Overpayment disbursements — rebates, rewards, refunds, etc. — may not come to mind when considering a consumers’ overall cash flow, but, when these overpayments are issued, consumers want them quickly.

Only about 71% of consumers receive some form of refund disbursements, with the average payout being about $68 (far less than the average disbursement amount of $433). Yet, according to PYMNTS Intelligence’s latest “Generation Instant” report, “How Instant Payments Help Consumers Receive Overpayment Disbursements Faster,” consumers are 39% more willing to pay a fee to receive a refund disbursement instantly than they would be to receive an average disbursement.

The report, a collaboration with Ingo Payments based on surveys with nearly 3,900 U.S. consumers, confirms that when consumers agree to pay a fee for instant access to overpayment refunds and rebates, they prefer paying a percentage fee. Why? Most of these disbursements are smaller in value, making percentage fees a cheaper alternative to paying a fixed-rate fee.

But data confirms consumers are so eager to get their overpayment disbursements instantly that they would even be willing to pay a fixed fee, highlighting the importance of getting even seemingly modest overpayment disbursements as quickly as possible.

Data shows that 79% of consumers would choose instant methods to receive overpayment refunds if given the opportunity, which is up 17% from September 2023, confirming a growing demand.

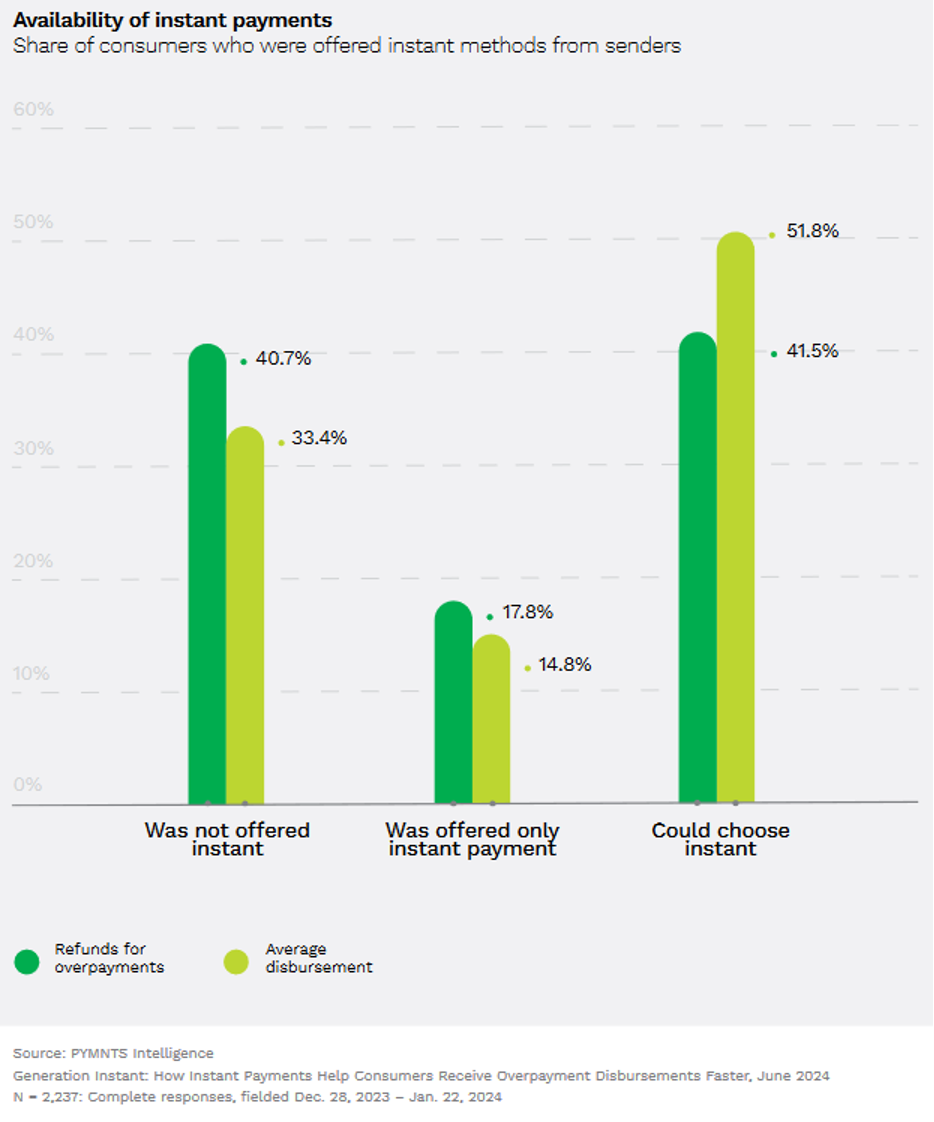

However, as the figure illustrates, overpayment refund receivers are 22% less likely than the average consumer to be offered the opportunity to receive funds instantly. While 52% of consumers receiving all types of disbursements could choose instant pay, just 42% of receivers of overpayment refunds are given the option. In fact, 33% of consumers receiving all types of disbursements could not receive payments instantly, and this rises to 41% for overpayment payments. Although they have less opportunity to use instant payment methods, overpayment refund receivers are slightly more likely to have instant as their only option than the average disbursement receiver.

Consumer appetite for instant payments isn’t confined to overpayment disbursements. In a series of recent reports, PYMNTS Intelligence determined there is an undeniable appetite on the part of most consumers to get paid faster — especially for those with fluctuating pay levels, such as gig workers, or others who may not earn traditional, biweekly paychecks.

In “Measuring Consumer Satisfaction With Instant Payouts,” we found that more than 58% of consumers who earn money for freelance, contract or consulting work said they would be willing to pay a fee to collect their earnings instantly. Similarly in “How Truckers Use Instant Payments to Support Their Lifestyles,” we determined that 93% of professional truck drivers in the U.S. would opt for instant paychecks if they were available. Another PYMNTS Intelligence study found that 78% of Americans were highly satisfied when they received government disbursements, retirement distributions, dividend payouts and insurance settlements instantaneously.

In other words, the desire to receive overpayment disbursements instantly reflects a broader trend: people want to get paid quickly. The fact that most Americans are willing to pay a fee to receive even modest disbursements in real time underscores the financial pinch many budget-conscious consumers now feel. For merchants and other payment senders looking to retain current customers while attracting new ones, instant payments may be one way to gain traction in the market.