Despite beating second-quarter revenue and earnings expectations in its first quarterly report since spinning out from Johnson & Johnson two months ago, Kenvue’s shares declined on Thursday (July 20).

The company, previously known as J&J’s consumer health division, also provided a positive sales outlook for 2023. However, during an earnings call, Kenvue CEO Thibaut Mongon pointed out that the consumer landscape remains uncertain, and the company anticipates that “market volatility will continue.”

Kenvue’s strong performance was driven by high demand for its brands, including Band-Aid, Tylenol, Listerine, Neutrogena and Aveeno. “This quarter was yet another proof point, showcasing the power of our portfolio,” Mongon said during the call.

With a 90% stake in Kenvue, J&J currently exercises significant control over the spin-off’s business direction.

During an earnings call on Thursday, Johnson & Johnson CFO Joseph Wolk revealed the company’s plan to reduce its stake in Kenvue through an exchange offer, which could begin “as early as the coming days.” This offer will allow J&J shareholders to exchange all or a portion of their shares for Kenvue’s common stock.

In its second-quarter earnings report on Thursday, J&J included Kenvue’s results.

Kenvue’s shares saw a decline of over 2% on Thursday. Despite a strong initial performance upon its public market debut in May, the stock has encountered challenges as investors express concerns about the company’s growth potential with its iconic brands, particularly due to consumer spending cutbacks.

Since its debut on the public market, Kenvue’s stock has experienced a decrease of more than 13%, leading to a decline in its market value to approximately $44 billion.

Kenvue by the Numbers

The company reported a net income of $430 million, compared to $604 million, during the previous year.

Kenvue is projecting sales growth of 4.5% to 5.5% for the year 2023. After its initial public offering (IPO) in April, Kenvue had said it anticipated annual sales growth to be around 3% to 4% globally through the year 2025.

Kenvue’s self-care unit, encompassing products for eye care, cough and cold and vitamins, achieved sales of $1.66 billion during the quarter, marking an increase of 12.2% compared to the same period last year, primarily driven by heightened demand due to a rise in cold and flu cases.

In the same quarter, skin health and beauty products contributed $1.15 billion in sales, reflecting a growth of 1.9% from a year ago. This category includes products such as shampoo, conditioner, hair loss treatments and skincare items.

Where Consumers Are Getting Self-Care Products

Consumers used to purchase their personal care products alongside their groceries at the supermarket. But there has been a notable shift toward digital channels.

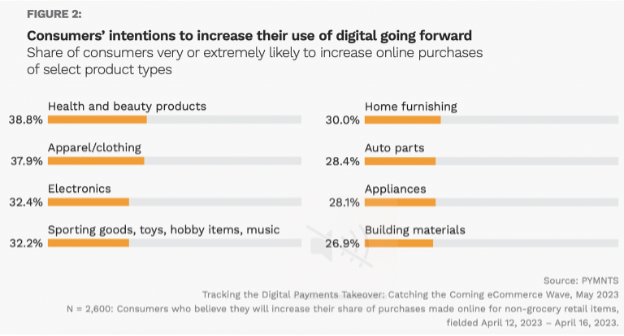

PYMNTS reported in June that according to findings from a study “Tracking the Digital Payments Takeover: Catching the Coming eCommerce Wave,” created in collaboration with Amazon Web Services, 39% of shoppers are very or extremely likely to increase online purchases of health and beauty products going forward.

Additionally, the study “Changes in Grocery Shopping Habits and Perception,” indicated that approximately half of all grocery shoppers have been reducing their purchases of personal and healthcare products from brick-and-mortar stores over the past few years. Furthermore, only one-third of the surveyed consumers reported buying these products more frequently in physical stores compared to digital platforms.

Read more: Grocers Losing Share of Health and Beauty Sales to eCommerce

In June, PYMNTS reported that Morgan Stanley predicted that by 2025, Amazon will have a 14.5% share of the beauty category, compared to Walmart’s projected 13% share.

PYMNTS has been monitoring the performance of both companies in the health and beauty segments, and in the most recent quarter, both Amazon and Walmart have been closely competing, with Amazon holding 5.1% of sales in this category and Walmart taking the lead with 5.9%.

During the pre-pandemic period of 2019, Amazon’s market share in the health and beauty segments was relatively low at 2.1%. Since then, however, it has consistently increased. In the latest report, there was a slight decline in Amazon’s share, partly due to a resurgence of in-store shopping as economies have reopened.

See: Amazon Trounces Walmart in Most Retail Categories — Is Health/Beauty Next?

Inflation’s Impact

While consumers are spending, they are still battling inflation.

The latest Consumer Price Index, published by the Bureau of Labor Statistics (BLS) on July 12, shows prices increased by 3% overall last month when measured on an annual basis. This shows a significant deceleration compared to the 4% increase observed in May and the peak of 9% approximately a year ago — but the pace of inflation remains higher than the Federal Reserve’s target of 2%.

Digging further into the data, several crucial metrics indicate signs of relief, particularly concerning essential goods. For instance, food prices remained stable in June for items consumed at home (groceries), as compared to May. According to the BLS, only two of the six major grocery store food group indexes experienced an increase over the previous month. Fruits and vegetables rose by 0.8% in June, while the cereals and bakery products index saw a 0.1% increase.

The cost of clothing saw a modest increase of 0.3% in June compared to May, maintaining a consistent pace observed over the past several months. The cost of shelter rose by 0.4% in June when compared to the levels of May.

Learn more: Economic Data Shows Inflation Still Threatens Discretionary Spending