Retail banking customers rely on digital services more than ever before, making it essential for all consumer-facing financial institutions (FIs) to keep pace with continuous innovations in the space. Credit unions (CUs) compete favorably with smaller for-profit FIs and even large national banks in core areas, such as online banking. Today’s consumers demand seamless access to more sophisticated digital products, however, such as digital wallets and real-time payments, making the road ahead more challenging — especially as FinTechs continue to disrupt the market.

CUs perform well on overall retail banking satisfaction, often receiving higher customer satisfaction ratings than other FIs. One recent survey found that 89% of CU members were pleased with their FIs, surpassing community banks at 86%, digital-only banks at 77% and large banks at 76%. The survey also indicated that consumers view credit unions three times more favorably than large national banks in terms of putting customers before profits. Just 24% of the respondents used a CU as their primary FI, however, versus 45% for the big banks. This month, PYMNTS Intelligence examines what consumers expect from their CUs regarding mobile and digital banking and how CUs can deliver on these expectations.

Growing Urgency on Digital Transformation and Real-Time Payments

Growing Urgency on Digital Transformation and Real-Time Payments

One of the key reasons for the gap between member satisfaction and market share appears to be the lack of a sense of urgency on CUs’ part, though this is improving. A new study from FICO revealed that 31% of CUs have not launched a digital transformation strategy, and 76% have no plans for fundamental changes to their systems to achieve digital transformation.

A February PYMNTS survey of CU executives found that just 19% identified their respective CUs as “early launchers” — those that move more quickly than their rivals — on digital innovation in 2021. This represents a significant rise from 12% the previous year and 8% in 2019.

An especially critical area is real-time payments. PYMNTS’ most recent survey of CU executives showed that 99% of CUs now offer some form of real-time payments service. Nearly one-quarter do not provide a real-time payment option to all their members, however, placing them out of step with the needs of many retail banking customers.

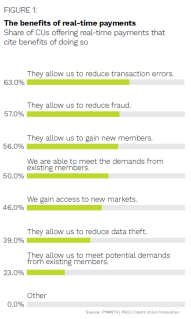

The study further indicated that most CU executives underestimate the value of real-time payments innovation to their members. Just 23% believed that the technology allows their CUs to meet potential demand from existing members, 56% agreed that providing this service allows them to gain new members and 46% believed it helps them reach new markets. Sizable portions of these executives also did not believe that real-time payments help reduce transaction errors or fraud or provide other benefits that the technology does in fact deliver.

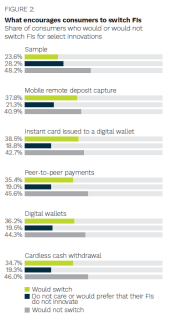

CUs must build momentum on digital innovation to retain existing members and acquire new ones. A large portion of consumers are eager to access retail banking innovations — and they are willing to change providers to do so. A recent PYMNTS survey polled consumers on their preferences surrounding digital banking innovation and found that 39% would switch to a different FI that offered instant cards issued to their digital wallets, a technology that allows customers to begin making purchases immediately without waiting for physical cards to arrive.  Thirty-eight percent would move to a new FI to use mobile check deposits, 36% would do so to get basic digital wallet access and 35% would switch for peer-to-peer (P2P) payment functionality.

Thirty-eight percent would move to a new FI to use mobile check deposits, 36% would do so to get basic digital wallet access and 35% would switch for peer-to-peer (P2P) payment functionality.

PYMNTS’ data showed that the top reason for consumer interest in real-time payments is ease and convenience, selected by 23% of respondents. Other popular reasons include instant availability of funds at 22% and easy tracking of payments at 14%. Real-time payments are especially important to CUs in attracting members from the millennial and bridge millennial age groups, with 61% and 59%, respectively, indicating that they are “very” or “extremely” interested in the service.

Forty-eight percent of respondents earning at least $100,000 per year, meanwhile, expressed strong interest in real-time payments, compared to 39% of those earning between $50,000 and $100,000 and 30% of those earning less than $50,000. Consumers who identified themselves as comfortably living paycheck to paycheck also had a notable interest in real-time payments at 45%.

As digital banking becomes table stakes, retail banking customers expect access to an ever-growing suite of technologies, including real-time payments, instant loan approvals and cryptocurrency. CUs must make these innovations a top priority to remain relevant in the rapidly changing landscape.