T.S. Eliot wrote that the world would end not with a bang but a whimper.

It may be the case that the unstoppable wave of consumer spending may end that way too, and not with a full-fledged slamming on the brakes — a wallop that hits merchants all at once.

We may see a pulling back on the purse strings that accelerates as consumers find savings can’t sustain that spending while debt adds additional pressures.

And it may be the lower income consumers who offer the clearest indication of what’s to come for merchants, particularly in discretionary spending sectors such as beauty and apparel.

As PYMNTS Intelligence has found, and as emphasized in a recent column by Karen Webster, 10% of U.S. consumers have an annual income of $50,000 or less and live paycheck to paycheck and already have issued issues paying their monthly bills. The challenges to this segment represent a challenge to keep 8% of all consumer spending going.

As for the obligations, wrote Webster it’s “not that they won’t eventually pay them, but each month becomes a game of bill-pay roulette as consumers decide which biller can wait a little longer. Interestingly, of all household bills, utilities, insurance, mobile phones and credit cards make the monthly cut — the billers that carry a big downside risk if not paid,” she wrote. But (stretched) funds spent on those necessities translate into less money to be spent elsewhere.

Advertisement: Scroll to Continue

Lower-Income Consumers Falling Behind

A few signals are coming from earnings season thus far, particularly from the banks. Most of the payment networks have yet to report, but the likes of JPMorgan Chase and Wells Fargo and Citi have noted year-over-year rises in delinquency rates on cards and auto loans, with some sequential improvement. We note that delinquency rates indicate some of the juggling act references above — the obligations have not been written off yet.

JPMorgan’s earnings supplementals indicate that, as far as delinquencies are concerned, the 30-day delinquency rate, at just under 2.1% in the second quarter, was higher than the 1.7% seen in the same period last year, but was better than the 2.2% seen in the first quarter. Overall card spending has been positive, but management has called out weakness has been seen among the lower-income cohorts.

During Citigroup’s earnings call, management pointed to the fact that individuals with higher credit scores continue to use their cards as lower FICO consumers are falling behind.

CEO Jane Fraser said that Citi sees “differentiation in the credit segment, with the lower income-customers seeing pressure,” and CFO Mark Mason said that “lower FICO band customers are seeing sharper drops in payment rates and borrowing more as they are more acutely impacted by high inflation and interest rates.”

The 90-day delinquency rate was 1.1% in the most recent period, up from 0.8% last year and down from the 1.2% in the first quarter. Wells’ filings indicate that card loans 30+ days delinquent stand at 2.7%, up from 2.3%

Other loan segments are seeing some uptick in delinquency rates, where, as JPMorgan’s filings reveal, the delinquency rate was 1.12% in the most recent quarter, up from a bit more than 1% in the first quarter and up from 0.9% last year.

We noted that “most” of the payment networks had not reported yet — Visa and Mastercard are still on tap. But Discover reported earnings last week, and as card sales were down 3%, we’re seeing what CFO John Greene said is a trend that “see[s] a cautious consumer evidenced by less card member spend with lower income households being most affected,” said the CFO.

The data show that in the card portfolio, the 30-day delinquency rate was 3.7% in the June quarter, up from 2.9% a year ago. The net principal charge-off rate was 5.6%, up from 3.7% last year. Greene said losses should “peak and plateau” later this year. The supplementals reveal that net charge-off rates, overall, should be in the range of 4.9% to 5.2%. The company’s latest annual filing details that 80% of its card business is tied to consumers with FICO scores of 660 or above, the remaining basket falls below that level.

PYMNTS Intelligence reported here that significant percentages of younger consumers — across millennial and Gen Z cohorts who are unmarried, or married and don’t live with children at home, or single with children — fall into the “less than $50,000” income strata.

These are the same segments that are pressured by living paycheck to paycheck, and where our data show that only about 22% bought clothing and roughly a third bought health and beauty products, trailing highly populated households with kids, where those items may be top of mind, wear out, need to be replaced. These are the merchants that may see pressure as lower income consumers pare back spending, and families trade down/trade off.

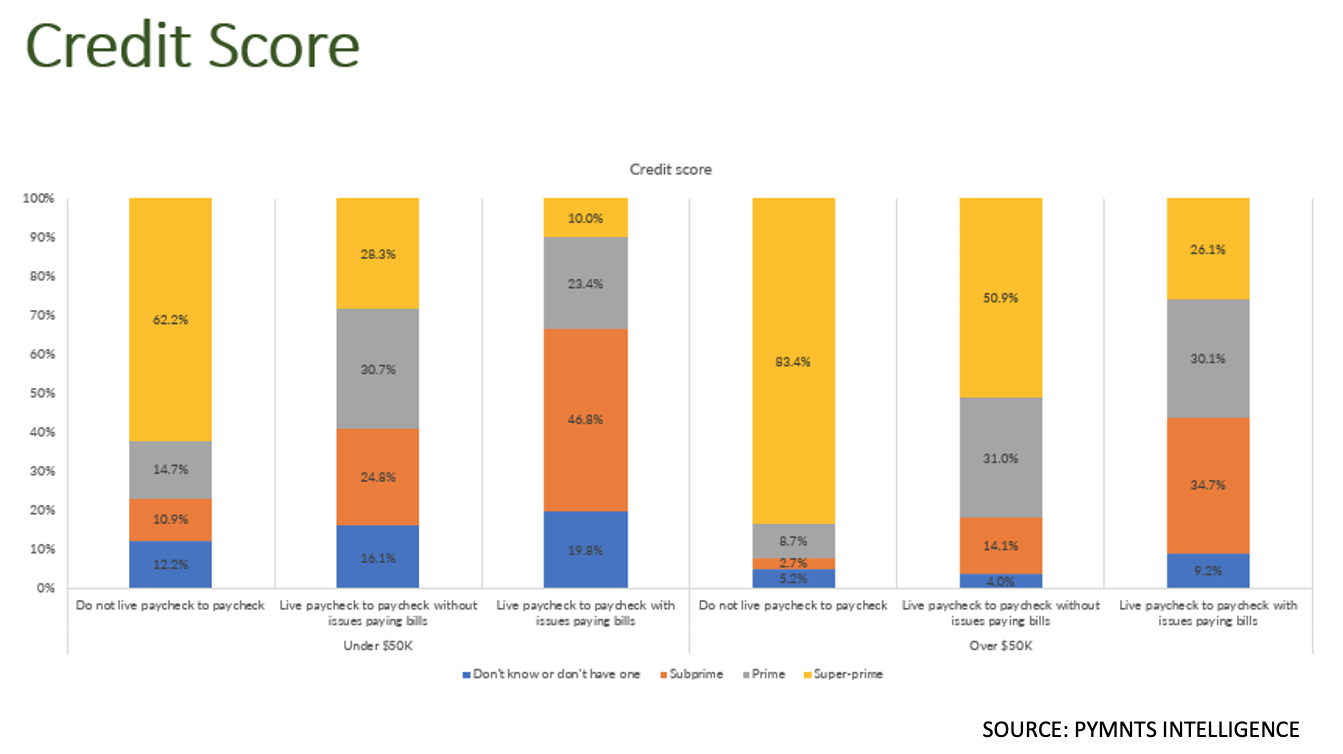

The above chart, as compiled by PYMNTS, indicates that about half of consumers with issues paying their bills fall into the subprime category, which is the lower FICO band that is being called out on earnings calls as being pressured.

The deposit trends indicate that savings may not help much here. JPMorgan reported that its consumer banking deposits were down 3% from the first quarter, and down 9% from a year ago.

PYMNTS Intelligence data show that the readily available savings — across all income levels, but most pronounced among lower-income consumers — is hardly a buffer against shocks or, perhaps, to pay down cards or sustain spending. For the paycheck to paycheck consumer struggling with and juggling the monthly obligations, the tally’s about $1,700.

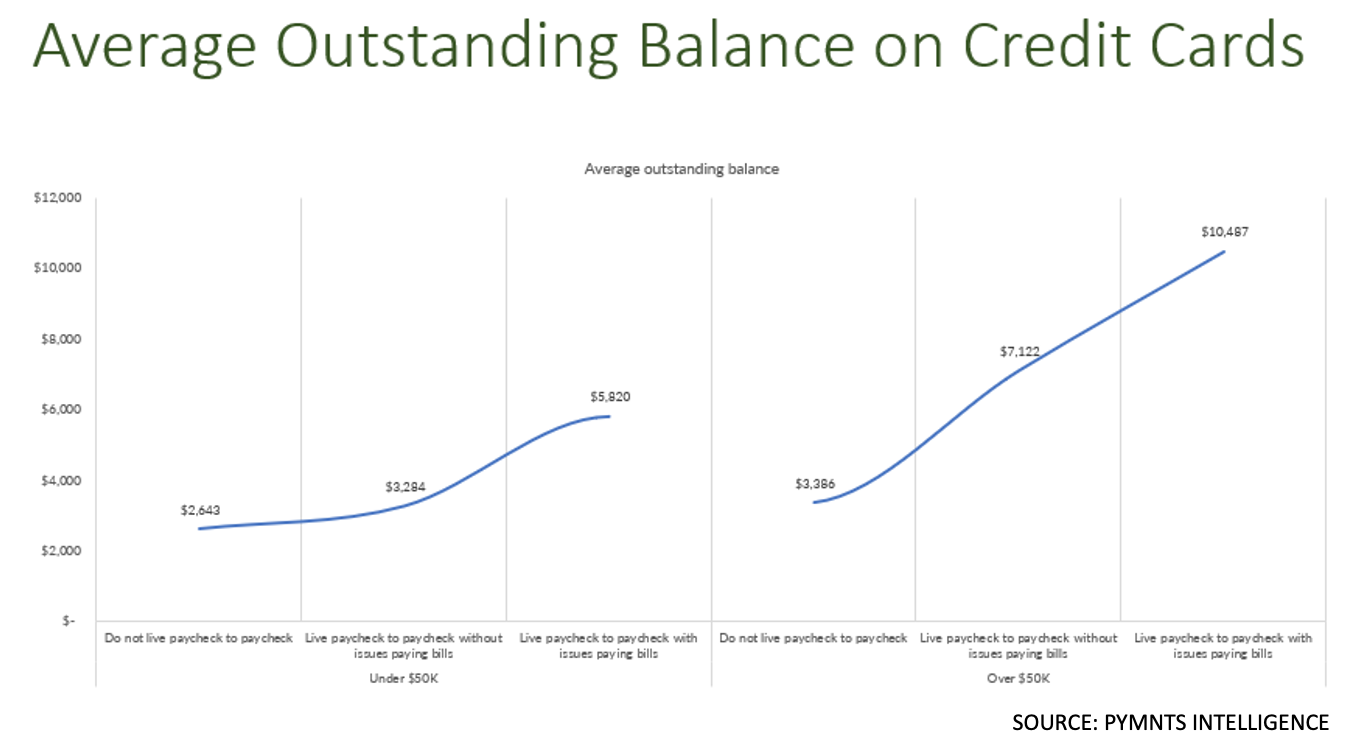

These same consumers carry an average outstanding balance of more than $5K — and even for relatively well-off households, the balance is even higher, at more than $10K. The juggling act looks more like a tightrope.