For faster payments — and specifically, for real-time payments — it may be a case of slow and steady wins the race.

In the study “Real-Time Payments: How Speed is Changing the Mix of Business Payments,” done in collaboration between PYMNTS and The Clearing House, there’s a common consensus among a majority of companies surveyed — 61% of them, in fact — that real-time payments can offer significant operational and strategic advantages.

Among those advantages: Better accounting efficiency and lower risks of payment failure.

And yet, by the numbers, the embrace of real-time payments has been muted, to say the least. Consider the fact that the same study found that RTP accounts for only 8.2% of payments received and 6.4% of payments sent across the 100 firms we surveyed.

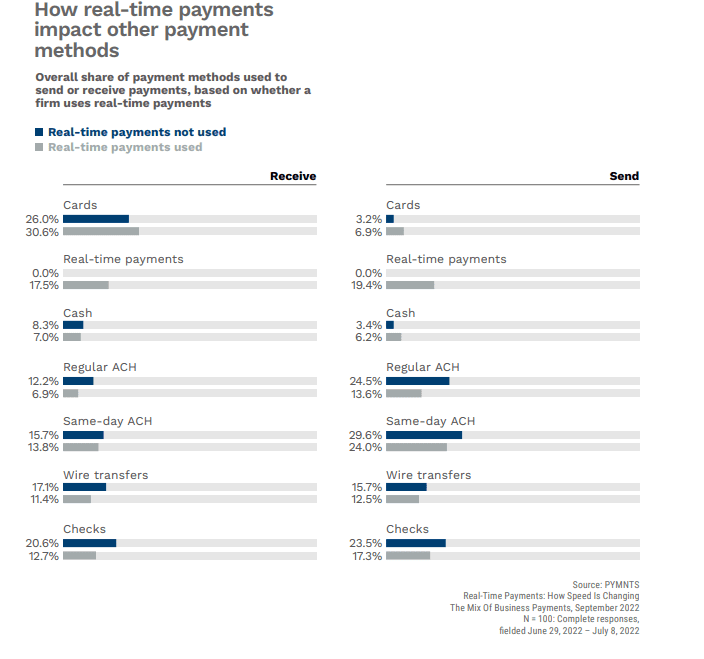

But once things get going, so to speak, we start to see RTP chipping away at other, entrenched payment methods. In the chart below, we can see that checks, for example, are used significantly less often by firms that transact with RTP than those that do not. The same goes for wire transfers.

But it’s interesting to note that card usage remains relatively high when it comes to receiving payments, at nearly a third “share” of transactions.

That’s likely due to the fact, we’d posit, that card transactions are somewhat quicker than wires and ACH and have of course been around for decades.

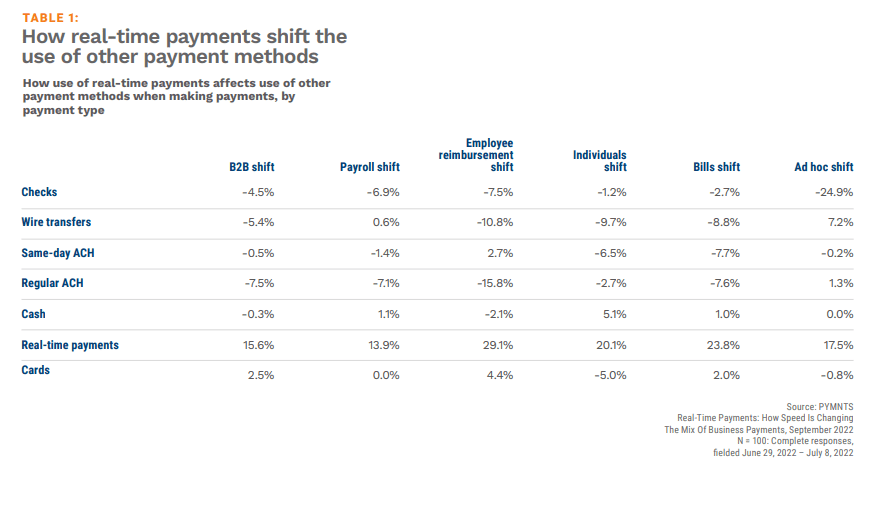

The questions remain as to just what it will take to get toward critical mass for RTP in B2B payments. Some answers can be gleaned from the chart below that shows just where companies are leveraging those payment choices.

There’s a particular appeal, as the numbers show, in using RTP for payroll and for employee reimbursements, where double-digit shifts here tend to be accompanied by shifts away from using other payment methods. It’s the individual, employee-level side of the business that seems to be among the most readily available conduit to get RTP into the mix.

As for the greenfield opportunity: 14% of the companies with annual sales of at least $1 billion are currently enhancing their real-time payments functions. An additional 63% are planning to upgrade their systems in the next 12 months. Conversely, and on the other end of the spectrum, a comparatively minuscule 3.3% of smaller companies — defined as firms with $250 million to $500 million in yearly sales, are currently working on improving their real-time payments capabilities. Forty-seven percent say they are enhancing their systems and will have them completed in the next 12 months.

As for the greenfield opportunity: 14% of the companies with annual sales of at least $1 billion are currently enhancing their real-time payments functions. An additional 63% are planning to upgrade their systems in the next 12 months. Conversely, and on the other end of the spectrum, a comparatively minuscule 3.3% of smaller companies — defined as firms with $250 million to $500 million in yearly sales, are currently working on improving their real-time payments capabilities. Forty-seven percent say they are enhancing their systems and will have them completed in the next 12 months.

Those plans indicated that within the next 12 months, and then of course beyond, RTP payments will be much more visible in B2B settings and in direct, employee-facing interactions within the companies themselves. The process will be an evolution — because of course, the companies themselves must have the technological capabilities in place first — but a steady one. And a year from now, our findings on the state of real-time payments may look quite a bit different.![]()

The Consumer Financial Protection Bureau’s (CFPB) acting director has reportedly agreed to pause a mass firing of agency employees.

As ABC News reported Friday (Feb. 14), attorneys for Russell Vought, acting director of the CFPB, reached an agreement during a court conference to postpone the firings amid a lawsuit challenging the regulator’s dismantling.

The agreement bars the CFPB from firing employees for reasons not related to their work performance or conduct, and also blocks the Trump administration from trying to shift funding away from the consumer protection agency.

According to the report U.S. District Judge Amy Berman Jackson said she will consider issuing a longer-term preliminary injunction at a hearing on March 3. Her ruling came after the CFPB cut its probationary workers as part of the Trump administration’s wide-ranging layoffs.

Unions representing the employees and suing the administration alleged in a court filing that Vought planned to fire more than 95% of CFPB staff. They argued that cuts of this size — or the end of the CFPB altogether — could have drastic consequences for American consumers.

Under the court ruling, the White House is also barred from destroying or altering sensitive records kept by the CFPB.

This came after former CFPB Chief Technologist Erie Meyer alleged in a legal filing that administration officials were preparing to delete databases holding the agency’s data, such as compliance and enforcement records.

“Reports that I have received from within the Bureau reliably indicate that databases holding the CFPB’s data will soon be deleted,” Meyer said in the filing. “If that happens, it would result in the immediate and irrevocable loss of data essential to the agency’s core mission.”

Vought last weekend froze all of the CFPB’s supervisory and examination activities, while also shutting down the bureau’s office and ordering workers to stay home. He’s also pledged to halt the agencys funding, saying he had told the Federal Reserve that the CFPB would not take its next draw of appropriated funding because it wasn’t necessary to fulfill its duties.

The suspension of work by the CFPB left the financial services industry wondering what to do next, PYMNTS wrote last week.

“If nobody’s home, you have financial services entities just trying to make their best guess,” former Obama administration assistant treasury secretary Amias Gerety said Monday as part of his weekly discussion with PYMNTS CEO Karen Webster.