The speed that makes instant payment apps such as Zelle and Venmo popular also makes them attractive tools for fraudsters. Bad actors defrauded nearly 18 million Americans through digital wallets and peer-to-peer (P2P) payment scams in 2020, for example.

There is currently much debate in the United States on who bears financial liability when instant payment fraud occurs. In the United Kingdom, the Payment Systems Regulator (PSR) intends to move forward with plans discussed last year to create regulations around mandatory reimbursement of losses from authorized push payment fraud.

This edition of the “Digital Fraud Tracker®” explores the need to recognize instant payments fraud and fight it head-on, as well as what banks and companies can do to protect their clients.

Around the Digital Fraud Space

In response to a report by Sen. Elizabeth Warren, D-Mass., highlighting fraud on Zelle, the American Bankers Association, Bank Policy Institute, Consumer Bankers Association and The Clearing House cautioned that overregulation  and expanding the current liability framework would diminish the value and benefits that Zelle offers consumers. In response, Early Warning Services, the network owner and operator of Zelle, released a statement that more than 99.9% of transactions conducted through Zelle occurred without fraud.

and expanding the current liability framework would diminish the value and benefits that Zelle offers consumers. In response, Early Warning Services, the network owner and operator of Zelle, released a statement that more than 99.9% of transactions conducted through Zelle occurred without fraud.

Merchants can no longer risk offering online experiences that fall short of customer expectations. Consumers who face negative experiences such as fraud are less likely to use the same merchant again. Smooth online experiences become even more urgent, considering 56% of buyers said they would share bad experiences with colleagues and co-workers, causing potential loss of clients and revenue in the future.

For more on these and other stories, visit the Tracker’s News and Trends section.

Axos Bank on Mitigating Instant Payments Fraud

Instant payments are just that — instant and irreversible. Once made, there is no getting that money back. It is vital to ensure they are processed correctly and that customers are educated on making these payments safely.

In this month’s Insider POV, PYMNTS spoke with Christian Santaniello, senior vice president and head of commercial deposits and treasury management at Axos Bank, about ensuring instant payments are safe and secure.

Responding to Flourishing Instant Payment Fraud

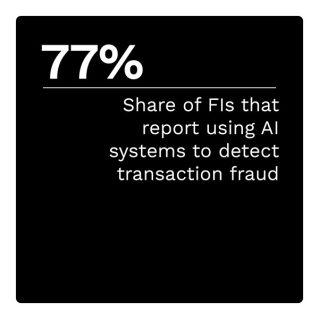

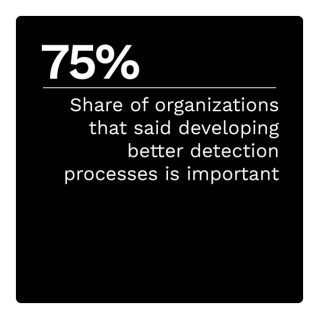

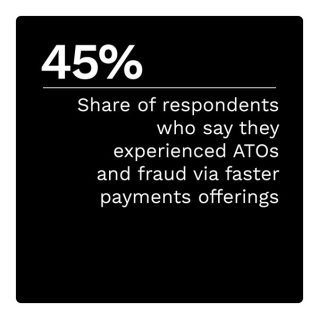

As the use of these faster payments has increased and become more mainstream, so have fraud-related problems. Twenty-three percent of P2P platform users have sent funds to the wrong person, and 15% have been victims of at least one scam, for example.

This month’s PYMNTS Intelligence examines the advanced technologies and authentication tools that firms can leverage to fight instant payments fraud.

About the Tracker

In the “Digital Fraud Tracker®,” a PYMNTS and DataVisor collaboration, PYMNTS examines instant payments fraud trends and how firms can mitigate this type of fraud.