Nineteen months into the COVID era, and the nation’s economic recovery continues to produce a mixed set of record results that are as complex as they are conflicting. With terms such as exceptional, resilient, inconsistent and insecure sharing the same space within PYMNTS’ latest Main Street Index (MSI) report, it is a telling indication of an uneven rebound that has created a chasm between winners and losers.

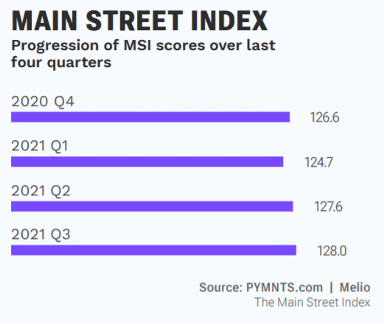

While the collective results of the latest MSI — which was produced in collaboration with Melio and tabulates 10 million data points back to 2004 — project that the benchmark hit a record high for the third quarter, deeper analysis of the numbers reflect how different pockets of Main Street businesses and industries are seeing a vastly different experience over the past year and a half, and will likely see continued discrepancies in the months and quarters to come.

“Despite a year of inconsistent performance, America’s SMBs have slowly approached recovery, and businesses that make up the MSI are expected to reach an all-time high [of] 128 in Q3 2021,” the study found. Those gains are, in part, due to the fact that “millions of America’s small businesses leveraged their agile operating structures to rapidly adopt new technologies as the pandemic made many of the processes that represented business as usual utterly impossible,” the research showed. Commonly used adaptations that allowed nimble businesses to engage local customers, expand operations and reach distant audiences via digital platforms included the uptake of user-friendly B2B payments platforms, as well as things like mobile-first delivery aggregator services.

These proactive innovations not only reflected the exceptional resilience of SMBs, the study found, but also fueled a recovery for many Main Street firms that started earlier and ran deeper than the economy at large.

The Haves, Have-Nots and Heartburn

While the collective rebound experienced by this critical contributor to the economy was solid, the PYMNTS data showed that ongoing uncertainty surrounding the threat from new COVID variants, as well as a number of key sectors that are lagging, are collectively clouding the forecast for Q4 and beyond.

For starters, the MSI growth rates, which hit an estimated 9.7% in Q2 2021 and were also well above the corresponding 6.7% jump in U.S. GDP growth, appear to have slowed to an annual rate of just 1.4% for the most recent period.

“Main Street businesses are enjoying a strong, if incomplete, recovery from the pandemic’s ongoing economic impacts,” the study found, noting that despite their resilience, “the recovery may not be secure” due to several key headwinds, including tepid employment level, volatile wages and other rising costs.

“Main Street businesses are enjoying a strong, if incomplete, recovery from the pandemic’s ongoing economic impacts,” the study found, noting that despite their resilience, “the recovery may not be secure” due to several key headwinds, including tepid employment level, volatile wages and other rising costs.

“The MSI’s drop over time may be due to several factors. First, inflation has and likely will continue to result in reduced purchasing power for SMBs,” the report found, with 41% of Main Street businesses citing negative impacts from vendor or supplier price increases. When combined with supply chain delays, business profit margins and sales are at risk.

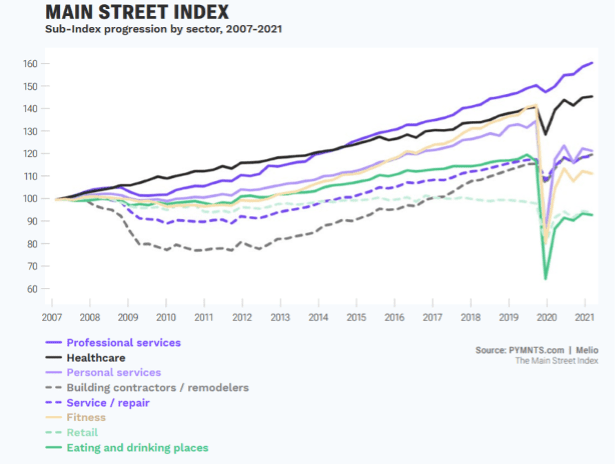

The unevenness of the recovery also continues to stand out, where half of the eight core components of the MSI are still seeing business levels that are below where they were before the pandemic, including restaurants, retail venues and fitness establishments, which were roughly 20% below where they were at the end of 2019.

On the upside, however, stand-out growth in the professional services and healthcare sectors continues to lead the way, driving the overall gains in the MSI to new heights.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More