But in today’s digital age, where a seamless and convenient experience across various touchpoints has become table stakes, particularly within financial services, prioritizing innovation has never been more mission-critical to long-term success.

So, what’s holding financial institutions like credit unions back from innovating new products and services to help win new members and better serve their current members?

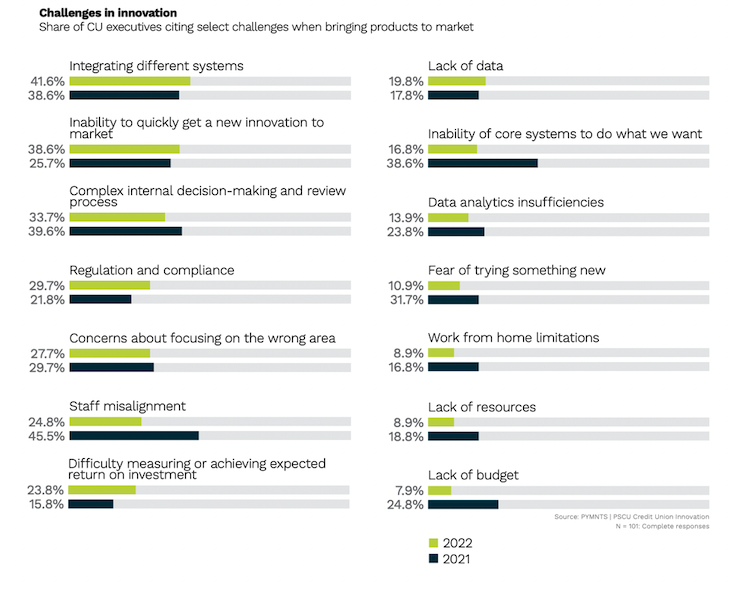

For the latest research in “Credit Union Innovation: The Race to Meet Consumer Demand,” a PYMNTS and PSCU collaboration, PYMNTS surveyed 6,483 U.S. account holders and 151 credit union executives. The top two challenges that credit unions face when innovating include integrating various systems at once and being unable to bring innovations to market quickly enough, according to the study.

Additionally, 28% of credit unions remain concerned about focusing their efforts in the wrong area, which could be why 34% reported getting bogged down in complex internal decision-making and review processes.

Additionally, 28% of credit unions remain concerned about focusing their efforts in the wrong area, which could be why 34% reported getting bogged down in complex internal decision-making and review processes.

Prioritizing innovation can allow credit unions to better meet customer expectations by offering personalized experiences that build trust and loyalty, gain a competitive advantage by accessing new markets, and improve their own operational efficiency.

Advertisement: Scroll to Continue

That’s because staying relevant is frequently the best way to stay in business. The financial services landscape is highly competitive, so effective innovations can give firms a winning edge in the market.

Still, 56% of third-party FinTech vendors providing credit unions with digital products said credit unions are taking too long to adopt new technology.

In a crowded and rapidly evolving environment, this spells trouble.

Innovation can open doors to previously untapped markets. For example, younger generations are often more tech-savvy and inclined toward digital banking. By offering innovative solutions that cater to their preferences, credit unions can attract these potential customers who may not have considered traditional banking options before.

Product and service innovations can also result in cost savings, improved productivity and faster response times for credit unions.

When these firms operate more efficiently, they can pass on these benefits to customers in the form of better services and competitive rates. This helps accelerate customer happiness and satisfaction, which is the backbone of sustainable success and long-term member relationships.

The study found that half of credit union members said they value product innovation, and nearly one-quarter said they would take their business to another financial institution to find innovative products and services.