By any measure, initial public offerings (IPOs) were hot last year, buoyed in part by the embrace by retail investors of special purpose acquisition companies (SPACs).

To get a sense of how heady the activity was in 2020, analysts have estimated that there were 480 IPOs on the U.S. markets alone, up more than 100 percent from the previous year. It’s a record year, too, as the 2020 reading was more than 20 percent higher than had been seen in 2000, the previously highest year for IPOs. We may be headed into an especially rarefied territory in 2021, as there have been 250 public listings in the U.S. as of the end of February, far outpacing the 32 seen in 2020.

Within that subset, the SPAC has gained ground, too. SPAC Research has estimated that 189 SPACs have gone public so far in 2021, at a velocity that far outruns the 248 that was seen in all of 2020.

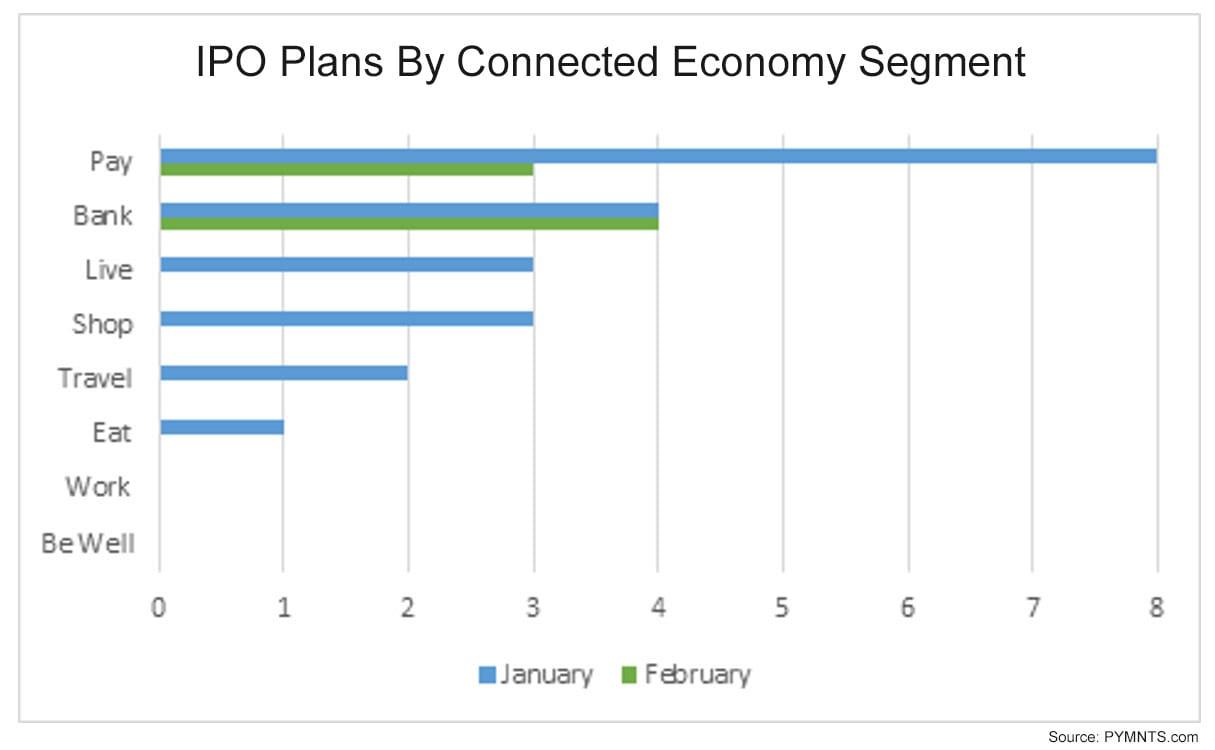

Drilling down, as PYMNTS has found, FinTechs and payments and commerce companies have seen their own fair share of public listings. Just two months into the year, planned IPOs announced by segment show 11 firms within payments, and eight within banking, to point out two of the more crowded spaces. The chart below shows how each of the PYMNTS connected economy sectors (How We Will Pay, How We Will Eat, etc.) fared for January and February. As shown, the payments sector jumped out to a torrid start in January, as did other sectors. Among the eight payments companies filing in January: Affirm, Poshmark and Petco.

It should come as no surprise that the payments and banking sectors should be overweighted here, given the fact that a number of FinTechs are coming to market. Square, PayPal and others have illuminated the appeal that the great digital shift holds for the companies that seek to enable the transactions themselves, which, after all, transcend verticals.

In recent headlines, with some of the larger targeted capital raises attached in recent weeks:

Velocity Merger

Velocity Merger, a blank check firm focused on FinTechs, said last week that it had filed with the SEC to raise up to $250 million via IPO. The implied market value of the firm, as reported by Renaissance Capital, would be about $313 million.

Figure Acquisition I

Figure Acquisition I raised $250 million earlier last month, eyeing the FinTech and financial services sectors. Figure Technologies issues mortgages and loans using its own blockchain, called Provenance. It was founded in 2018 and raised $220 million from Ribbit Management, DST Capital, RPM Ventures, Nimble Ventures and Morgan Creek, the prospectus noted.

ByNordic

Elsewhere, as reported by Renaissance Capital, ByNordic Acquisition, also filing as a blank check firm but intent on targeting firms in northern Europe, has said that it will go public at $150 million, which is a deal size that is 50 percent higher than an original announcement made in August of last year.

Affirm, Too

As for firms that have already gone public, Affirm Holdings last month priced its own IPO, and which now has a market cap north of $23 billion, reported that it is launching a debit card with buy now, pay later (BNPL) functionality.

“We know consumers are looking for financial control and flexibility. In the last year, we’ve seen two key trends: huge growth of buy-now-pay-later transactions and consumer preference shift to debit cards over credit cards. The Affirm Card combines the two, allowing Affirm to meet consumers where they are and empowering them to pay on their own terms,” Affirm Founder and CEO Max Levchin said in the late February announcement.

The Tailwinds

The tailwinds that have underpinned the digital payments revolution, and by extension, the SPAC-centered activity that draws a bead on digital payments, can be crystallized by PYMNTS data from the end of February.

In the PYMNTS’ Holiday Retrospective Report: Merchant Insights For 2021 And Beyond, a study done in collaboration with PayPal, 40 percent of the more than 2,000 consumers surveyed said that they’d used a digital wallet to pay for gifts during the holiday season — up by more than 50 percent from 2019. As many as 62 percent of consumers used QR codes and 47 percent turning more to alternative credit solutions like buy now, pay later (BNPL) plans. Some 75 percent of consumers who switched to digital shopping channels said they would maintain “some or all” of those digital habits after the pandemic ends.

The Headwinds

In today’s market, there aren’t many obstacles to filing for an IPO via direct listing or SPACs. The main obstacle any company should consider, especially those who have benefited from the acceleration of the digital-first economy, is planning for the post-pandemic economy. Affirm is a perfect example.

On Feb. 11, the company presented what looked on the surface like respectable results. Among them, gross merchandise volume (GMV) for the second quarter of fiscal 2021 was $2.1 billion, an increase of 55 compared to the second quarter of its 2020 fiscal year. Active consumers were 4.5 million, a hike of 52 percent and transactions per active consumer stood at 2.2, an increase of 7 percent. CEO Max Levchin told the company’s earnings call that he saw the results as a prelude to continued expansion, perhaps into everyday purchases, in 2021.

But Wall Street analysts have a nasty habit of looking past history and into the future. Affirm had to address its 2021 plan. It said it expected its third-quarter gross merchandise volume (GMV) to decline to between $1.80 billion and $1.85 billion, compared to the $2.1 billion reported for the previous quarter. That revision sent its shares down 8.7 percent in after-hours trading.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More