According to PYMNTS Intelligence data, 95% of U.S. credit unions (CUs) are now wooing prospective Gen Z members.

However, as “How Credit Union Innovation Can Drive Gen Z Engagement, makes clear, Gen Z consumers are a fickle bunch. In the past year, 42% of Gen Z CU members switched their primary financial institution (FI). To put that propensity to switch in perspective, Gen Z consumers are 2.5 times more likely than their Gen X counterparts to have switched their primary FI in the past year, while less than 4% of baby boomers and seniors recently switched.

So, if Gen Z is so temperamental, why are CUs so keen on bringing these younger consumers into the fold? One reason is that they are poised to transition into higher-paying jobs and careers in the years to come, which will drive additional spending. In fact, it’s projected that by 2030, Gen Z consumers will increase their spending sixfold, meaning they will likely need access to more sophisticated financial products.

But their high churn rate suggests Gen Z consumers have high expectations from the FIs that get their business, and our report, created in collaboration with Velera (formerly PSCU/Co-op Solutions) and drawing on survey data from more than 200 CU executives and 4,525 U.S. consumers, reveals that what they really look for in financial services providers are innovative products and features. Should a financial institution fail to deliver these expectations, these digital-first consumers have no qualms about taking their business elsewhere.

If CUs are determined to persuade Gen Z consumers to become members, they need to have an innovation roadmap in the works — one designed to retain current younger members while attracting new ones.

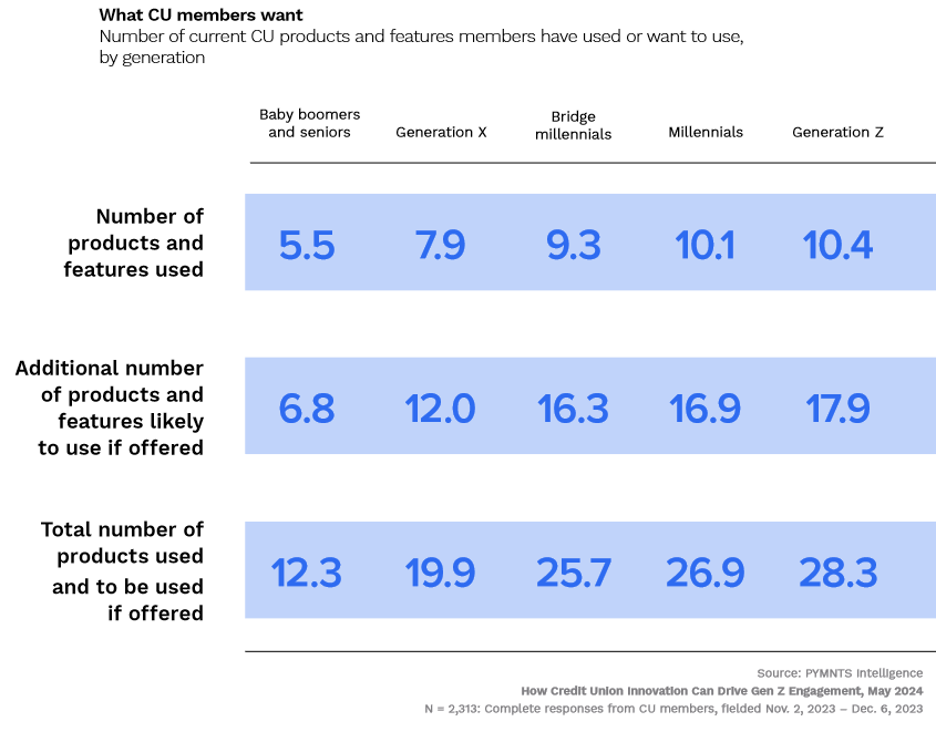

As the accompanying figure illustrates, Gen Z members use more products and features right now than any of the other generations we surveyed — and they would welcome even more if additional features were on the menu. The average Gen Z consumer has used 10 credit union products and features in the past year, but would use an additional 18 if offered, meaning they would be comfortable juggling nearly 30 different products and features.

Advertisement: Scroll to Continue

For comparison, the average Gen X consumer has used about eight CU products and features in the last 12 months and would use another 12 if offered. Baby boomers and seniors have used about six in the last year and could envision using seven more if offered.

This generational difference starkly illustrates what credit unions — and all FIs for that matter — will need to accomplish to meet the needs of younger consumers — and their notably large appetite for innovative products and features. Data shows they are already comfortable switching up their primary FIs, so the new features can’t come soon enough.