The 34,000 companies operating in the United States’ wholesale food distribution industry generate about $991 billion in collective yearly revenue.

Even as digital technologies advance, however, paper checks still account for a large segment of wholesalers’ B2B payments. The paper check industry standard has led to growing frictions as wholesalers face pandemic-related supply chain struggles and increased demand worldwide.

Data from the United Kingdom’s Federation of Wholesale Distributors found that independent wholesalers saw their sales decrease as much as 80% between 2020 and 2021, while larger players saw declines of about 34% during this period.

As industry competition tightens, many distributors are moving to cut costs by reducing their reliance on paper checks and other manual B2B payment tools. Visibility into a company’s supply chain is a must as retailers, grocers and other businesses come to expect more flexibility and transparency out of their distributors and suppliers. One updated 2019 study found that 75% of surveyed companies considered supply chain visibility to be essential to strengthening relationships between businesses and consumers.

Wholesale companies must be able to support digital-first payment methods while also finding ways to make and reconcile paper check payments more swiftly and easily. This month, PYMNTS examines how implementing emerging technologies can help wholesale distributors reduce current B2B payment frictions while transitioning to new, digital payment tools to foster lasting relationships with their clients and business partners.

Leaving a Digital Space for Paper Checks

The global health crisis has driven companies to rethink how they are making routine B2B payments as business conditions have grown less forgiving of checks’ frictions. Check payments — together with paper invoices and other manual B2B processes — can be slow to finalize, leading to payment delays that can severely impact wholesalers’ cash flows. One study found that 69% of payments made to wholesale frozen goods providers are current, while 12% are up to 30 days late, and 17% are more than 90 days late. Such payment lags can have significant economic consequences for wholesalers, especially as margins have become increasingly thin. Food wholesale distributors not only are struggling to regain lost ground due to the pandemic but also are working with a decreased pool of potential new clients. U.S. restaurants alone lost $240 billion in 2020, with 100,000 physical eateries closing down.

These figures make it crucial for wholesalers to transition to digital-first B2B payment methods, but with checks still representing a thriving percentage of payments in the space, it is difficult for companies to avoid legacy payment methods entirely. A 2019 report found that for 78% of distributors and wholesalers, eCommerce accounted for only 10% to 25% of their annual sales, leaving the rest to be paid and processed with paper checks.

Merging the Old With the New

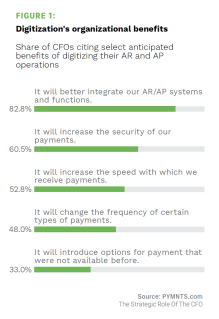

Wholesale distributors are far from the only companies seeking to innovate their B2B processes without alienating the significant portion of their customer bases still looking to send and receive funds via checks. PYMNTS’ data shows that many companies are beginning to view digitizing their accounts receivable (AR) and accounts payable (AP) processes as a strategically important move for their organizations. Nearly 53% of chief financial officers (CFOs) cited receiving faster payments as an anticipated benefit of digitizing their AR and AP operations.

The same PYMNTS report found that companies are wary of replacing their current processes or infrastructure entirely, however, with many seeking to tap digital technologies to speed up their established payment processes rather than completely revamp them. The report noted that 59% of surveyed companies in the food and beverage distribution industry said AP digitization should be geared toward transforming previously existing processes or using digital tools to do things in new and better ways, as opposed to simply eliminating manual functions and replacing them with digital ones.

A strategy that involves both innovating B2B payment processes to support emerging digital-first tools and enabling swifter check payments through automation could be key to meeting distributors’ shifting needs.