![]()

Cross-border payments have been critical in keeping the global economy afloat during a period of extraordinary instability. As a result, a report predicted that the transaction value of global remittance and cross-border payments will rise from $37.2 trillion last year to $39.9 trillion by 2026. The increased demand for cross-border transactions means that consumers need dependable, speedy and secure services, a not-so-easy ask of a space that is historically plagued with obstacles and slow transaction speeds.

Cross-border payments’ popularity is gaining momentum across all markets, particularly among small- to medium-sized businesses (SMBs). Thirty-eight percent of SMBs are sending and receiving more cross-border payments this year than in 2020, according to one report, and 74% said cross-border payments played a key role in helping their businesses survive the pandemic. Perhaps most impressive, however, is that 81% of SMBs that use online cross-border payments agree such capabilities have helped their businesses flourish. Organizations are becoming more aware of the various cross-border payment options accessible to them and are eager to incorporate these options to meet consumer demand and to help their businesses expand overseas.

The following Deep Dive examines how cross-border payments solutions can be used as a marketing tactic to help attract new customers from different geographic locations. It also explores how payment service providers (PSPs) can innovate their services to ensure optimal experiences for all involved parties.

Addressing Consumer Payment Preferences, Fraud Concerns

A growing number of consumers are becoming more comfortable with sending and receiving cross-border payments, and higher transaction volume is highlighting technological shortcomings in current practices. More than one-third of respondents in a Mastercard report complained of the time it takes for cross-border transactions to reach completion, and 73% said they would be more inclined to use online systems if they were quicker, for example. The delays in payment confirmation make 73% of consumers anxious when conducting cross-border transactions, and 40% said sometimes they never even receive a confirmation notification.

Cross-border merchants are discovering that simply accepting credit or debit card payments is no longer sufficient. There are more than 450 primary local payment methods in use all over the world, and as consumers grow progressively disenchanted by past purchasing norms, accepting only traditional payment methods, such as cash and credit cards, can limit spending potential. In the U.K., retailers that disregard their customers’ payment options risk losing 44% of their customers, for example. Merchants can bridge the gap between themselves and the foreign market by considering the local payment preferences of customers in a way that is compatible with regional laws and regulations.

Concerns over fraud are also influencing the purchasing habits of international consumers — a valid fear, as fraud and identity theft reports are up 45% from 2019. Worries about falling victim to fraud prevented 50% of consumers from making digital cross-border payments more often. Additionally, 45% worried that their funds would be deposited in the wrong account due to human error, a complication that often occurs within companies that still use manual processes instead of automated systems. To sway foreign customers to make purchases outside of their local regions, businesses must first properly secure their infrastructure against cyberattacks and invest in the appropriate accounts payable (AP) technology.

Familiarity Is Key to Boosting Cross-Border Sales

The pandemic has compelled businesses to reconsider their payment operations and rethink customer interactions. SMBs are becoming more aware of the different payment alternatives available to them and are feeling encouraged to promote the use of those that best fit their customers’ needs.

Payment providers are now striving to offer customized solutions that make the payment experience more seamless and contactless, such as QR codes, tap-to-pay technologies and link-based payments. Organizations can simplify the seller onboarding process to attract more sellers and lower expenses as well. Mastercard, for example, launched Soft POS in India, a multiform-factor, white-label solution for banks and payments providers that allows a smartphone to act as a merchant acceptance device.

customized solutions that make the payment experience more seamless and contactless, such as QR codes, tap-to-pay technologies and link-based payments. Organizations can simplify the seller onboarding process to attract more sellers and lower expenses as well. Mastercard, for example, launched Soft POS in India, a multiform-factor, white-label solution for banks and payments providers that allows a smartphone to act as a merchant acceptance device.

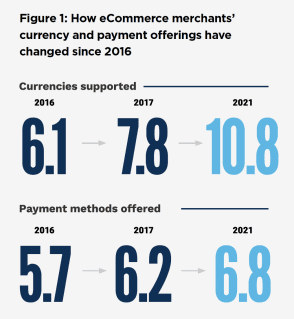

For consumers, merchants are working to increase the number of currencies and payment types they accept on their websites or mobile apps. Only 6.1 currencies and 5.7 payment methods on average were supported by eCommerce platforms in 2016, according to PYMNTS’ research, but those numbers have risen to 10.8 and 6.8 in 2021, respectively, since digitization in the eCommerce sector accelerated. This data suggests that most merchants have added at least one new payment option over the last four years. When customers can pay in the way they prefer, they are more likely to complete transactions and make future purchases, increasing their loyalty.

Merchants must tailor their customer experiences to each market in which they are looking to expand to thrive in cross-border eCommerce. This entails enabling a wider range of payment options, accepting a greater variety of international currencies and adapting their websites for local languages. Alternative payment methods continue to gain momentum for cross-border transactions, and customers are more likely to shop at an overseas merchant that offers their preferred local payment method at checkout. Offering the top three payment options in any region can help boost sellers’ conversion rates by up to 30%, according to research by ACI.

By procuring a more familiar experience for foreign users, companies stand to gain the trust of a larger demographic of consumers, enhancing their brands’ names and boosting cross-border sales.