Digital-only banks may fill the gap between traditional institutions’ low rates and Apple’s reported newcomer wrinkles.

As some of Apple’s first set of savings account users are learning, early adopters get the cachet of signing up early — along with the brunt of a new products’ wrinkles as it scales to market. Reports are emerging that some of these customers are having issues moving their money out of Apple’s much-heralded high-yield savings accounts within reasonable time limits, including taking weeks for transfers to go through.

Offered in a partnership with Goldman Sachs to Apple Card users, Apple’s savings account transfer delay could be due to additional review required by anti-money laundering and other security rules, banking experts say. This kind of additional review is common when large transfers are made from new accounts, which all Apple savings accounts are considered, since the product was only launched in April.

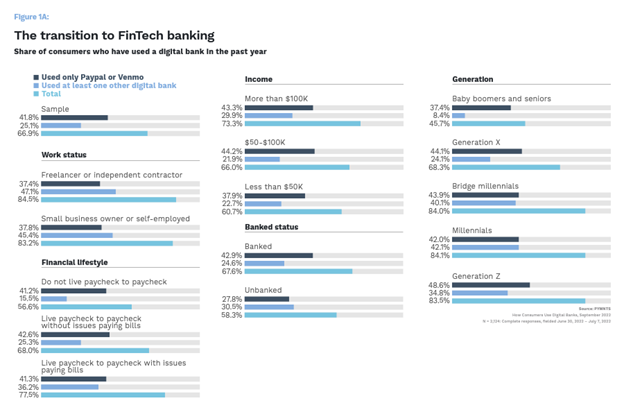

Simply put, the jump from traditional financial institution (FI) to non-bank focused FinTech may be too much for some. As evidenced in the PYMNTS collaboration with Treasury Prime, “How Customers Use Digital Banks,” the widespread adoption of digital-only banking alone has been a slow transition.

Although 42%, a significant share, of consumers have used platforms such as PayPal or Venmo in the year previous to being surveyed, that number drops to 25% when it comes to those using the services of a digital-only bank during the same time period. And despite Apple’s partnership with Goldman, there may still be hesitancy among certain customer segments about entrusting a business whose main purpose is other than banking with their hard-earned savings.

One of the main draws for the Apple savings account, of course, is the ultra-high 4.15% APY, which is more than 10 times the national average of 0.4%, per FDIC. As consumers continue to dip into their possibly dwindling savings, with 21% of paycheck-to-paycheck earners dipping into financial insecurity to cover costs, this rate may be very attractive to banking customers seeking assistance.

Those consumers may feel the temptation to instead test out a digital bank to get the best of both worlds — better money mobility and rates that more closely match Apple than the national average offered by traditional FIs. For example, established neobank Ally’s currently offered rate is 4%.

These higher rates could be one reason why these digital banks are doing better than some of their competitors. Ally in its Q1 2023 release noted total deposit gains of $11.5 billion year-over-year, and SoFi saw total deposits grow 37% during the same period. And these are just two examples.

Savings cushions are thankfully on a slow return to being repadded, consumers may continue to seek options to best passively grow their funds. For those hesitant to deposit in FinTechs, digital-only banks may already be the answer they seek.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More