll out touchless payment innovations before their FinTech competitors beat them to the punch.

“Most credit unions will still have to offer a variety of payment types to capture the overall desire of the membership base because people do transact and process payments in different ways,” explained Stevens. “Again, I think credit unions need to stay very diligent on their digital strategies — that isn’t going to change.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More