A dramatic rise in credit card debt over the last several years has pressured paycheck-to-paycheck consumers, with a disproportionate burden on those individuals and households that find themselves struggling to pay for the essentials of daily life, such as groceries.

That’s according to the PYMNTS Intelligence report “Average Credit Debt Hits More Than $7,000 for Financially Struggling Cardholders,” which found that financially struggling consumers — who live paycheck to paycheck with issues meeting their monthly obligations — carry a balance, on average, of more than $7,000 in credit card debt, which outpaces the overall sample average of about $5,000.

Experian found earlier this year that credit card utilization stood at 29%, even with the roughly $1 trillion in card debt held by households.

There may be further evidence that spending dry powder tied to cards may be strained. In data released Friday (Dec. 6) by the Federal Reserve — known as the G.19 report — overall credit across revolving lines (like credit cards) and non-revolving lines (which would be fixed-term loans like auto loans) increased at a seasonally adjusted annual rate of 4.5% in October.

But it is the revolving credit metrics that prove eye-popping. This line item increased at an annual rate of 13.9%, while nonrevolving credit increased at an annual rate of 1.1%.

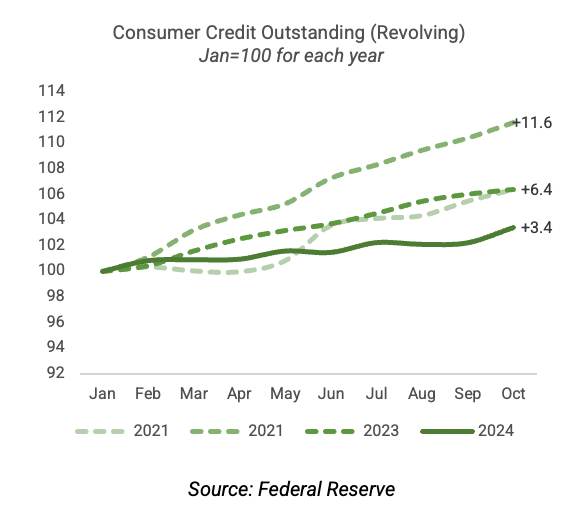

The October increase in borrowing in the revolving segment marked the strongest monthly uptick of the year and is the most notable surge seen since 2022 when consumers padded revolving credit by an annualized 22.8% pace.

The surge into the end of the year comes as overall balances in October were 3.4% above their January levels, which was below the 6.4% cumulative increase in 2023 and the 11.6% growth for the same period in 2022.

On a more granular level, many consumers — especially those having trouble paying their monthly bills — reported maxing out their cards regularly, PYMNTS Intelligence found. In an environment where roughly two-thirds of consumers live paycheck to paycheck, 25% of individuals said their outstanding balance increased through the past year. As balances increase, the debt that’s on the books, so to speak, inches ever closer to card spending limits.

On a more granular level, many consumers — especially those having trouble paying their monthly bills — reported maxing out their cards regularly, PYMNTS Intelligence found. In an environment where roughly two-thirds of consumers live paycheck to paycheck, 25% of individuals said their outstanding balance increased through the past year. As balances increase, the debt that’s on the books, so to speak, inches ever closer to card spending limits.

The pressures are most pronounced for cardholders living paycheck to paycheck with issues paying their bills, where the average limit stood at nearly $5,000, per PYMNTS Intelligence. That’s below the more than $10,200 average spending limit extended by card issuers to financially stable consumers.

As for the constraints, 41% of financially struggling cardholders often or always reach their card limits. PYMNTS Intelligence found that one-fifth of consumers in high earning segments, north of $100,000, said the same.

The most recently revised average APR for credit cards in the third quarter came to 21.8%, still the highest register of 2024 and above the 2023 and 2022 marks, when APRs averaged 20.9% and 16.3%, respectively. Sixty-month auto loan interest rates at commercial banks averaged a revised 8.4% in Q3, versus yearlong averages of 7.8% and 5.4% in 2023 and 2022.

There also are indications that returning to the proverbial well for more credit may be a tougher undertaking. The Fed said in a report on credit access that more consumers were applying for card limit increases, and at the same time, more credit applications were being rejected by banks.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More