Individuals and households are paying down at least some of their debt — bringing the “headline” consumer credit number down a bit.

But the devil’s in the details, and the details show that credit card debt continues to mount.

To that end, the Federal Reserve’s latest report Friday (Oct. 6) shows that in August, overall consumer credit decreased at a seasonally adjusted annual rate of 3.8%.

Nonrevolving credit decreased by an annualized rate of 9.8% after several months of increases, coming in at a bit under $3.7 trillion, down about $30 billion month over month.

Nonrevolving debt includes student loans and auto loans.

Along with those pay downs, though the latest granular data for August did not disclose student debt levels, we’ve detailed in recent coverage that for those borrowers shouldering those loans, the monthly repayments would pinch annual disposable income by several percentage points.

In the meantime, consumers are wielding their cards more often, and revolving credit — which includes credit card debt — soared at an annualized pace of 13.9%. Revolving debt in August stood at nearly $1.3 trillion, up about $15 billion month over month.

In other words, at least some of the debt that’s being paid down is being offset by loading up on credit cards, where the rates are variable and where the latest Fed numbers on annual percentage rates on those cards have topped 22%, up from 16% during the pandemic.

Trying Just to ‘Get By’

By taking on relatively more expensive debt that immediately adds to monthly expenses, consumers are pressuring their disposable income right into the holiday shopping season. PYMNTS Intelligence in recent days already shows that the holidays already create financial stress for consumers — and more than a third of them use credit products to “get by.”

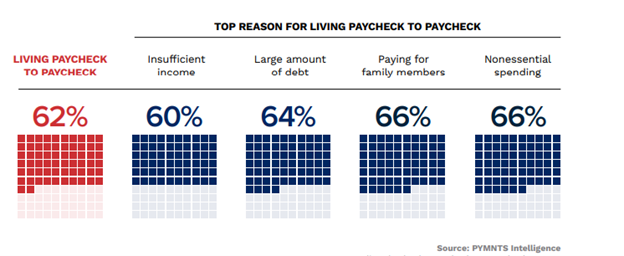

The chart below details that most consumers say insufficient income and high debt burdens are the key reasons they live paycheck to paycheck.

Those pressures may be exacerbated by the fact that, in the meantime, wage growth is slowing, which means that any boost in paychecks is not likely to keep pace with the additional credit card-related interest payments. In separate economic data released Friday by the Bureau of Labor Statistics, average hourly earnings were up 0.2% in September month over month, in line with the same gains in August. The annualized increase in wages stood at 4.2%, which is down from 4.3% in August.

In the meantime, inflation tied to core items such as food is running at roughly the same pace as wage growth — and in August, per the latest CPI data, outpaced wage growth significantly, if all line items are factored in, such as energy.

The data covers the waning months of summer and the beginning of fall. But it is November and December that can be make or break for so many households. Consumers surveyed by PYMNTS in the latest paycheck-to-paycheck report state that December and November are among the most financially stressful months — beyond the holiday events and the gift-giving. As many as 32% of consumers cited utility bill cost changes as a key reason for financial stress, with 13% saying it is the top reason. And another 13% of consumers have said that year-end tax payments contribute to financial stress.