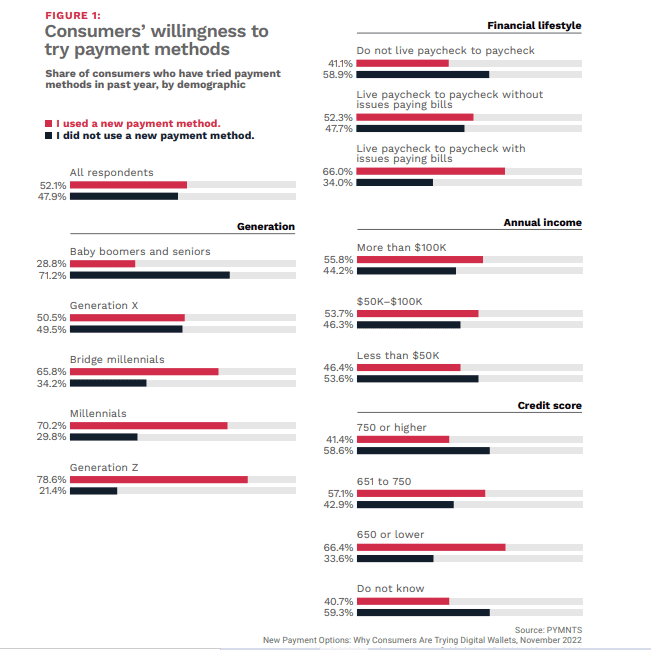

This at a time when new findings in the report “New Payment Options: Why Consumers are Trying Digital Wallets,” done in collaboration between PYMNTS and Nuvei found that 52% of consumers, overall, tried a new payment option last year.

The data shows that digital wallets are the key beneficiaries here, where 59% of consumers adopting new payment methods pivoted to this option. Drill down a bit, and we see that nearly 53% have embraced credit, debit or store cards and another 11% of respondents have given BNPL a shot.

Drill down a bit more and it becomes apparent that the consumers most firmly entrenched in the paycheck-to-paycheck economy — which represents more than 60% of us here in the United States — are the ones utilizing BNPL and cards. We found that more than half of respondents making less than $100,000 use those payment conduits, and 11% use BNPL.

A significant majority of individuals with credit scores of 650 or lower — more than 66% of them — used new payment methods, by far the highest percentage of any cohort we studied. There’s an awareness that bringing new cards and BNPL into the individual’s “toolbox” to deal with everyday financial life can help stretched consumers juggle it all. The report shows 66% of consumers living paycheck to paycheck with issues paying their bills tried a new payment method.

More Than Just Easy to Use

Advertisement: Scroll to Continue

Digital wallets and other mobile means of loading and using new payment options are prized for their ease of use (cited by 47% of respondents), but new payment choices are also being considered and embraced for financial reasons. Now, perhaps more than ever, people are cognizant of their financial health and that creditworthiness is a key component of financial health.

For forward-thinking providers, as the great digital shift continues, there’s the opportunity to help those with subprime credit ratings, or so-called “thin” credit files, build and improve their creditworthiness with a range of alternative data sources and payment options.

As we’ve noted, in just one example, Bond Financial Technologies CEO Roy Ng said earlier this year that it had brought its Credit Builder Card solutions to market to help enterprise clients launch their own branded cards. The card functions as a bank account with its own routing number — and as consumers pay down their balances each month, they build their credit while the security deposit earns interest.

“The market is still pretty early around this credit building capability,” Ng told Karen Webster in an interview. The greenfield opportunity is a considerable one: There are hundreds of millions of unsecured cards in circulation in the U.S., but only a few million secured cards. The cards are targeted at subprime consumers — with credit scores between 580 to 669, which includes 40% of millennials — or who may have thin credit files.

Just this week Intuit said it would acquire SeedFi, the partner behind Credit Karma’s Credit Builder, which offers a line of credit and secured savings account enabling members to increase their credit as they save money at the same time.

And elsewhere, as reported in September, credit reporting agency Experian is launching a new tool that can help people who pay rent contribute qualifying, “positive” residential rent payments directly to benefit their Experian credit file. The agency has estimated that 66% of consumers will see an instant increase in their FICO Score 8 if resident rental payments are reported through Experian Boost. As noted by PYMNTS in reporting over the summer, FinTechs and others are stepping in with digital payments tools to make modern renting seamless, even offering discounts. FinTech Rentdrop released its new mobile app for digital rent payments, paying with cards or through ACH methods.