Under SB-1075, the 100+ CUs now doing business in the Golden State would be prohibited from charging their customers more than three overdraft fees per month. The bill would also require CUs to give customers a five-day grace period to replenish their accounts before charging them any fees.

“Although overdraft is viewed as a financial tool by credit unions, its fees are inherently predatory,” the bill’s co-author, state Sen. Steven Bradford, told fellow lawmakers last week.

The California Credit Union League responded by asking state residents to encourage their local representatives to push back on the proposed law because it “imposes stringent requirements on how state-chartered credit unions serve their members.” At the very least, the trade group asked lawmakers to table the bill until the Consumer Financial Protection Bureau (CFPB) issues a decision on the proposed fee cap it introduced in January.

There’s no denying overdraft fees can be a burden to Americans struggling to pay their bills. The CFPB estimated the proposed fee cap would save U.S. consumers $3.5 billion a year. But, as PYMNTS recently reported, CUs remain popular with Americans for a number of reasons, including affordable fees.

But CUs are also delivering on other consumer needs.

Advertisement: Scroll to Continue

For example, when consumers submit credit applications, it usually means they need cash. Reduced wait times between applications and approvals can be crucial, helping applicants gain quicker access to the funds they need.

And as we found in “Credit Union Innovation: How Credit Products’ Rates and Terms Impact FI Selection” — a PYMNTS Intelligence collaboration with PSCU/Co-Op Solutions — 45% of CU executives said they are making significant efforts to cut down on waiting times after members apply for credit.

Having quick access to funds is an important feature for more than a quarter of all account holders, and 59% of CUs said their expedited product setup times sway members to apply for credit products.

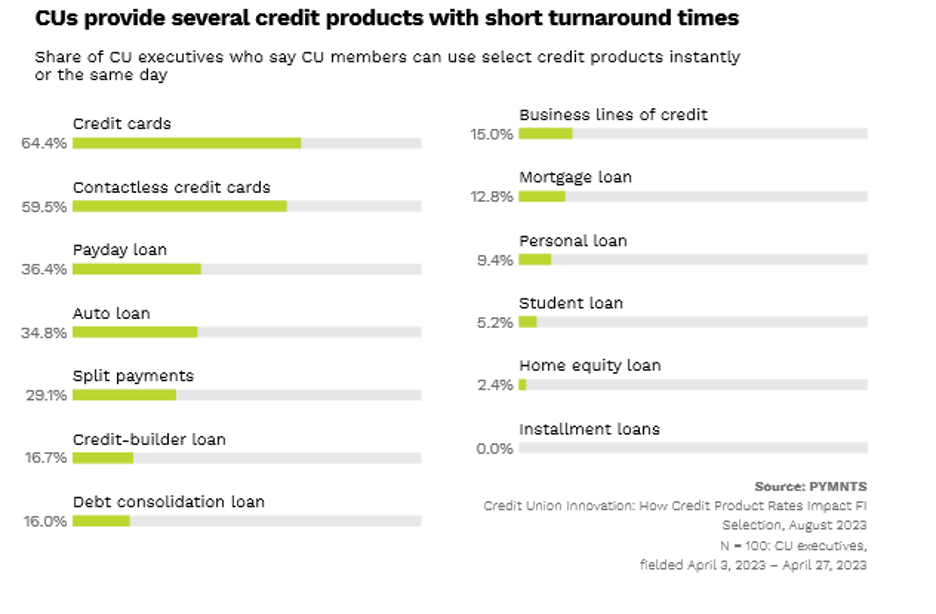

As the chart above shows, CU executives make reduced loan-application turnaround times a priority, with 64% saying they process credit card applications the same day, while more than 36% finalized payday loan applications just as quickly.

Quick access to credit is just one reason members value their credit unions. In a follow-up PYMNTS Intelligence report, “Growing Credit Union Membership via Lending and Omnichannel Banking Innovation,” we asked more than 4,500 consumers what they looked for when selecting a primary financial institution, and 81% of the CU members surveyed said they value the innovation their credit unions deploy.

Seventy percent of current CU members said their CUs innovate well or very well, and they want them to continue. CU members said they expect their CU to innovate an average of 4.4 products and 4.2 features over the next three years, which is much higher than the three products and three features traditional financial institution (FI) customers are expecting.

One example of this hunger for innovation is this: 8% of CU members tell us they specifically switched to a credit union because their previous FI lacked sufficient online and mobile banking features.

But speed and innovation are double-edged swords. CU members want both so much that they told us they would switch to another FI should their current CU fail to live up to their expectations.

Which brings us back to a larger point: it’s unclear why California lawmakers have put credit unions in their crosshairs, especially in light of the proposed CFPB fee cap, which will likely impact both credit unions and traditional FIs. In fact, California CU executives probably hope SB-1075 doesn’t slow their plans to innovate further, because whether consumers want lower fees, faster access to credit, or more innovative products, they can vote with their feet and find an institution that better meets their needs.