A downward revision to previously released job market data might be enough to spur interest rate cuts.

But the damage to the paycheck-to-paycheck economy — to all consumers, in fact, and especially to the most vulnerable, low-income consumers — may have already been done.

The U.S. Bureau of Labor Statistics (BLS) said Wednesday (Aug. 21) that the United States economy employed 818,00 fewer individuals (equating to 0.5% of all nonfarm employment) than what was initially reported.

Revisions are a mainstay of economic data. Each year, the Labor Department revises its data on jobs, which paints a clearer picture of what happened, and whether 12 months’ worth of gains, losses and the resulting snapshot of the economy has proven accurate.

Wednesday’s data is preliminary. The final stats won’t be released until early 2025.

According to the revised data, the service industry was the hardest hit, as employment was recalculated downward by 358,000 roles, followed by leisure and hospitality jobs, revised downward by 150,000 positions. To get a sense of the revision, consider the fact that, as the BLS noted, “For national [Current Employment Statistics (CES)] employment series, the annual benchmark revisions over the last 10 years have averaged plus or minus one-tenth of one percent of total nonfarm employment.”

The data lowered the monthly job additions seen in the U.S. economy over the year that ended in March to 174,000 from 242,000.

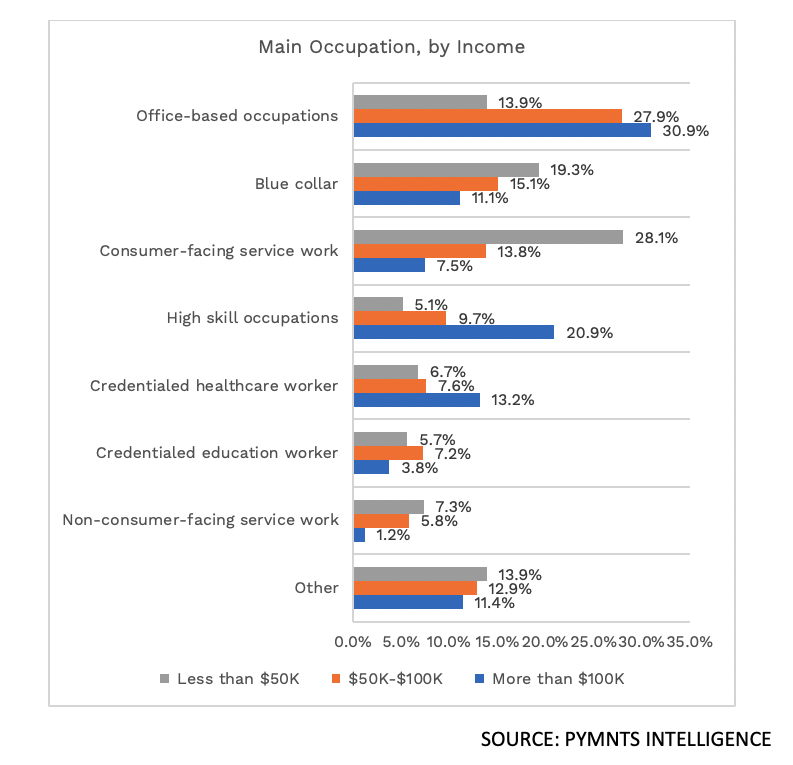

PYMNTS Intelligence data shows that low-income employees tend to work in service sectors such as nursing or hospitality. Roughly a third of consumers earning less than $50,000 annually work in consumer-facing or non-consumer-facing service roles.

The Federal Reserve bases its policies on BLS and other such data. A hot job market portends inflation, and thus, higher interest rates. A cooler employment landscape implies that price increases may be slowing (and pressures on households might impact spending, which impacts gross domestic product), so rates tend to move lower.

The Fed may decide to cut interest rates as soon as next month. In the meantime, the higher cost of debt, perhaps needlessly too high, dented the nation’s pocketbook overall.

Each quarter-point of interest rates — where the federal funds rate is the benchmark by which all manner of debt is calculated in terms of prime rates and financing costs — winds up making the cost of borrowing more expensive, by billions of dollars. Almost all credit card debt is variable, so the financial impact of rate hikes can be keenly and swiftly felt, with a vast divide between the consumers who have the funds and financing to absorb the shock waves and those who do not.

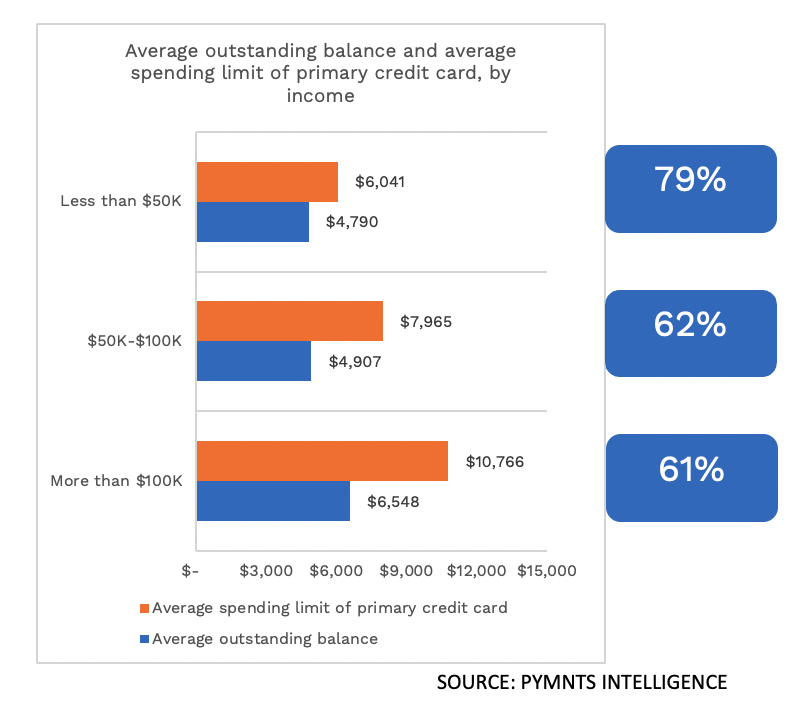

“Low” earners have tapped out much of their spending power, with 79% of the available limits used. They also have roughly $5,600 in savings, compared to as much as $16,000 for individuals and households earning more than $100,000 a year.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More