There’s never been a better time for digital-first financial institutions (FIs), as customers are pulling their savings from big banks.

The opposite seemed true just a few short months ago. U.S. consumers were hesitant to break up with their traditional FIs, for reasons ranging from the convenience physical branches might offer to time required in switching banks and associated accounts. This overall consumer hesitancy likely played a large role in the slow adoption of digital-first banking in the U.S. market and started leading to sector job cuts.

Then the new year hit and customer savings cushions began dwindling as more consumers live paycheck-to-paycheck, including over half of high-income earners. As The Wall Street Journal reported last week (Feb. 7), consumers and businesses are pulling their deposits out of the standard non-interest-bearing accounts most big banks offer. A good share of these funds will likely be transferred to products such as CDs and high-yield savings accounts offered by some traditional FIs. Presumably however, a large portion of bank customers may be newly considering, or have already jumped to, making a digital-first bank their primary FI. The main driver for consumers making the switch are the higher interest rates offered on many neobanks’ regular checking and savings accounts.

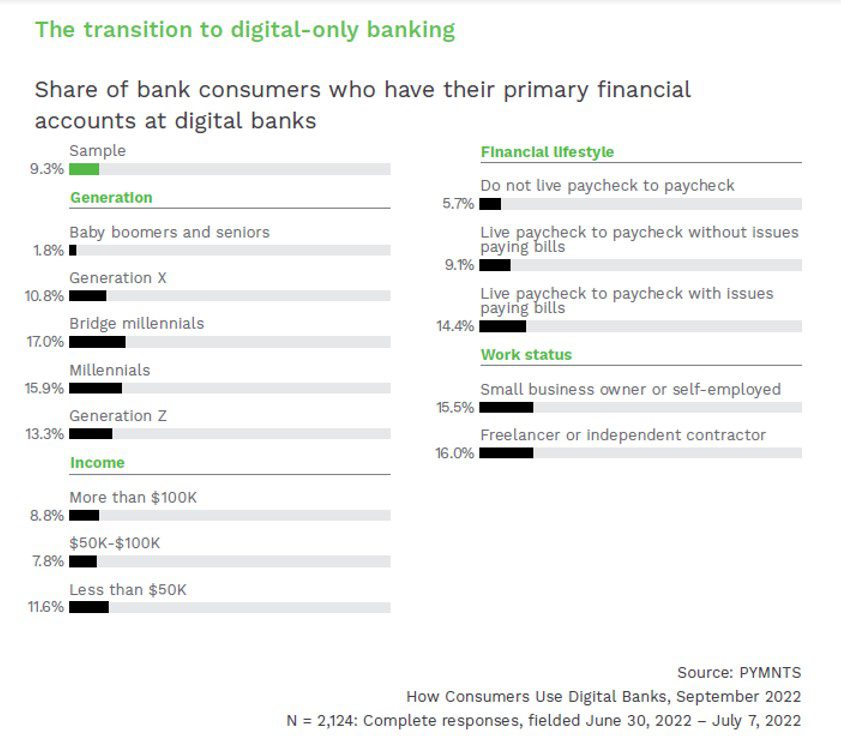

As with many digital-first experiences, per PYMNTS’ “How Consumers Use Digital Banks,” the younger generations are leading the move towards neobanks.

The appeal of higher account interest rates is undoubtedly a primary concern for consumers considering the switch. However, digital-first FIs may offer further appeal through other customer satisfaction approaches that under the umbrella of experience-oriented banking. Personalization features strongly in these approaches neobanks offer, including customizable budgeting assistance and expanded payment choices such as bank-backed buy now, pay later. Some have started offering digital products aimed at under-18s.

This delivery on promises of personalization and convenience may be especially appealing to younger consumers, who consistently prefer robust digital banking apps and solutions that help build and manage wealth. It stands to reason, then, that these innovative offerings could be another factor in the higher rate of consumers who call digital-first banks their primary institution. Small businesses have been turning to neobanks as well, seeking fresh sources of capital from digital-first FIs.

Advertisement: Scroll to Continue

And digital-first banks have been seeing results for these strategies. U.K.-based Mondo may see light at the end of the profitability tunnel by the end of this year as the bank’s most recent earnings showed an annualized revenue surge of 250%, to £44 million in 2022. This kind of increased profitability may be a factor in Thailand recently approving virtual banks’ operation within the country. It could also be why in November Saudi Arabia granted licenses to three local neobanks, marking the first time since 2006 that new Saudi-based banks have launched in the kingdom.

Big banks are noticing consumers’ increasing openness towards digital-first banking, especially among the younger set, as rumors swirl around Chase possibly exploring their own digital-first banking options overseas. Whether they continue to keep any major neobank industry disruption at bay remains to be seen. Though as it currently stands, customers and banking businesses may turn out to be the real winners in this sector tug-of-war.