The adoption of external working capital solutions continues to be widespread globally among growth corporates, commonly known as middle-market firms.

This practice has enabled companies to enhance their operational efficiency and maintain sustainable growth in an uncertain economic environment.

Findings detailed in the Fleet and Mobility Edition of the “2023-2024 Growth Corporates Working Capital Index” highlight this trend, while examining the working capital needs and strategies of fleet and mobility growth corporates — firms generating between $50 million and $1 billion in annual revenues.

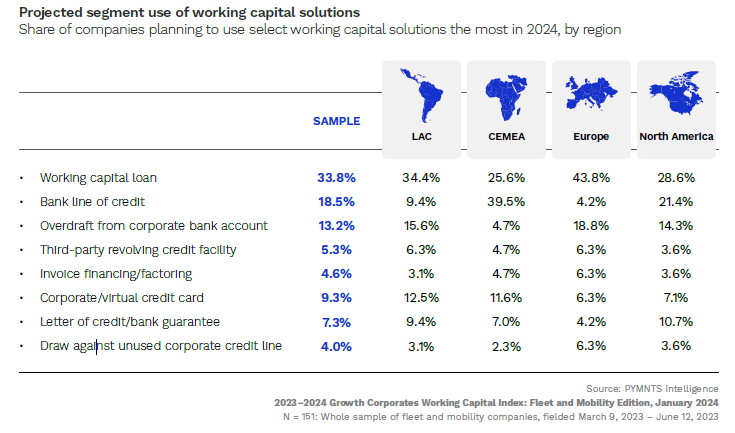

According to the Visa-sponsored study conducted by PYMNTS Intelligence, middle-market firms in the fleet sector employ varied working capital solutions depending on their geographical location.

For instance, European growth corporates predominantly rely on working capital loans (40%) and overdrafts (23%) to finance growth initiatives and handle emergencies, while firms in Latin America and the Caribbean (LAC) are more inclined to finance their expansion through overdrafts (25%), working capital loans (28%) and virtual credit cards (13%).

In contrast, growth corporates in Central Europe, the Middle East and Africa (CEMEA) display a more diverse and fragmented market, with a mix of corporate overdrafts, virtual cards, bank lines of credit, and third-party revolving facility solutions, each being used by less than 10% of companies.

Further data analysis shows that the top-performing growth corporates in the fleet and mobility sector are mainly located in North America and fall within the revenue bracket of $250 million to $750 million. These leading companies demonstrate 26% lower days payable outstanding (DPO) compared to their bottom-performing counterparts, suggesting higher operational efficiency and improved cash flow.

As the segment advances toward strategic growth objectives, the data shows that fleet and mobility firms are planning to increase their reliance on working capital solutions this year, buoyed by a positive economic outlook in the industry that is expected to attract new users of such solutions.

The anticipated growth in use will mainly stem from companies that did not employ any external working capital solution in the previous year. These newly onboarded firms intend to use these solutions for strategic growth initiatives, including investments and system upgrades.

While the overall use of virtual cards is expected to rise, regional nuances are highlighted in the report. European fleet and mobility companies demonstrate a cautious approach toward virtual card use, with a small increase or no change anticipated. However, firms in Central Europe, CEMEA and North America are projected to drive the use of virtual cards, demonstrating a surge in use rates.

Letters of Credit Still Relevant

Letters of credit (LCs) or bank guarantees, once deemed indispensable for transactions but now considered an outdated business practice, remain on the list of select working capital solutions that companies intend to use this year.

Firms in the North American market emerge as the most inclined to rely on these, with over 1 in 10 planning to do so in 2024. Following closely are firms in the LAC and CEMEA regions, while European firms appear the least likely to opt for this option.

Despite the continued prevalence of LCs, PYMNTS highlighted in 2022 that the integration of blockchain technology is modernizing LCs, offering enhanced security, reducing common paperwork errors, and expediting transaction processing.

Meanwhile, the International Chamber of Commerce and Swift have unveiled the first application programming interface (API) industry standards for bank guarantees and standby LCs.

Announced last August, the solution, which is available for testing and implementation by industry stakeholders, is expected to bridge the standardization gap in the trade API space, while providing real-time visibility and enhancing interoperability and integration of banking capabilities, specifically for guarantees and standby LCs.

“The completion of the standard model API for guarantees and standby letters of credit is a great step forward toward interoperability and digitization of trade finance,” ICC Global Policy Director Andrew Wilson said at the time.