These newly minted members are migrating to credit unions due to the appeal of competitive interest rates, lower fees and the accessibility of staffers, The Wall Street Journal reported Tuesday (March 5).

PYMNTS Intelligence has also found over the last several years, that credit unions have been upping their game to expand their member base.

However, members new and old still expect credit unions to deliver the kind of cutting-edge, digital-first capabilities that traditional banks offer their customers.

The PYMNTS Intelligence report “2024 Credit Union Innovation Readiness Index” confirmed that some CUs are rising to the innovation challenge, while others lag behind.

In compiling the report, PYMNTS Intelligence conducted two surveys — one with more than 200 credit union executives, and the other with 4,525 U.S. consumers, who were asked about the products and features they would like to see credit unions offer.

The report found that those credit unions deemed “most innovative” were those that were delivering on members’ innovation expectations almost 70% of the time. The bottom-performing credit unions surveyed, meanwhile, were only delivering on about 40% of the innovations that members look for.

Not coincidentally, top-performing credit unions were also the ones most willing to invest in product innovation — and most likely to reap benefits from doing so. For instance, top-performing credit unions invested 13% more into payment innovations than low-performing credit unions, and, as a result, 90% of them saw a positive return on investment.

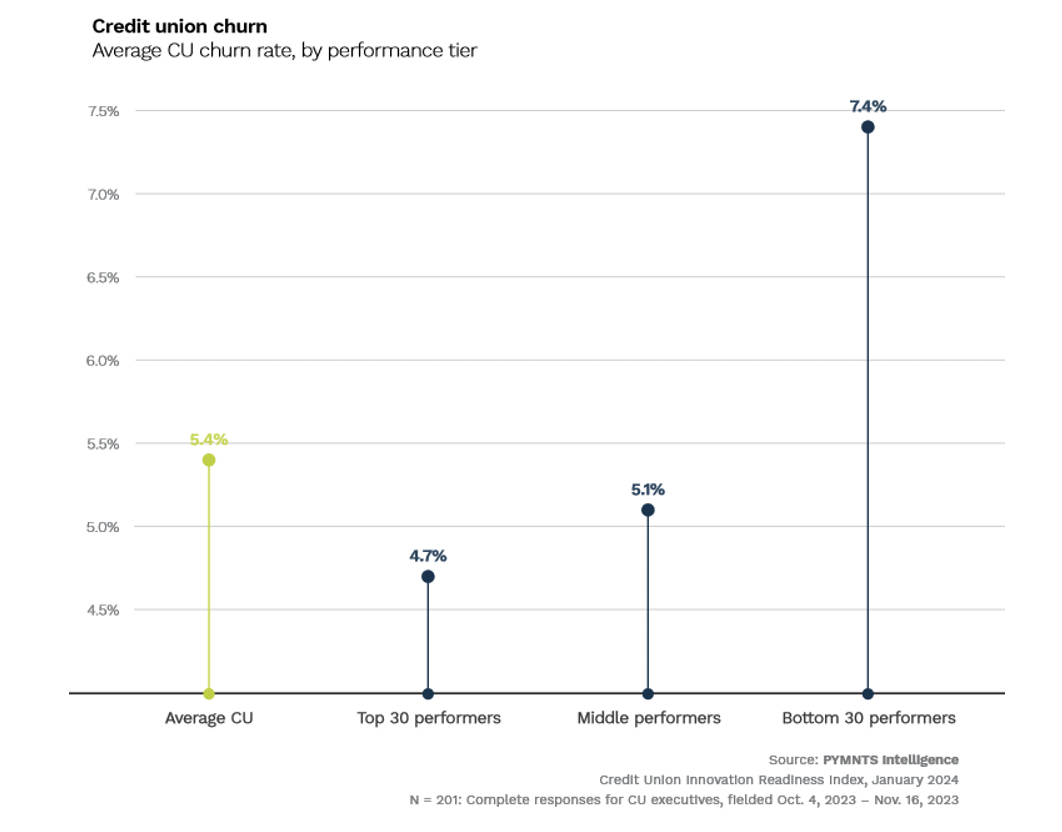

These investments also appeared to pay off in the form of customer satisfaction. The report found that member churn was 57% lower for top-performing credit unions than bottom-performing ones. Top-performing credit unions’ member churn was 4.7% last year, while bottom performers witnessed a member churn rate of 7.4%, indicating those credit unions that are willing to invest in innovation not only stand to gain a competitive edge, but also higher levels of customer satisfaction.

However, investing in innovation appears to be only part of the formula for credit union success. The report also confirmed that consumers place a premium on personalized member experience, which may explain why high performers were making it a priority.

However, investing in innovation appears to be only part of the formula for credit union success. The report also confirmed that consumers place a premium on personalized member experience, which may explain why high performers were making it a priority.

Seventy-three percent of top-performing credit unions surveyed said delivering a “highly personalized user experience” was one of their organization’s top priorities for the next three years, while only 55% of low-performing credit unions said the same.

Instead, 61% of bottom-performing credit unions said their three-year plan included offering members features such as enhanced user experience and less restrictive credit offerings. However, only 40% of top performers said they thought improved user experience would draw new members, and only 23% of the top-tier credit unions said they believed less-restrictive credit offerings would resonate with prospective members.

Instead of guessing what members might want, credit unions should include members in the decision-making process.

The report found that 60% of top-performing credit unions invited members to help test proposed innovations — something only 32% of bottom performers did. And while 60% of the top performers had a process in place that enabled members to identify their preferred innovation priorities, only 45% of bottom performers did, suggesting that many credit unions may be missing out on an opportunity to fully engage their members in strategic planning.