With lending rates climbing, credit unions are continuing to offer more affordable auto loans.

As The Wall Street Journal reported Tuesday (Dec. 27), credit unions (CUs) charged an average interest rate of 5.94% for used cars in the third quarter, compared to the 8.36% rate offered by banks. This was the largest gap in at least five years, the report said, citing data from Experian.

For consumers in the market for new cars, CUs charged an average rate of 4.43%, while banks were charging 6.06%. The report noted that while it’s not unusual for CUs to offer lower rates than banks, the extent to which they are doing so amid rising rates has drawn notice in the consumer-lending sector.

“They kept rates low when the rest of the market just exploded,” John Toohig, head of whole-loan trading at Raymond James, told WSJ.

CUs had a larger share of the auto-finance market than any other type of lender during the third quarter, holding 28% of all auto financing, compared to 20% a year earlier, according to the report.

As PYMNTS has reported, consumers have cut back on buying big-ticket items such as cars as their economic situation grows more precarious. Data from the Department of Commerce released earlier this month showed retail sales falling for November, driven in part by a 2.6% slump at car dealerships.

And a survey by Cox Automotive Dealers found American auto dealer sentiment at its lowest level since the start of the pandemic.

And a survey by Cox Automotive Dealers found American auto dealer sentiment at its lowest level since the start of the pandemic.

“Dealers are normally optimistic, so the drop in the 3-month outlook to a new low in our survey history is particularly noteworthy,” said Johnathan Smoke, chief economist at Cox. “As the year began, dealers were telling us about one obvious problem: inventory. Now, as 2022 comes to a close, it’s all about the economy and interest rates.”

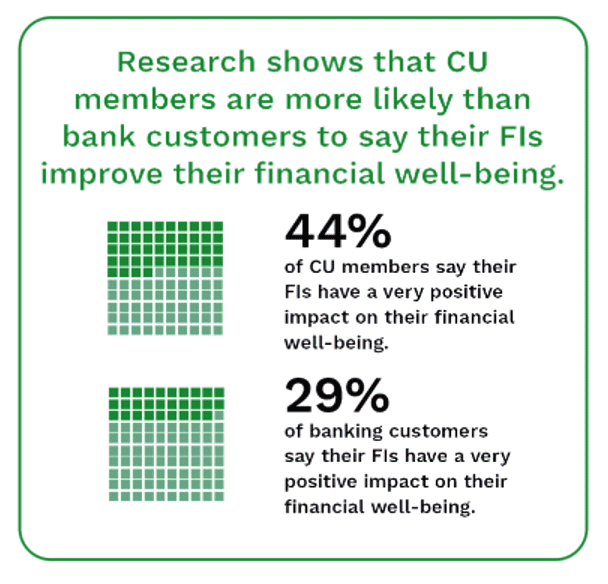

Against this backdrop, CUs are well-positioned to help struggling consumers, PYMNTS wrote last week. CUs have already established themselves as a positive force in consumers’ lives, with 90% of CU members saying their institutions make it easy to manage their finances.

Part of the reason CUs can provide such help — as noted in PSCU’s “Eye on Payments” 2022 report — is their access to data and community connections, which lets them deploy actionable strategies. These strategies can include surveys to assess members’ financial health, behavior modification alerts, and other tools.