It’s not that B2B commerce needs to be introduced to the concept of BNPL. B2B buyers and sellers have been trading on credit for centuries, and extended payment terms are the norm for this ecosystem.

Rather, explained Hokodo Co-founder and Co-CEO Richard Thornton, it’s that B2B merchants are now tasked with figuring out how to translate what has traditionally been a lengthy and manual process of extending credit and terms to their customers, onto their digital commerce platforms. With B2B sellers looking to replicate the convenience and seamlessness of integrated BNPL solutions at B2C online checkout, vendors are in need of technologies that can deliver that same user experience while navigating the nuances of B2B trade.

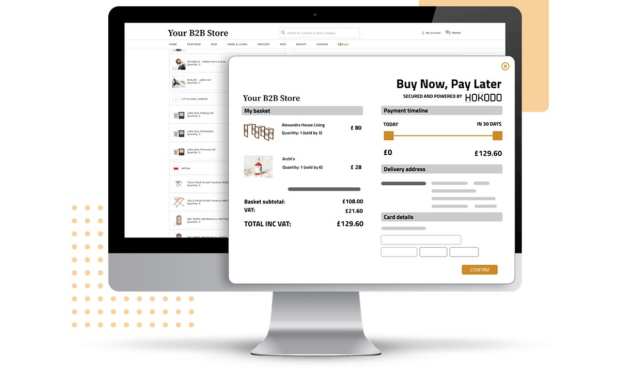

Hokodo announced Thursday (June 10) a $12.5 million Series A funding round in support of its technology designed to do just that. In a conversation with Karen Webster, Thornton discussed what B2B merchants need from retrofitted BNPL technology in order to drive smoother commerce and payments.

BNPL — The B2B Way

More B2B sellers are embracing digital platforms to reach customers, and the pandemic has only accelerated that shift. Yet shifting sales strategies from emails, phone calls, trade shows and in-person sales meetings to a wholly digital ecosystem is no easy feat.

When it comes to extending credit and establishing payment terms with a customer, business buyers are traditionally sent an application for credit approval, which can take several days. That lag is no longer suited for a B2B eCommerce environment, said Thornton.

“That works fine with a sales rep, but obviously, it doesn’t work when you’re selling online — and the world of B2B is moving online,” he noted.

With more B2B sellers stepping onto a digital platform for the first time, translating customer credit workflows to an online world can be a confusing headache. Alternatives, like factoring solutions or trade credit insurance, aren’t translating well to the world of B2B eCommerce, Thornton said.

With factoring, for instance, it’s only after a purchase agreement has been made and an invoice has been generated that a company will be able to determine whether or not that deal can be financed. In an offline world, firms would typically discuss the potential purchase with a factoring provider first. Yet with B2B traders no longer willing to wait days to get financing in place, companies need to understand credit decisions at the point of purchase.

A Tailored Approach

Thornton said there are three key features necessary for a digital B2B credit solution to be successful.

The first is a significant investment in credit analytics, which enables Hokodo to develop tailored underwriting algorithms depending on the profile of the customer. Second, he said, is enabling technology that is highly configurable, empowering merchants to relax criteria for trusted customers, or tighten them up for new ones. Third — and according to Thornton, perhaps the most difficult to achieve — a B2B credit tool must be able to understand the unique needs of specific verticals.

He pointed to the digital trade of grain as an example of a transaction in which a contract is signed but a delivery may not happen for months until grain is harvested. In another example, equipment rentals might be facilitated for $2,000, but a customer could extend that rental and ultimately owe $4,000. In some sectors, B2B purchases are a few hundred dollars, while others can be tens of thousands of dollars.

“Each of the verticals we’re in has its own idiosyncrasies, and we have to find ways of culminating with them,” said Thornton.

To provide the kind of positive customer experience that B2B merchants are after, it is not only essential to customize underwriting process to fit the unique profile of a buyer, but also to optimize the timing and amount of that credit.

Empowering the B2B merchants themselves with what is both a staple and a competitive advantage in their fields is also key. According to Hokodo, merchants that deploy its technology see a 40 percent increase in revenue, which Thornton attributes to higher conversion rates, larger basket sizes and repeat customers. When buyers can seamlessly secure credit, they’re more likely to stick with that vendor and consolidate spend with them.

On the heels of that success, and with new funding from Mosaic Ventures, Notion Capital and angel investors, Hokodo is gearing up to scale via new team hires and meet growing demand from new merchant clients.

In the digital migration, B2B merchants have plenty to be concerned about. Translating legacy workflows like price negotiations, bespoke and customizable products, or electronic B2B payments acceptance, to an eCommerce environment is difficult, but innovators are gradually chipping away at these pain points. And as they do, said Thornton, sellers need to have a way to extend credit and establish payment terms with their customers digitally to support these modernization efforts.

“All of these problems are gradually being solved,” Thornton said. “Our strategy is to make sure that, as people and industries and suppliers get to the stage where they feel ready to move online, payment terms don’t become a blocker.”