The threat businesses face from financial crimes has never been greater.

Nearly three-quarters of compliance professionals in a survey reported filing more suspicious activity reports related to financial crimes in 2020 than in 2019, and 69% said better fraud detection would have the most impact on reducing losses. More than half also cited cybersecurity as their No. 1 vulnerability.

Financial cybercrime in particular has surged alongside the accelerated shift to remote work. The FBI received nearly 800,000 internet crime reports in 2020 — a 69% increase over 2019. Financial crimes accounted for the majority of cases and also were the most costly, with victims losing $1.8 billion to business email compromise (BEC) alone. Other research indicated that eCommerce merchants will lose over $20 billion to payments fraud this year — 18% more than in 2020 — and this trend will worsen in the years ahead.

New PYMNTS research showed that banks and other financial institutions (FIs) are more frequently implementing artificial intelligence (AI) and machine learning (ML) in the fight against fraud. The following Deep Dive examines the importance of AI and ML technologies in fraud monitoring and prevention, including the top benefits they offer over legacy methods. It also highlights the gap in these tools’ adoption between larger and smaller firms and the perceived obstacles that may be keeping more firms from jumping on board.

AI and ML’s Anti-Fraud Capabilities

Online fraud represents one of the greatest challenges that businesses face in the digital space. A 2020 PwC survey of more than 5,000 firms found that 47% had encountered fraud attempts in the last 24 months, with known fraud losses totaling $42 billion. A global study of more than 2,500 fraud cases from the Association of Certified Fraud Examiners found that businesses suffered median damages of $125,000 per case in 2020, with 25% losing upward of $600,000.

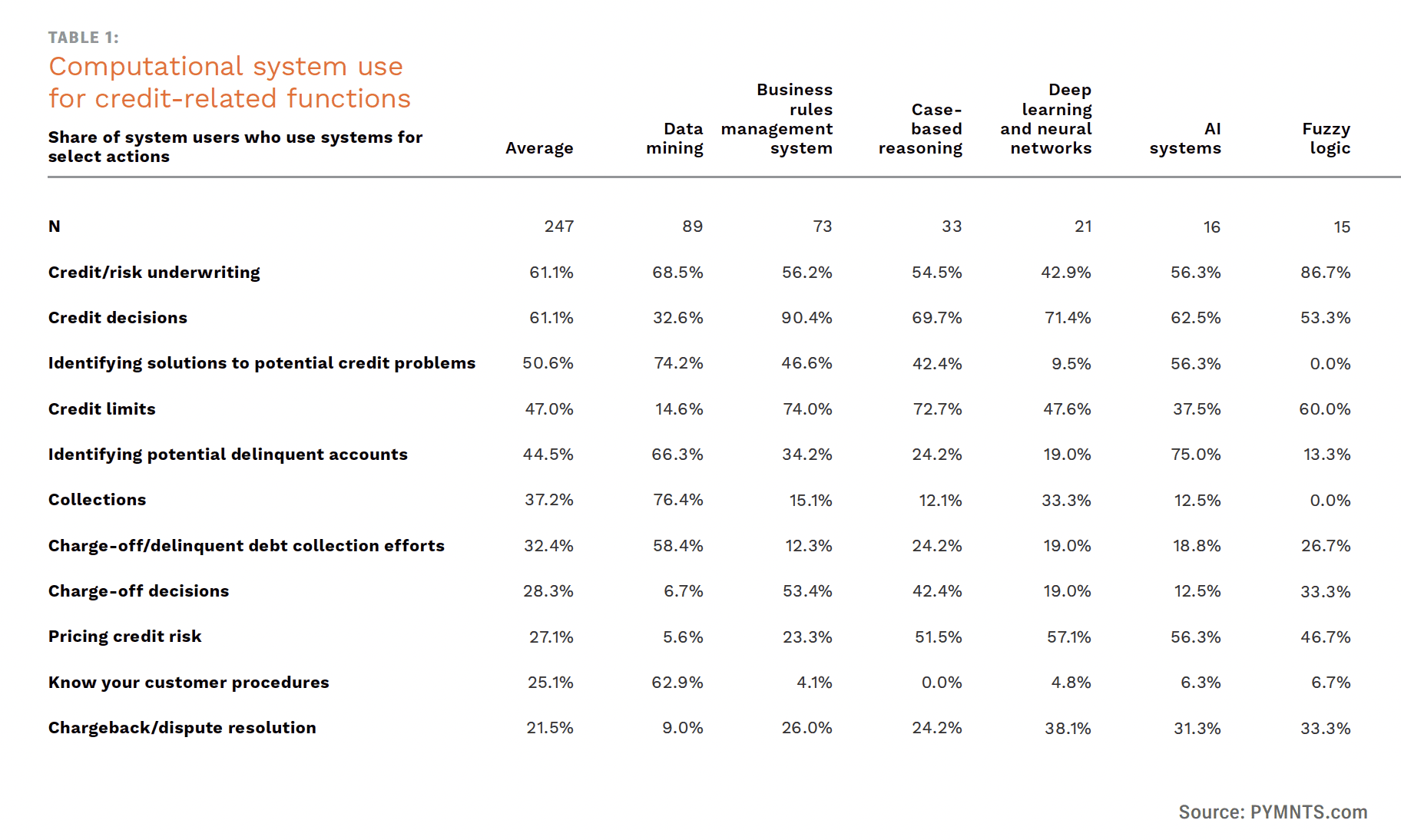

FIs have traditionally used rules-based systems along with manual review for fraud detection. Fraudsters’ growing sophistication and the difficulty of creating rules for every anomalous transaction challenge this method. False positives — the flagging of legitimate customers as fraudulent — and fraud going undetected due to high data volumes are two of the thorniest problems plaguing rules-based systems. AI and ML, on the other hand, lean on the much more effective principle of detecting deviations from standard activity.

ML specializes in spotting outliers in large data sets and in “learning” and adapting to new patterns of input. Banks can deploy the technology for both supervised and unsupervised learning, which can bolster their fraud-prevention efforts in different ways. Supervised learning enables FIs to receive real-time insight into their fraud analytics, helping them better tailor their solutions to eliminate false positives based on fraud investigators’ experiences. Unsupervised learning, meanwhile, allows banks to harness ML to root out potential fraud scenarios that are not outlined within the existing analytical framework.

AI and ML systems thus excel at fraud prevention because they can identify subtle trends in savvy cybercriminals’ constantly evolving approaches, as they are increasingly using AI themselves. This explains why more industry players, governments and auditors alike are adopting AI and ML for fraud prevention in place of their old rules-based systems.

Benefits and Barriers to AI and ML Adoption

Major payments players such as American Express and Visa have deployed highly advanced AI-based systems for fraud monitoring and credit risk and continue to invest in their AI programs. Synchrony has achieved an over 90% accuracy rate with its AI anti-fraud ecosystem as well. A PYMNTS study polled FIs in the U.S. about their use of AI and other advanced technologies, and the results confirm rapid growth in AI system adoption, which roughly tripled between 2018 and 2021, from 5.5% to 16% of respondents. This aligns with broader industry trends and, while still low, suggests that most firms could be using AI solutions within a few years.

The FIs surveyed that had already adopted AI identified benefits either directly or indirectly related to fraud monitoring and prevention as the top five benefits of the technology.

Eighty-one percent cited being alerted to fraud before it happens, 75% cited the reduction of false positives and 56% specified the reduction of payment fraud as key outcomes of their AI systems — all of which are core anti-fraud functions. The other top two key benefits — improvement of operational efficiencies (81%) and improvement of customer satisfaction and experience (63%) — also relate indirectly to effective fraud prevention because an accurate and seamless AI-based system will increase efficiency and keep the customer experience frictionless.

Only the larger FIs surveyed tended to already have adopted AI systems, however. A total of 79% of FIs with more than $100 billion in assets said they were using AI versus just 4.5% in the $25 billion to $100 billion range, and none were using it among those with less than $25 billion in assets.

Another PYMNTS study highlighted why some firms have not implemented AI systems. Seventy-two percent cited regulatory problems, making it the most common worry, followed by the complexity of AI (59%) and its higher data management costs (59%). These findings identify the key concerns — and perhaps misperceptions — that AI and ML service providers should seek to address in their messaging to potential clients.

Many smaller firms have plans to start using AI, however. Ninety-nine percent of firms said they either already have invested in AI systems (21%) or plan to within three years (72%), most of the latter within 12 months (57%).

These strong results suggest that AI systems have reached a tipping point in terms of interest among FIs, even if some do not implement the technology as quickly as they would like. AI and ML offer major advantages over rules-based systems for banks and other institutions in the fight against fraud, including fast and accurate identification of fraud before it occurs, reduction of false positives, elimination of manual labor costs and improvement of the customer experience. Companies wishing to remain competitive in the rapidly evolving fraud landscape will want to invest in these systems without delay.