One of the main advantages of A2A payments lies in their simplicity. Users are not required to share sensitive financial information, such as credit card numbers, reducing the risk of fraud, according to findings detailed in “Tracking the Digital Payments Takeover: Consumer Familiarity Controls Account-to-Account Payment Growth,” a PYMNTS Intelligence and AWS collaboration.

“With pay-by-bank transactions, you don’t have to hold a customer’s [card] information,” Chris Jameson, managing director and head of GTS product management EMEA at Bank of America, explained further in an interview with PYMNTS last year. Jameson added that A2A payments offer a dual benefit: it eliminates the necessity of storing consumer data and reduces the costs and liabilities associated with safeguarding card information, a boon applicable to both card acquirers and issuers.

Additionally, A2A payments are typically processed in real time, enabling merchants to receive funds immediately. This leads to improved cash flow and a reduced risk of bad debt. Moreover, A2A payments have the potential to enhance customer engagement, with merchants offering discounts or rewards for their use, or utilizing them to streamline online checkouts.

But while this payment method continues to gain popularity, with 36% of consumers using them in the past quarter, they have yet to fully disrupt the wider payments landscape.

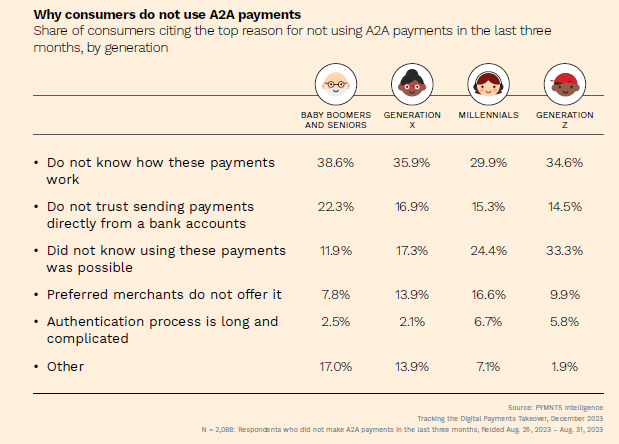

The primary barrier hindering wider acceptance of A2A payments stems from a lack of comprehension regarding its mechanics. Notably, over half of the consumers surveyed admitted to not using A2A options due to their limited knowledge. Additionally, 36% of consumers admitted to having no grasp of how A2A payments function, while 24% weren’t even aware of the existence of this payment method.

Advertisement: Scroll to Continue

The survey also highlighted a generational divide in the inclination towards A2A payments. Baby boomers and seniors exhibited the least interest, with 38.6% admitting to their lack of understanding regarding these payments. Conversely, millennials displayed a more open attitude towards adopting A2A payments, with over half of them having utilized this method in the past 90 days.

To encourage broader adoption of A2A payments, targeted awareness campaigns and educational efforts are crucial in addressing the knowledge gap among consumers, the report noted. Incentives such as discounts, rewards and exclusive offers could also play a significant role in driving adoption, as the survey revealed that 41% of non-users expressed willingness to switch if provided with such incentives.

Ultimately, despite the numerous advantages A2A payments present over traditional transaction methods, their widespread adoption faces obstacles due to a lack of comprehension and differences in generational awareness.

Looking ahead, addressing these barriers through education and incentives is crucial for A2A payment platforms to drive broader use and expand their market reach. Collaborative efforts among stakeholders will also be pivotal in bridging the knowledge gap, ensuring that all generations can embrace and capitalize on the convenience and security offered by A2A payments.