For the jobs market, this is the way the year ends — not with a whimper but a bang.

Data released Friday (Jan. 10) by the Bureau of Labor Statistics noted the addition of 256,000 nonfarm payroll jobs in December. The latest number was significantly above economists’ forecasts for about 155,000 jobs to be added.

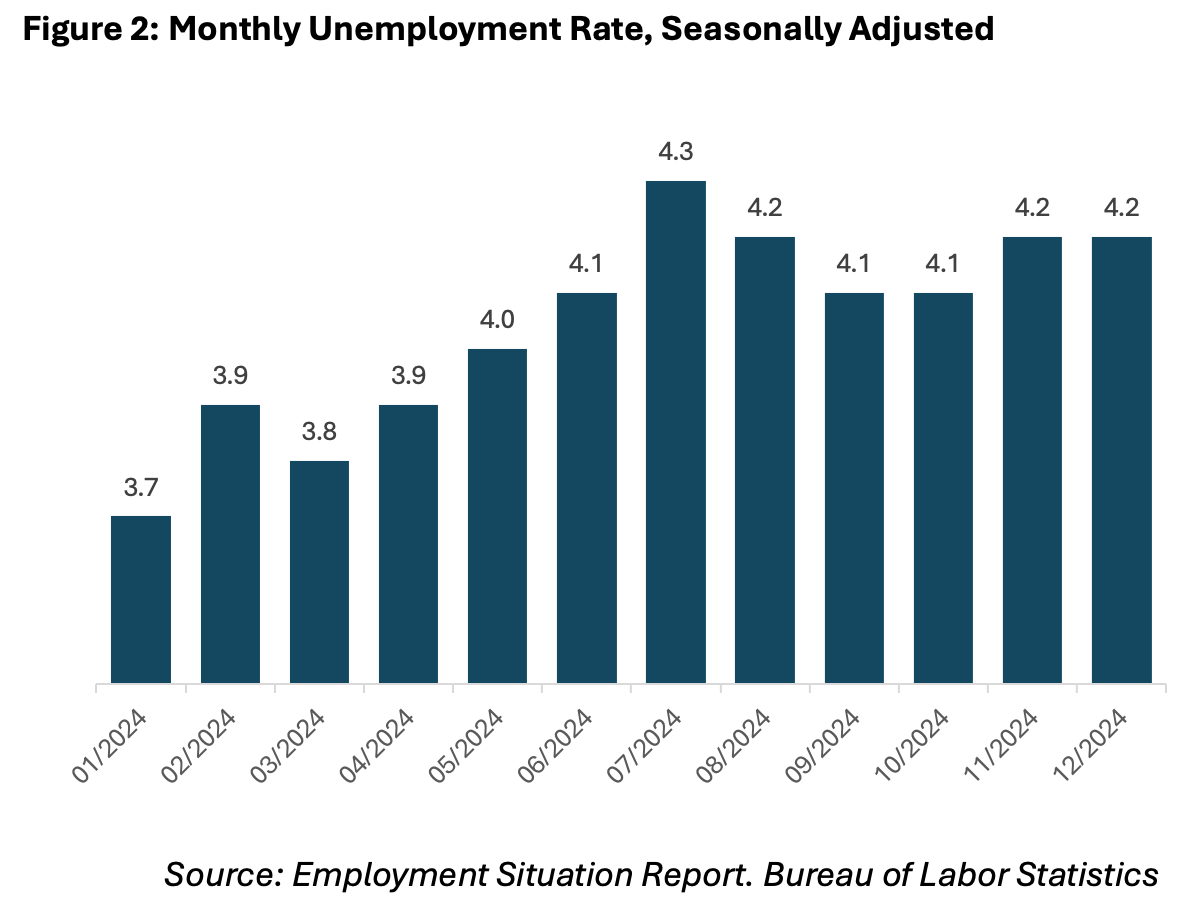

The unemployment rate remained steady at 4.2%, a percentage that has been relatively consistent for the past seven months, though above recent troughs of about 3.7% that had been measured at the beginning of the year. Gains in sectors like healthcare, government and retail trade were highlights of the latest report, while wage growth continued at a moderate pace.

Average hourly earnings for private nonfarm payrolls rose by 0.3% to $35.69 in December, reflecting a 3.9% annual increase.

The pace of gains in the labor market, overall, is moderating: In 2024, payrolls expanded by 2.2 million jobs, averaging 186,000 per month — a slower pace compared to the 3 million jobs added in 2023.

It may be the case that the boom in December has a two-fold effect: Encouraging workers to mull job switching as 2025 is in its infancy and to keep spending — on the assumption that wages will keep at least some measure of growth.

But there’ll need to be a clearer picture of where things stand. In earlier coverage this week, Job Openings and Labor Turnover Survey details noted that for November showed that job openings were up for the month, standing at 8.1 million roles, up from 7.8 million in October. The 3.3% growth was primarily driven by new openings in the financial activities and professional services sectors. But hiring slowed a bit — indicating that filling those roles has been taking some time.

There’s a fly in the ointment, perhaps, given the fact that the robust labor market data from December now puts some of the Fed’s path toward cutting interest rates in less-than-certain territory. That means, too, that inflation worries may impact spending. Also on Friday, the University of Michigan’s Consumer Sentiment Index, for January, was 73.2, down from the December reading of 74. Expectations for inflation were notably higher, at 3.3%, where that rate had been projected last month to be 2.8%.

In remarks that accompanied the release, Surveys of Consumers Director Joanne Hsu said, “The current reading is the highest since May 2024 and is above the 2.3-3.0% range seen in the two years prior to the pandemic. Long-run inflation expectations rose from 3.0% last month to 3.3% this month. This is only the third time in the last four years that long-run expectations have exhibited such a large one-month change. For both the short and long run, inflation expectations rose across multiple demographic groups, with particularly strong increases among lower-income consumers” and we’d note that the spending picture has now just become just a bit murkier.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More