Top Performing financial institutions (FIs) understand that success may not always be about speed, but timing is often paramount. In fact, they make the timing of their product rollouts a crucial part of their innovation strategies.

Top Performing financial institutions (FIs) understand that success may not always be about speed, but timing is often paramount. In fact, they make the timing of their product rollouts a crucial part of their innovation strategies.

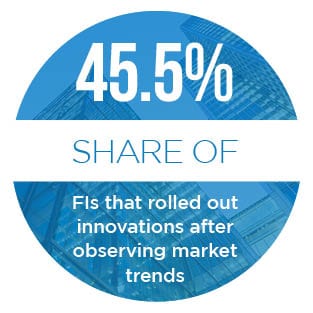

Only after observing their competitors’ missteps do they fully commit to the rollout of their innovations. As much as 53.3 percent of the top innovators in the financial sector said they observe market trends first. Another 6.7 percent said they wait even longer to release their innovations to market. Instead, they opt to wait for new products to be developed, then integrate the most successful of those products.

Only after observing their competitors’ missteps do they fully commit to the rollout of their innovations. As much as 53.3 percent of the top innovators in the financial sector said they observe market trends first. Another 6.7 percent said they wait even longer to release their innovations to market. Instead, they opt to wait for new products to be developed, then integrate the most successful of those products.

The question is: Do the slow and steady always win the race?

The 2019 Innovation Readiness Index™ explores the answers to such questions and more. PYMNTS analyzed survey responses from more than 200 financial decision-makers at FIs across the United States, ranging in size from below $500 million to more than $25 billion in assets, and varying in type from commercial banks, community banks and credit unions.

Our research demonstrates that most FIs of all shapes and sizes — not just Top Performers — prefer to take innovation slow. Among the FIs that tend to release their innovations shortly after observing market trends, 81.3 percent said they did so to help meet their consumers’ changing expectations. Meanwhile, 64 percent of FIs that waited until products had already been developed, and were being used widely among consumers, said they used this strategy to respond to potential clients’ needs.

For all the time they spend on planning their innovations, many FIs tend to focus on innovating the same — or similar — products as their competitors: namely, consumer and corporate credit cards. More than 90 percent of all FIs have invested or plan to invest in consumer  credit cards, for instance, and more than 85 percent have invested or plan to invest in corporate credit cards.

credit cards, for instance, and more than 85 percent have invested or plan to invest in corporate credit cards.

For this, they can hardly be blamed. These are the types of products and services from which FIs generate the most revenue. Yet, as the Index shows, there are risks to taking such a narrow view of what constitutes financial “innovation.”

To learn more about innovation in the financial sector, download the Index.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More