Consumers and businesses alike are expressing more curiosity surrounding emerging payment methods after a year of rapid change to common shopping and banking practices. Both groups are making a larger amount of their daily transactions online nowadays, a trend that led merchants to examine the current payment method they offered and their current benefits with more scrutiny. Interest in emerging payment tools such as cryptocurrencies is rising as businesses and financial institutions (FIs) look for ways to stay competitive.

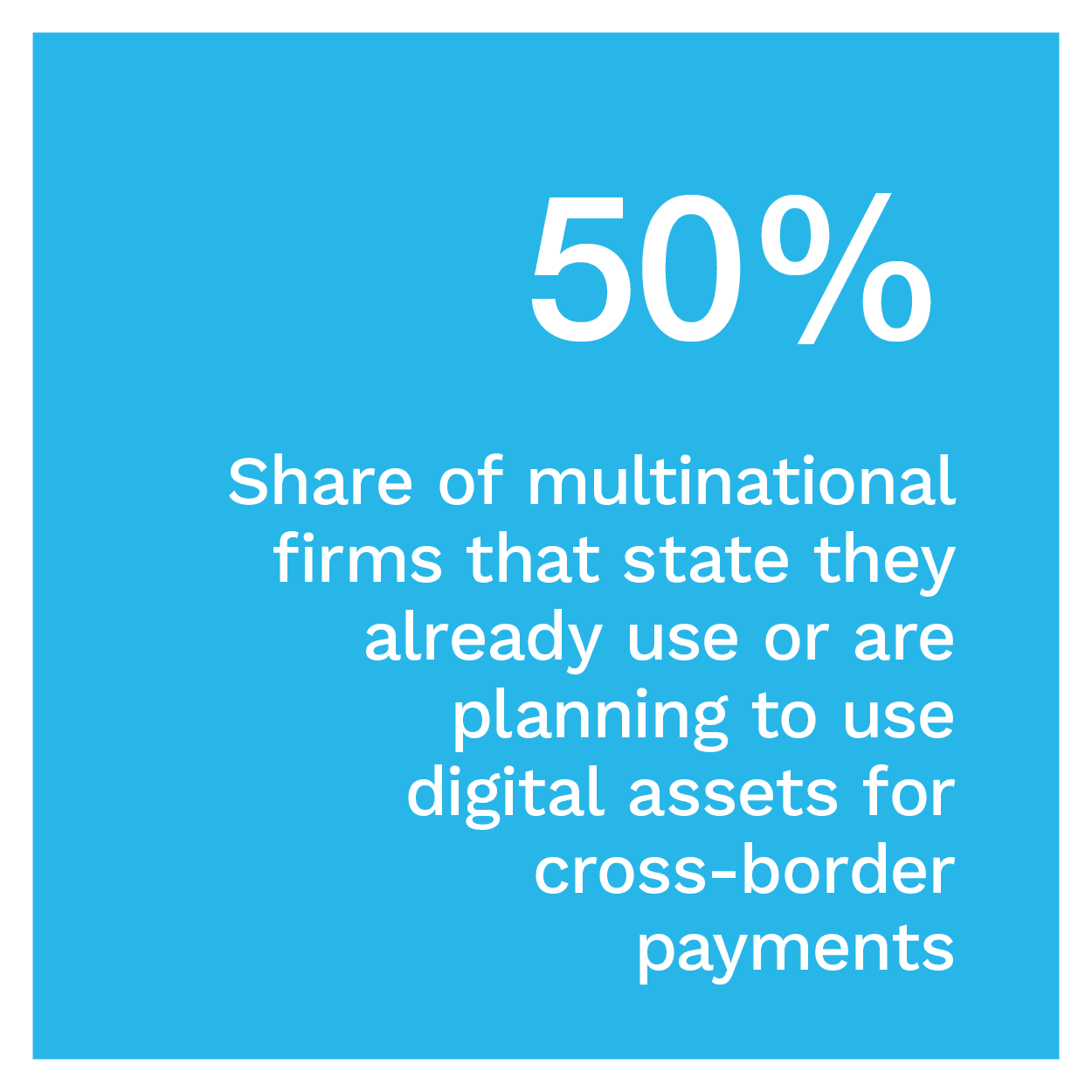

One recent report found 40% of companies in the Americas, Africa and the Middle East plan to tap digital currencies to make purchases within the next year, for example, indicating businesses are examining their use for business-to-business (B2B) as well as consumer-facing payment applications. Such currencies could represent an intriguing opportunity for companies making cross-border payments, as they could potentially lower the settlement time and ease costs for firms seeking to grow their global presence.

In The Cryptocurrency Payments Opportunity: Driving Crypto Adoption And Use Around The Globe, PYMNTS examines how attitudes and perceptions of cryptocurrencies are changing worldwide, as well as how businesses, banks and other financial players can take advantage of the opportunities these changes present. It will also analyze what tools and technologies may prove key for such entities to do so.

Around the Global Cryptocurrency World

Consumers and businesses are eying cryptocurrencies with more interest — investments in digital currencies among Americans have increased, for example, with one recent study finding 48% of investors in the country bought such alternative currencies in the first half of 2021. Younger consumers especially are growing increasingly intrigued by digital currencies. The report found 37% of investors 18 to 44 years old who have not yet bought digital currencies are either “very” or “somewhat” interested in doing so. This compares to just 19% of those over 60 years old who said the same, potentially indicating younger consumers are more comfortable with these alternative currencies.

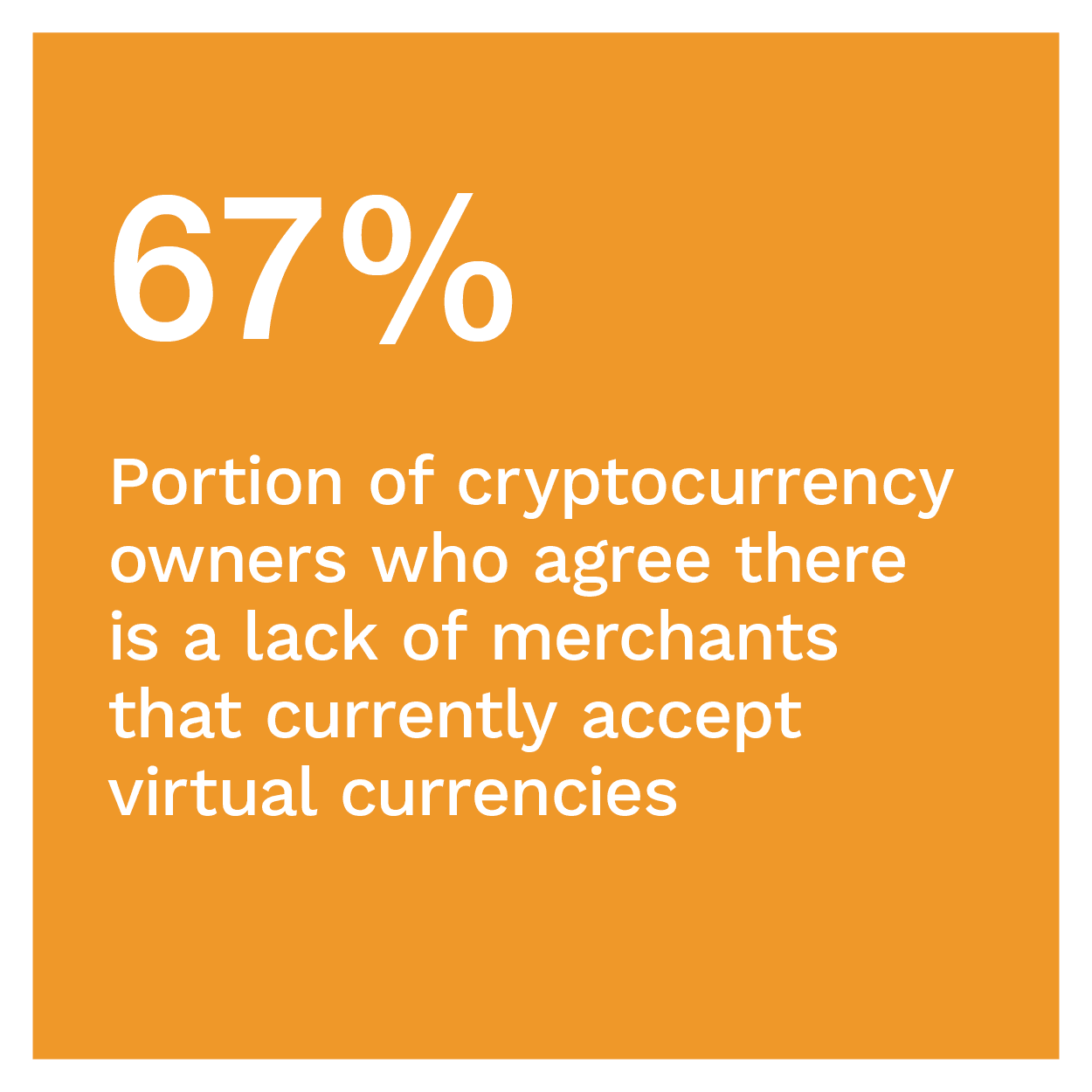

This bodes well for cryptocurrencies’ continued status as a digital asset, but acceptance of these currencies as a form of payment will require merchant and consumer support. Recent reports show cryptocurrency payments have been steadily rising, with more than $12 billion transferred over the bitcoin, Ethereum and Litecoin networks daily — representing approximately 1.5 million transactions each day. Transaction volumes are set to continue to expand, but this will require more businesses to trust and support these currencies. Sixty-seven percent of cryptocurrency owners agree that there is a current lack of merchants who accept payments via digital currencies, for example. Gaining merchants’ trust therefore appears key to ensuring future growth.

This bodes well for cryptocurrencies’ continued status as a digital asset, but acceptance of these currencies as a form of payment will require merchant and consumer support. Recent reports show cryptocurrency payments have been steadily rising, with more than $12 billion transferred over the bitcoin, Ethereum and Litecoin networks daily — representing approximately 1.5 million transactions each day. Transaction volumes are set to continue to expand, but this will require more businesses to trust and support these currencies. Sixty-seven percent of cryptocurrency owners agree that there is a current lack of merchants who accept payments via digital currencies, for example. Gaining merchants’ trust therefore appears key to ensuring future growth.

We’d love to be your preferred source for news.

Please add us to your preferred sources list so our news, data and interviews show up in your feed. Thanks!

Developments inside of the global cryptocurrency space are unfolding quickly as the attention on such currencies increases. Chinese authorities recently declared all cryptocurrency transactions and mining illegal within the country, for example — a declaration that saw bitcion’s value nosedive. The impact of China’s decision will likely reverberate throughout the global cryptocurrency market, and comes as the country’s central bank continues with its plans to develop a digital currency of its own within the nation. The bank announced in March it was testing out an electronic version of the Chinese yuan and also noted that both Bitcoin and ether were issued by “non-monetary authorities.” This indicates that central bank-backed cryptocurrencies or stablecoins may play a more noticeable role in the future global payments ecosystem.

For more on these and other stories, visit the Report’s News & Trends.

Apto Payments, Wirex Examine Global Cryptocurrency Payment Trends

Cryptocurrencies are gaining more attention from consumers, businesses and financial players worldwide, but there are still several challenges that must be met before digital assets can take their place in the payments mainstream. Digital currencies could allow both consumers and businesses to make smoother, swifter transactions — and they have especially intriguing potential for cross-border payments — but both individuals and companies must place their trust in this emerging payment type. PYMNTS spoke with industry experts including Matthew Goldman, vice president of sales and partnerships for crypto card issuer Apto Payments, and Pavel Matveev, CEO of multicurrency digital wallet and money transfer service Wirex, to understand current happenings in the cryptocurrency world and what must occur to open the way for future growth.

Deep Dive: How Financial Service Providers Can Create Smooth Cryptocurrency Payments to Win Businesses’ Loyalty

Thoughts surrounding cryptocurrencies and their potential applications appea r to be shifting in the public eye, changing from poorly understood payment tools on the outskirts of the financial ecosystem to emerging digital assets that could help to smooth out transactions in a number of use cases. One July PYMNTS report found two-thirds of individuals who currently hold cryptocurrencies bought them with the intent of using them to make purchases, for example. Businesses are also becoming more comfortable with such currencies, with more than 2,300 U.S. merchants now accepting Bitcoin as a payment method, for example. Examining cryptocurrencies’ potential benefits and how they can help to support them could provide financial service providers with key advantages for growth. To learn more about how supporting cryptocurrencies can help providers gain customers’ loyalty, visit the Report’s Deep Dive.

r to be shifting in the public eye, changing from poorly understood payment tools on the outskirts of the financial ecosystem to emerging digital assets that could help to smooth out transactions in a number of use cases. One July PYMNTS report found two-thirds of individuals who currently hold cryptocurrencies bought them with the intent of using them to make purchases, for example. Businesses are also becoming more comfortable with such currencies, with more than 2,300 U.S. merchants now accepting Bitcoin as a payment method, for example. Examining cryptocurrencies’ potential benefits and how they can help to support them could provide financial service providers with key advantages for growth. To learn more about how supporting cryptocurrencies can help providers gain customers’ loyalty, visit the Report’s Deep Dive.

About the Tracker

The Cryptocurrency Payments Opportunity: Driving Crypto Adoption And Use Around The Globe, PYMNTS and i2c Inc. collaboration, examines the latest trends and developments surrounding the cryptocurrency space, including how digital currencies can offer key potential benefits for consumer, B2B and cross-border payment use cases.