Payments choice is a proving a key driver of digital commerce, as consumers form bonds of familiarity, loyalty and rewards from favoring different payment types for various transactions.

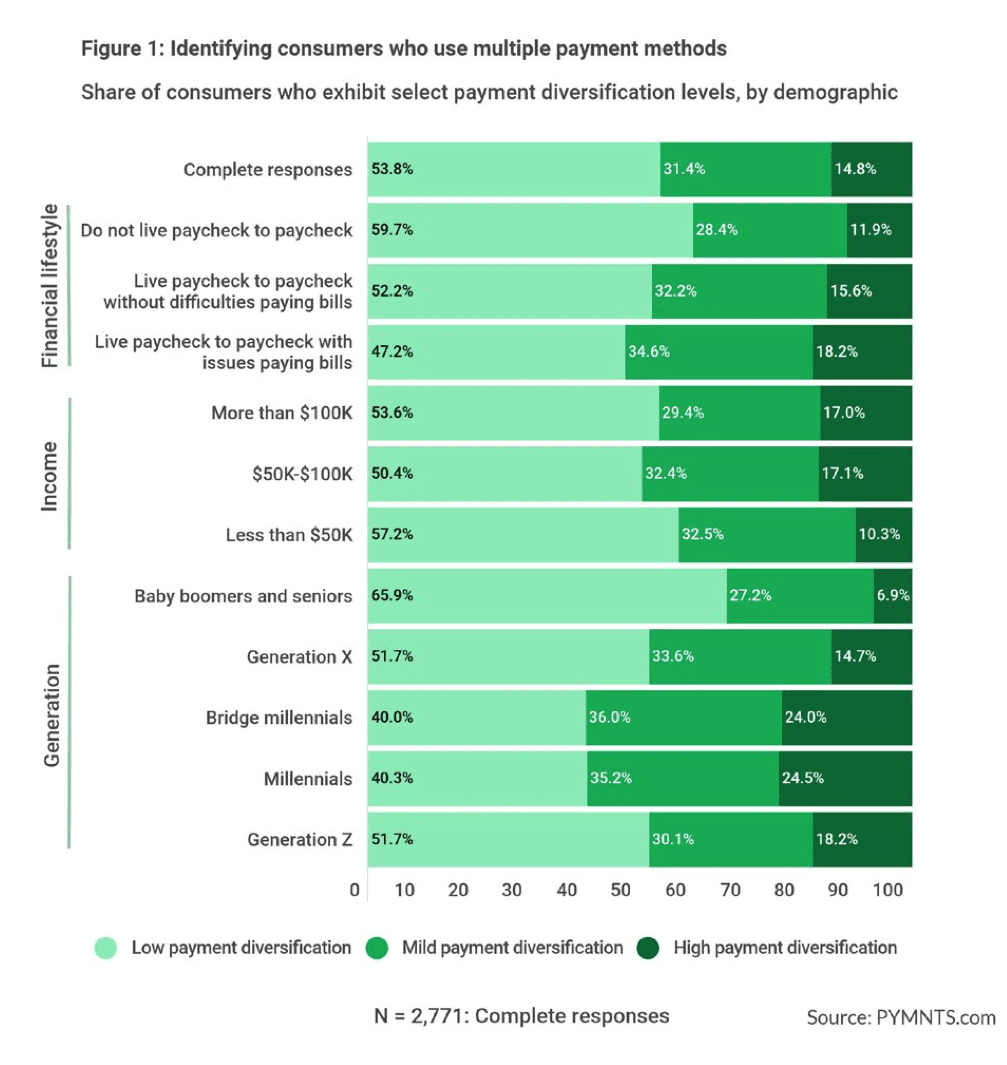

In the June edition of PYMNTS’ study series Digital Economy Payments: How Consumers Pay In The Digital World – Payment Method Diversification, we divided consumers into three groups — high payment diversification (HPD), mild payment diversification (MPD) and low payment diversification (LPD). Each has unique attributes, and each prioritizes payments diversification differently, informed by a range of factors from age to income and lifestyle.

See it now: Digital Economy Payments: How Consumers Pay In The Digital World – Payment Method Diversification

Those exhibiting high payments diversification (HPD) are typically younger, higher earning cohorts like millennials and slightly older bridge millennials. These demographic groups remain at the vanguard of early adopters as regards usage of different payment methods.

Per the June study, “a consumer’s age and financial lifestyle are the strongest factors influencing their level of payment method diversification. After the 25% of millennials who exhibit HPD, Generation Z members (at 18%) and Generation X consumers (at 15%) have the next highest concentration of HPD consumers. Just 6.9% of baby boomers and seniors have high payment diversification.”

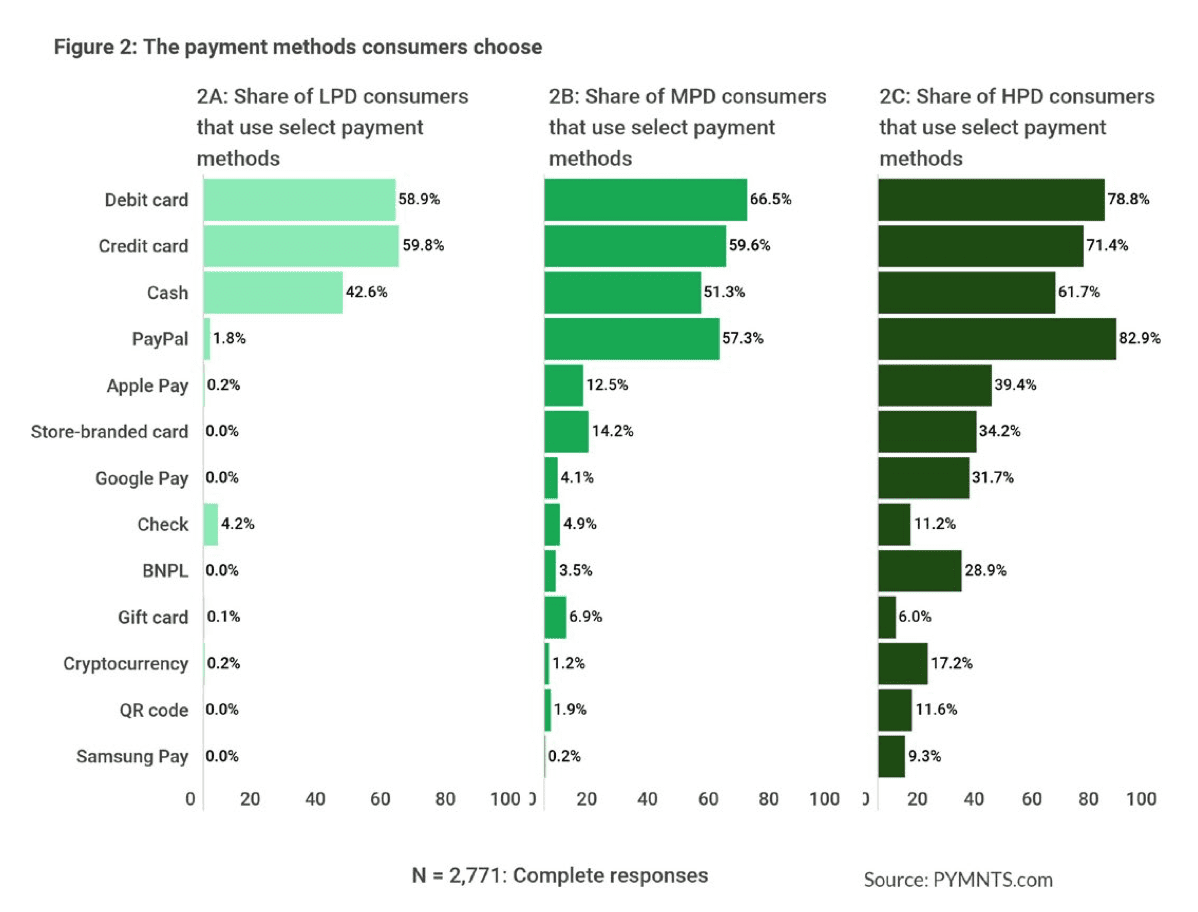

We found that HPD consumers use an average of 4.8 payment methods, the MPD group uses 2.9, and the LPD category employs just 1.7 payment methods on average. Among the highly diversified group, PayPal is the most ubiquitous, although there’s plenty of competition.

“HPD consumers tend to use traditional payment methods, just as less-diversified consumers do: 79% use debit cards, 71% use credit cards and 62% use cash,” the study states, adding that “HPD consumers also favor more innovative methods that have come to the fore during the digital payments era, and PayPal is simply the most popular of this group,” with 39% using Apple Pay, 32% using Google Pay and 29% using buy now, pay later (BNPL) financing.

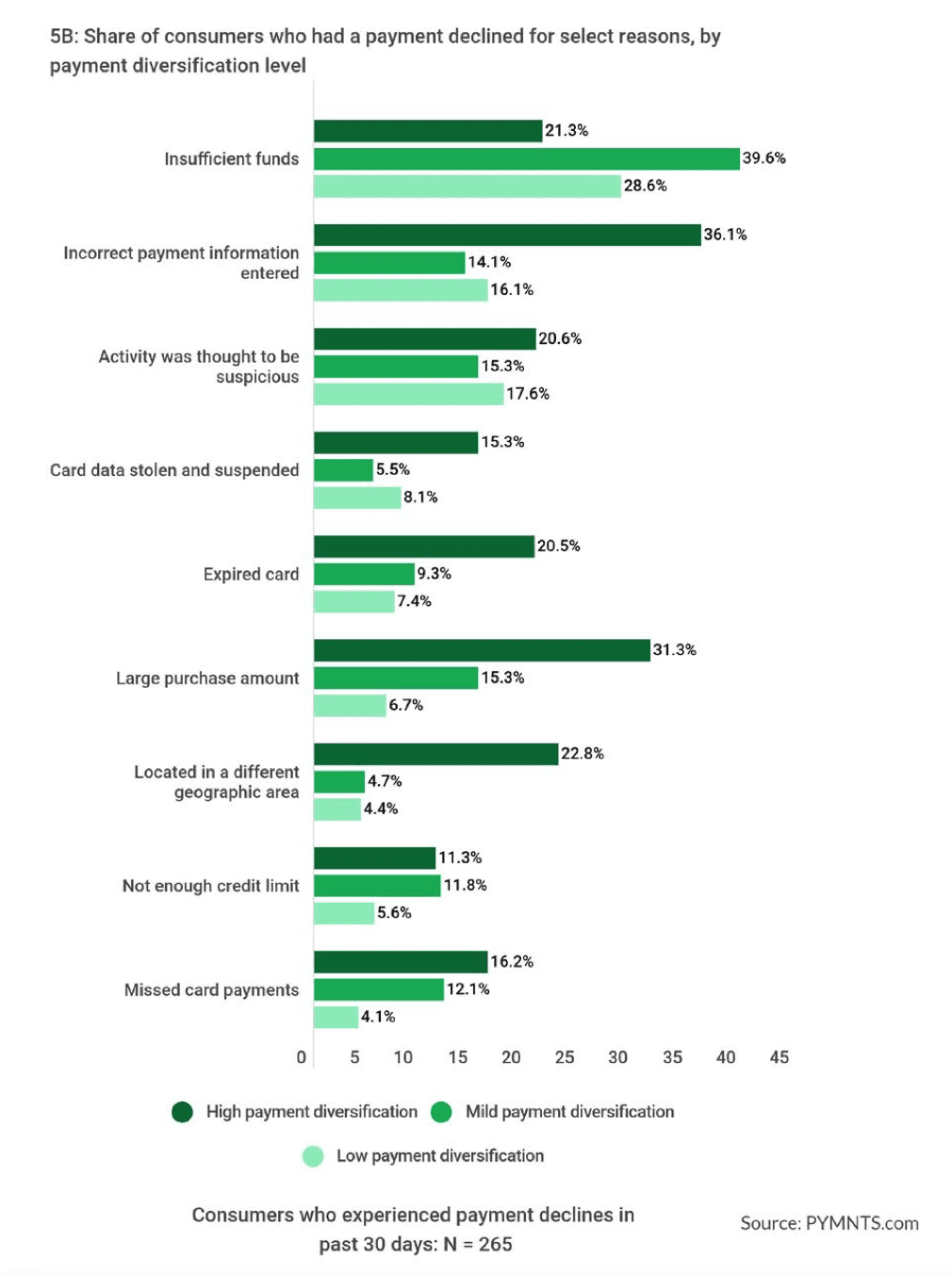

There are tradeoffs to using more payment methods as each one creates more surface area for fraudsters to conduct their illicit attacks across, resulting in double-digit fraud for some.

In the June edition, data shows the risk HPD consumers take on, which while scary and financially harmful isn’t enough to discourage this adventurous group from trying cool new ways to pay. We found that 21% of HPD consumers experienced a payment decline in the past 30 days, and 13% were victims of fraud.

This has less to do with funds for this group, with most declines the result of information entered incorrectly at checkout flagging a transaction, according to the latest data.

Get your copy: Digital Economy Payments: How Consumers Pay In The Digital World – Payment Method Diversification