Fighting payments friction is more or less PayPal’s DNA.

In its early days (a little less than two decades ago), PayPal solved the payments frictions associated with using checks to pay for purchases made on eBay. One Touch Checkout on mobile in 2014, and on web in 2015, removed the friction of entering name, address, billing, shipping information and a sixteen-digit account number to complete a purchase online — or via the fastest growing online commerce channel then and now: mobile.

Today, 96 million of PayPal’s 245 million users and 9 million businesses (79 percent of internet retailer’s Top 100 merchants) use it, and according to a recent comScore survey, more than half who do say they make more online purchases because One Touch makes it easier to checkout.

With all that progress, friction remains a stubborn problem for digital retailers to crack. It’s estimated that $236 billion is up for grabs each year, as sales gravitate to the merchants with the least amount of friction on the way to checkout. It’s a problem that plagues big and small merchants alike.

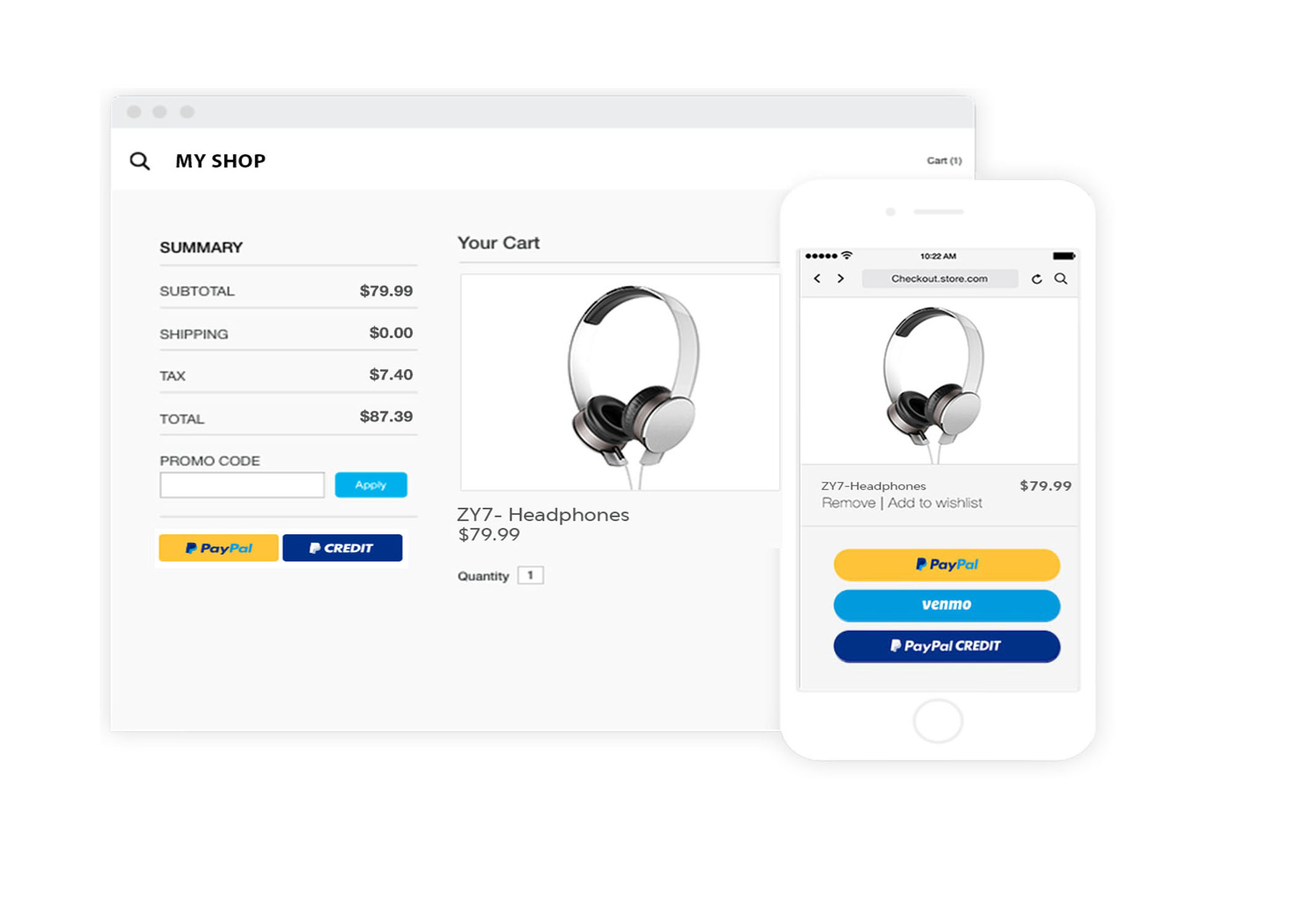

Yesterday, with the launch of PayPal Checkout with Smart Payment Buttons, PayPal EVP and COO Bill Ready told Karen Webster that it was time to make checkout buttons work smarter by not making it harder for consumers to pay using the method of their choice — or harder for merchants to streamline how those options were presented to consumers at checkout. Smart Payment Buttons dynamically present the payment methods that individual consumers will find most relevant, without a complex merchant integration or having to Nascar-ize their checkout page with every conceivable payments option, and support each of those options as part of their existing payments workflow.

“There’s been a coming-of-age with mobile when it comes to the proliferation of digital wallets and the new buying experience,” Ready told Webster. “Merchants are now bombarded with all the new ways that their customers might want to pay for what they buy. Our goal with the rollout of Smart Payment Buttons is to make it easy for merchants to present the most personalized payment option possible for our different audiences.”

Creating Consumer Choice Without Creating Confusion

Smart buttons started with PayPal’s increasingly diverse ways to pay in-house — some customers use PayPal, some are Venmo customers, some are PayPal credit customers and some use a mixture of all three. The initial thought, Ready told Webster, was that those customers should be able to see the buttons most relevant to them; customers who use all three services should get to choose among all three, while customers who use just one only need to present the one option they always use.

Ready said they soon discovered that the opportunity was bigger. In fact, it was quite literally global.

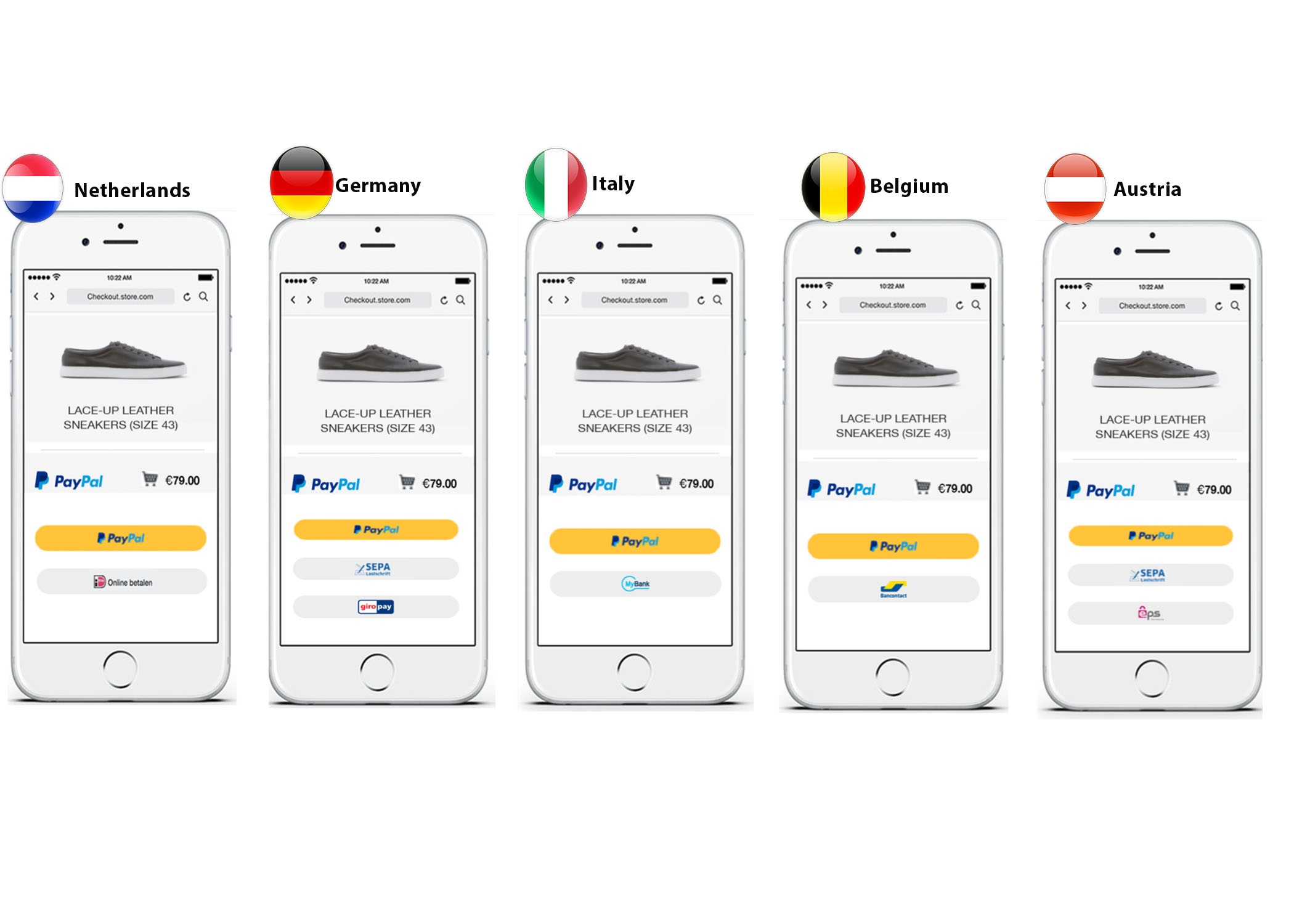

“If you look outside the U.S., you see all types of local payment methods that are most often shown on the biggest eCommerce sites,” Ready said.” Small- and even larger medium-sized firms can support accepting local payment methods, even if they wanted to offer those options to their customers. It’s simply totally out of reach.” Smart Payment Buttons, he noted, puts that in reach. Over the next few weeks, Smart Payment Buttons will enable iDEAL for customers in the Netherlands, Bancontact for customers in Belgium, MyBank for customers in Italy, Giropay for customers in Germany and EPS for customers in Austria. SEPA Direct Debit for customers in Germany is already online and, Ready noted, local payment method rollouts will be ongoing.

Since the Smart Payment Button technology is designed to be expansive and inclusive, Ready told Webster, the odds are becoming increasingly good that a customer will be able to find their chosen payment method. However, because the tech is smart, customers will only have to look through the payments options most relevant to them. A German shopper won’t see an option for iDEAL because only a Dutch shopper would be able to use it.

“When you look at the data, merchants see a boost in conversions when five, maybe six, options are presented to them at checkout,” Ready noted, adding that making a customer wade through 20 payments options when only five might be relevant for them, drags down sales. “Customers don’t want to hunt around for the method they want. Smart Payments Buttons keeps that from happening,”

Opening Merchant Options

Apart from a flood of payments options running the risk of cluttering a merchant’s page, Ready noted, trying to bring in a host of international payment methods is mostly out of the reach for small- and mid-sized merchants, given the complexity of having to support the payments workflows needed to support them.

“Having a lot of integrations with gateways leaves merchants exposed to a lot of complexities around how local payment methods work. And that complexity is pervasive through the process at signup, at checkout and with different methods that settle differently in different markets,” he said.

Managing that level of complexity can quickly spiral out of control for all but the largest merchants, which can dedicate a sufficiently large cache of resources to support this complexity. Smart Payment Buttons, Ready said, means that small merchants can offer the relevant breadth of options by shifting the complexity of managing those systems to PayPal. All that’s required of the merchant is to change a static PayPal button into a block of JavaScript.

He explained, “What this does is let the merchant — no matter what their size — literally hit a checkbox that then opens up their business to all of these international payment methods without making any changes to their checkout.”

From there, the merchant gets to go back to doing what they are presumably in business to do: provide a better experience for their customer so they will want to buy more.

Building A Smarter Shopping Experience

While the transactional elements of PayPal’s checkout product are primary, PayPal’s new checkout experience isn’t just primed around making the buttons smart, but helping the merchants build a smarter shopping experience all around. Part of that, Ready noted, is built into the new Shopper Insights tool at checkout, which gives PayPal’s merchant customers both aggregated and anonymous views of information about how shoppers visiting their site behave, as well as a series of recommendations.

He said, “We can share information with them to help them understand what might be common among consumers who are coming [to] their sight and not converting. Once we help them understand that, we can also give them ideas on how to offer tailored incentives to help turn those shoppers into buyers.”

That, he noted, is better than the somewhat “scattershot method” retailers have been known to employ. But more importantly, by giving merchants the opportunity to use One Touch as a tool to enroll customers in their loyalty or shopper program, they have an opportunity to offer merchants a much more elegant way to access their customers.

“No one likes that sign-up page that pops up when you first visit a new sight,” Ready told Webster. “Merchants know customer hate it, but they are willing to introduce that friction because that is how valuable those repeat and loyalty member customers are to them. They know this could cost them sales, and it is a trade-off they are willing to make.”

But it’s not a trade-off they should have to make, Ready noted, since One Touch already has all the necessary data about the consumer to enroll them into the loyalty program — if they wish to be.

“From the consumer perspective, they are still fully in control as to whether they want to join or not, but now we can offer them a seamless flow when they are checking out with a merchant, to just click a box and say yes, they want to join the loyalty program,” he said.

Consumers often want to join the program, Ready noted, but they just don’t want to do a lot of annoying extra work on the way there. Ultimately, he noted, that’s how PayPal wants to take on the fight with friction: find the uses customers and merchants are already signaling they need, then provide them an easier way to do it. It’s the philosophy that motivated the design of the Venmo debit card, launched earlier this week. That, among other features, allows users to divide their payments with other Venmo users at the point-of-sale (POS) when the card is swiped.

“We know that is how users are using Venmo — to split up tabs in restaurants and bars — and so we can now make dividing that tab as easy as a swipe and a few quick taps in succession,” Ready said.

He added, it is what is continuing to guide the development of the PayPal checkout process.

Ready concluded, “We don’t want to tell either consumers are merchants what choice they should make. We want to present them with all the options that are most relevant to them or their customers, and be able to make the decisions that are right for their business.”

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More