Despite the growing interest in digital payment methods, the adoption of pay by bank remains surprisingly low. A PYMNTS Intelligence report, “What Consumers Need for Pay by Bank to Catch On,” done in collaboration with Trustly, looks at the barriers to adoption and what payment providers can do to educate more consumers about pay by bank.

Several key barriers contribute to the low adoption rates of pay by bank among consumers. A significant factor is the lack of awareness about the payment method itself. Many consumers are simply unfamiliar with how pay by bank works and its potential benefits. Approximately 56% of consumers are unaware of this payment option, according to the report, underscoring the need for more effective education and outreach efforts.

Concerns about security and the complexity of the payment process remain significant barriers to the adoption of pay by bank. Despite its design to enhance security, many consumers perceive traditional payment methods as safer, with only 32% expressing confidence in pay-by-bank transactions. Additionally, the nature of changing established payment habits, particularly for those used to credit or debit cards, illustrates the need for providers to simplify the user experience and effectively communicate the benefits of pay by bank to build trust and encourage broader acceptance.

While discussions around pay by bank focus on retail transactions, the report shows a growing consumer interest in applying this payment method to non-retail scenarios. For instance, 41% of current pay-by-bank users expressed interest in using this payment option for ridesharing services. This trend is particularly relevant among millennials, with 39% indicating interest in using pay by bank for such services. This presents a potential growth area for providers seeking to expand the use of pay by bank beyond traditional retail applications.

Additionally, the report highlights how the effectiveness of discounts varies by transaction type. Consumers offered significant discounts for retail purchases are 36% more likely to adopt pay by bank compared to those presented with lower discounts. Non-retail transactions can benefit from discounts of any size, suggesting that incentive strategies should be tailored based on the specific context of the transaction.

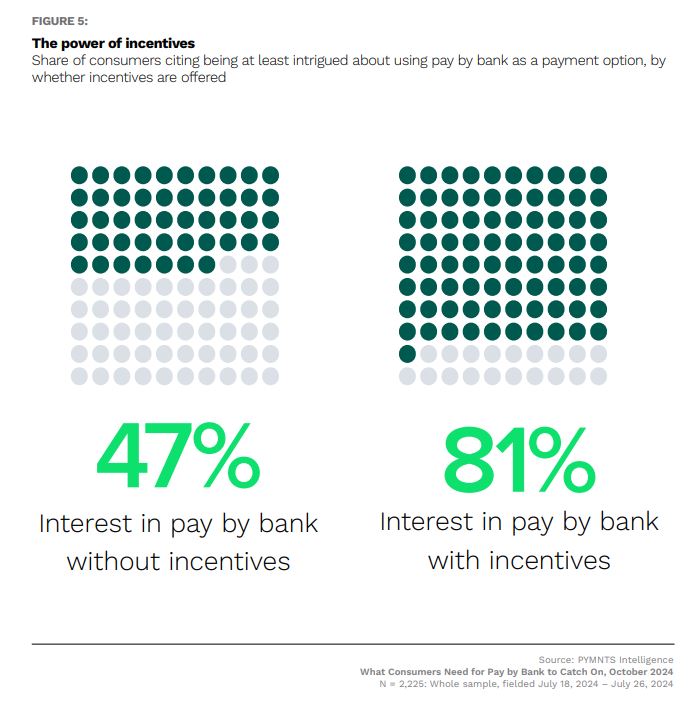

One of the most significant findings in the report is the role of incentives in enhancing consumer interest in pay by bank. When presented with cash-back discounts or loyalty rewards, consumer interest increases dramatically, with a reported 72% surge in willingness to consider the payment option. Notably, 81% of consumers express at least some interest in pay by bank when informed about potential rewards.

Among the various incentives, cash-back offers stand out. Nearly 60% of consumers said these financial incentives would increase their interest in adopting pay by bank. In contrast, only 32% stated that enhanced fraud prevention measures would similarly influence their willingness to adopt the method. This disparity suggests that providers should prioritize attractive financial incentives over security-focused messaging to better capture consumer attention.

To increase adoption of pay by bank, payment providers must overcome awareness barriers and target younger, higher-income demographics. By providing appealing incentives and broadening use cases beyond retail, they can create greater acceptance. Clear communication of benefits and heightened awareness will be crucial in transforming consumer hesitance into engagement.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More