Consumers are using mobile wallets more, but it is taking a while for them to grow accustomed to utilizing the technology to pay in stores, PYMNTS Intelligence reveals.

The PYMNTS Intelligence report last year, “The Mobile Wallet Challenge: Replacing Physical With Digital,” created in collaboration with ACI Worldwide, drew from a census-balanced survey of more than 2,000 U.S. consumers to understand their growing interest in using mobile wallets for various purposes.

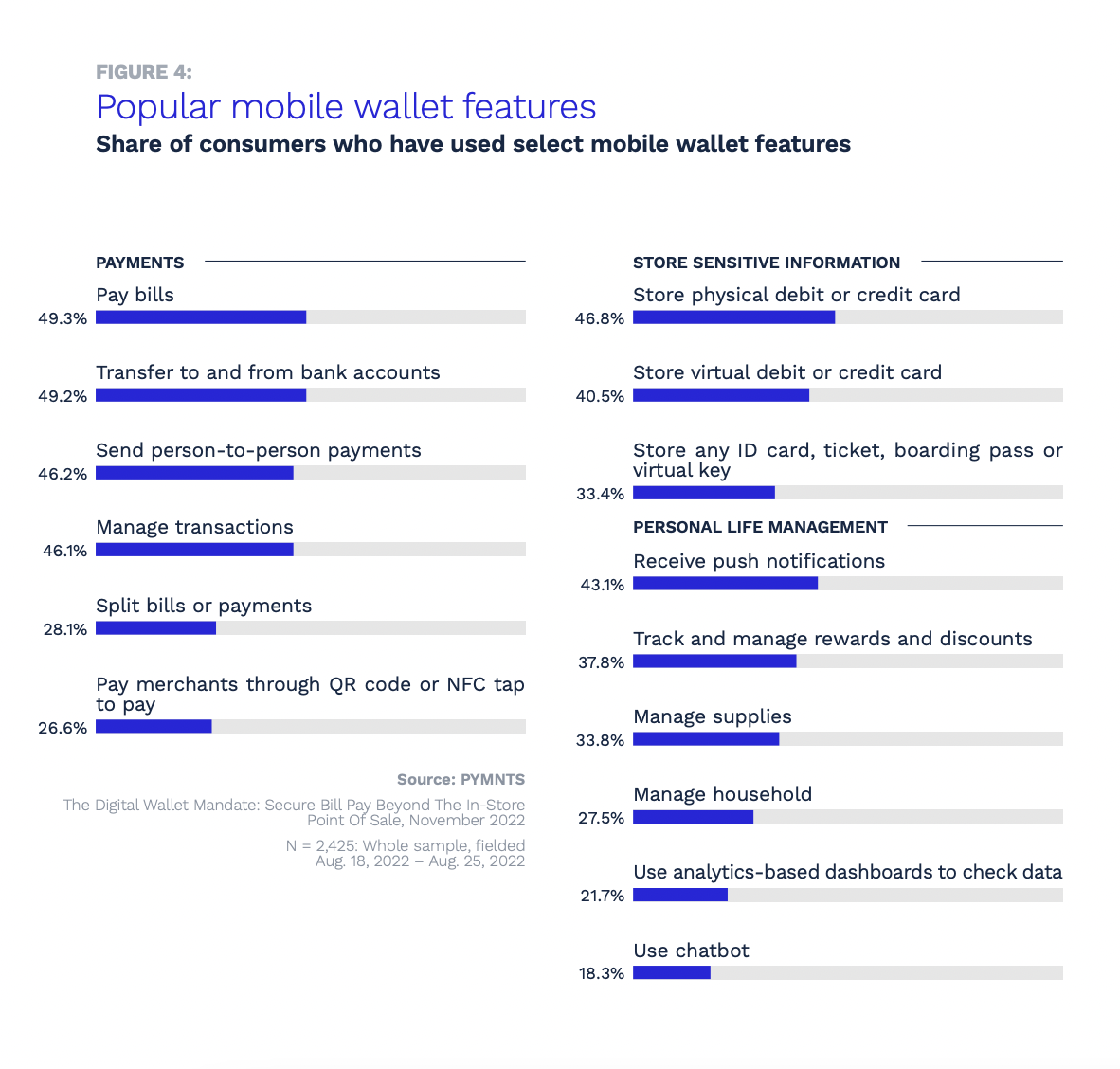

The study found that 85% more consumers use mobile wallets to pay bills than to pay merchants through QR codes and NFC tap to pay, with 49% using the technology for the former and just 27% for the latter.

Many consumers are already accustomed to paying bills through various digital platforms or online banking services. Therefore, transitioning to mobile wallets for bill payments may feel like a natural extension of their existing behavior.

Consumers are also more likely to use mobile wallets to transfer funds to and from bank accounts, to send person-to-person payments, to manage transactions and to split bills or payments than to pay merchants through QR code or NFC tap to pay.

Still, for those who do use the technology to pay in stores, that convenience can be a top priority.

“A faster checkout experience is at the top of customers’ minds when choosing which stores to patronize. Consumers are flooded with options for shopping, both in-store and online and have become more discriminating about their retail experiences,” Peter Davey, then senior vice president and head of the Innovation Lab at The Clearing House, said in an interview with PYMNTS last year. “Retailers, in turn, are offering a range of checkout options with which to accelerate their payments.”

Adoption will likely continue to grow, given younger consumers’ preference for the technology. Research from PYMNTS Intelligence underscores Gen Z’s love for digital wallets, with nearly 80% of them embracing these platforms. This surpasses adoption rates among millennials and bridge millennials, at 67% and 63%, respectively.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More