The paycheck-to-paycheck economy is bifurcating as inflation rages and consumers fret over an uncertain future, with one group of customers who cannot spend, and another group who won’t spend.

In the middle of it all are the retailers, who look set to be squeezed this holiday season, and beyond.

Consumers tend to open up the wallets and purses when they feel flush, just as they pull back when they don’t. When they feel threats on the macro horizon, they cut where they can or must.

The latest PYMNTS study on what lies ahead, “Consumer Inflation Sentiment: Inflation’s Long Consumer Spending Shadow,” is sobering. Two out of every three consumers say they are “very” or “extremely concerned” about the outlook for the coming months. Eight in 10 consumers say inflation causes them to feel worried about the future. And 45% of consumers say the day-to-day struggle of paying bills has soured their view of the future.

In the meantime, about 60% of consumers say their income has stayed the same, at best, relative to price increases, or at worst has decreased.

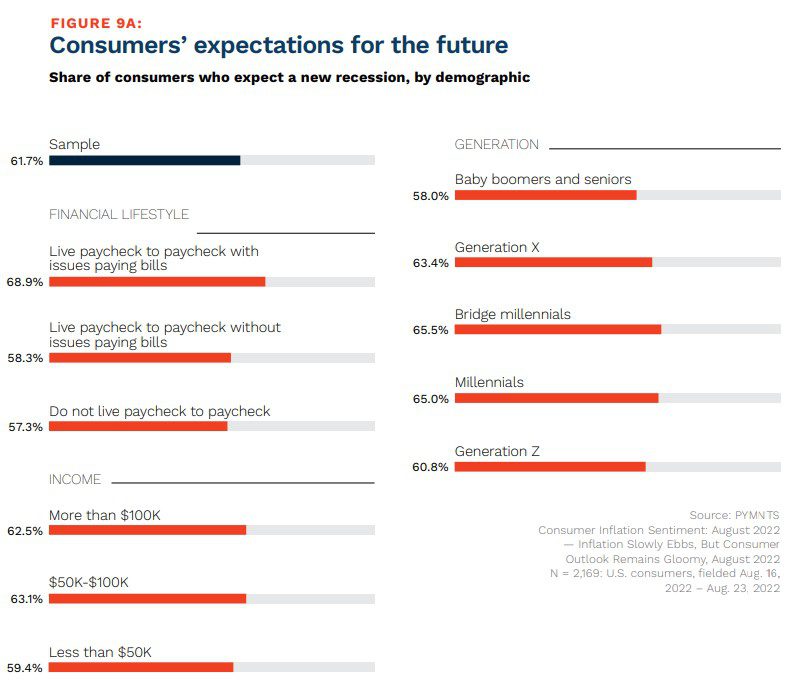

In the most recent Paycheck to Paycheck report, done in collaboration with LendingClub, PYMNTS found that pretty much everyone (and 62% of us live paycheck to paycheck) expects to see a recession. Of the consumers surveyed, 62% say so, and a majority (over 57%) of those of us who do not have issues paying the bills expect a recession.

The pullback is already clear: Companies running the gamut from Yum Brands to Nordstrom to PayPal have taken note in recent earnings reports that lower and middle income households have been cutting back on non-essential spending.

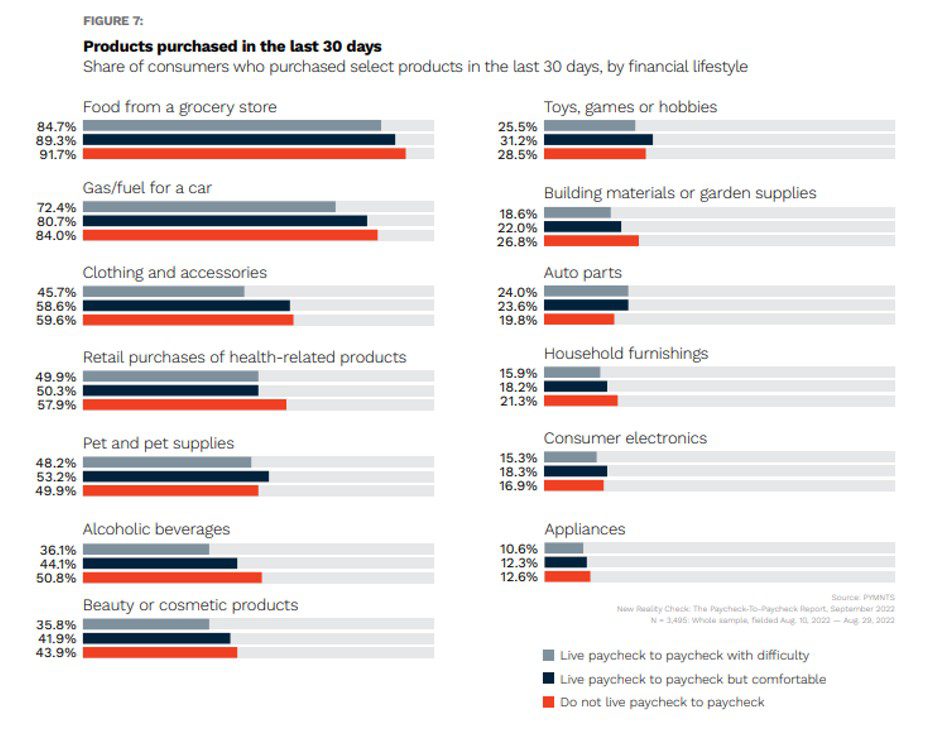

Last month, a previous PYMNTS Paycheck to Paycheck study showed that pretty much everyone, regardless of financial lifestyle, paid for food and gas; however, only about a quarter paid for toys, games or hobbies. Those categories are, of course, the most discretionary of purchases, and the easiest to throttle back. The strikingly similar pattern across different income levels show an unwillingness, or inability, to spend money on these products.

The shaky consumer confidence is showing up in other data points, too. Credit card debt’s slowing pace hints at renewed caution, even when, last summer, the Fed estimated that there was $3.3 trillion in untapped lines. The latest data show total revolving credit grew by 8.7% when the pace had been in the double digits, and the read-across is that we’re not as bold whipping out the plastic as we once were.

PYMNTS reports have shown that paycheck-to-paycheck consumers are three times as likely to revolve credit card debt and carry higher monthly balances overall. Among cardholders living paycheck to paycheck, 34% of those without issues paying monthly bills and 47% of those who struggle to pay their bills “always” or “usually” have a revolving balance. Just 12% of consumers not living paycheck to paycheck “always” or “usually” revolve credit — and the odds are that they may not be about to start now, with card interest rates at new highs.

Consumers, increasingly cautious about what they can (or should) spend in the coming months, look set to cast a pall over merchants.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More