The crypto winter has now chilled all manner of digital currency activities, including an IPO.

FinTech Circle, which issues USDC stablecoins, said in an announcement Monday (Nov. 5) that it would no longer go public through a proposed business combination with SPAC Concord Acquisition Corp. The deal had been planned more than a year ago, in July 2021. And while Circle has maintained that, in the words of CEO Jeremy Allaire, going public “remains part of Circle’s core strategy,” the termination speaks volumes about SPACs and stablecoins.

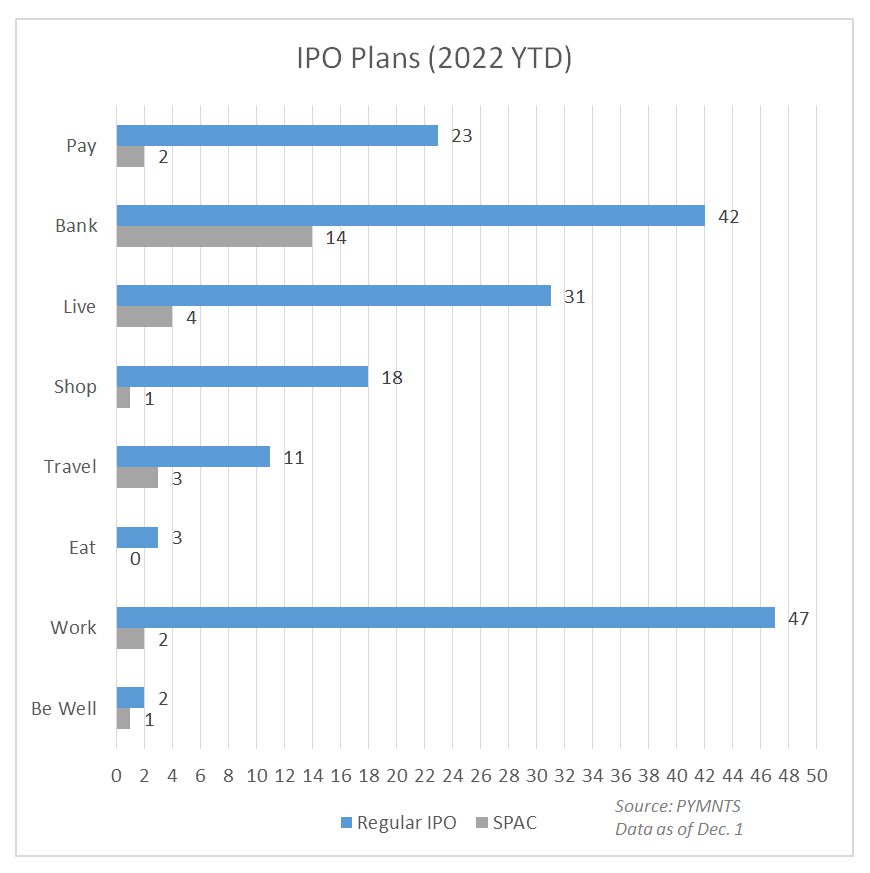

PYMNTS own data speaks to the first point: SPACs, once the darling of Wall Street, are now the equivalent of investing’s persona non grata.

The chart below, as compiled year to date, shows that SPAC-related activity — particularly in the payments space — has been anemic at best, in the low single digits.

As for Circle, management noted that the proposed transaction “timed out,” as the Securities and Exchange Commission had not declared the filing was effective.

Advertisement: Scroll to Continue

We note that the timing out, as cited by the companies, might be viewed as a technicality. By stating the goal is to go public over the longer term, the read across might be: Wait until the dust settles.

For stablecoins, the dust may not settle anytime soon.

As Circle pointed out in its announcement, the company became profitable in the third quarter of 2022, with total revenue and reserve interest income of $274 million and net income of $43 million. Circle also said that it ended the quarter with close to $400 million in unrestricted cash.

That last metric is one that shows liquidity on hand that can navigate turbulent operating seas. And the latest Reserve Report, prepared by Grant Thornton, lists $43.5 billion of USD Coins in circulation, with slightly more than that in Treasuries ($35.7 billion) and the remainder in cash. However, the latest reading of circulating supply is down from more than $50 billion as recently as October.

Stablecoins have had a bumpy time of it as of late, in the wake of the continued FTX fallout. The overall market cap of the stablecoin industry, as measured by CoinCodex, is about $146 billion, where the peak had been more than $180 billion before the Terra/Luna implosion, and down from more than $150 billion just before the Thanksgiving holidays. We’ve noted that the stablecoin market is one where pretty much any private firm can strive to create a coin, and this is a world where even the infamous SBF had promised to deliver a stablecoin.

There’s at least one use case for stablecoins that seems to be diminished: using fiat to buy stablecoins and then using the stablecoins to buy crypto. If the demand for cryptos continues to wane — sites including Coindesk have noted outflows from crypto funds at levels not seen in months — then stablecoins might have a continued rocky road ahead.

Last month, Circle’s Allaire wrote to Congress stating that there’s a need for legislation at the federal level on reserve requirements and transparency from the companies themselves.

What stablecoins may be in the future – well, that’s anyone’s guess. Right now, one thing they won’t be ….is Wall Street’s next darling.