Businesses have long been phasing out manual processes in favor of digital systems that improve efficiency, deepen relationships with suppliers and better serve customers. The trend gained new focus during the pandemic when businesses throughout the United States economy needed to upgrade their payment platforms rapidly.

Businesses have been relying predominantly on payment methods like credit and debit cards. However, spending plans clearly show that the most forward-thinking businesses are prepared to invest in innovative payment technology to ensure they can effectively transact with customers and suppliers. For example, 37% of finance and insurance businesses have already adopted ePayables with virtual cards, which more efficiently link the accounts payable (AP) process with enterprise resource planning systems, and another 39% are planning to invest in this method.

Businesses have been relying predominantly on payment methods like credit and debit cards. However, spending plans clearly show that the most forward-thinking businesses are prepared to invest in innovative payment technology to ensure they can effectively transact with customers and suppliers. For example, 37% of finance and insurance businesses have already adopted ePayables with virtual cards, which more efficiently link the accounts payable (AP) process with enterprise resource planning systems, and another 39% are planning to invest in this method.

In “Digital Payments: Expanding the Payments Palette,” a PYMNTS and Corcentric collaboration, we survey 250 CFOs from healthcare companies and finance and insurance firms to assess where they have invested over the last three years and the factors that are influencing their future technology budget priorities.

Some of our key findings include the following:

• Businesses are supporting an increasing number of payment methods to remain competitive.

Healthcare companies and finance and insurance firms now support an average of nearly six different payment methods. Not only do businesses need to support the payment methods their customers currently use, but they also need to prepare for the next wave of innovative payment options. Tried-and-true methods still dominate, but businesses are working on adopting new, innovative methods.

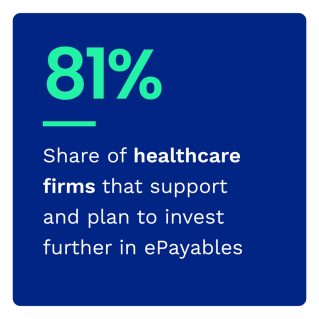

• Companies are doubling down on and expanding their investments in payment technology.

The most forward-looking businesses are not content to rest on their heels but continue building up their payment infrastructure. For example, we found that 81% of healthcare companies and 92% of finance and insurance companies that have already adopted ePayables are making additional investments in the technology.

• Retaining existing customers and attracting new consumers requires implementing additional payment options.

• Retaining existing customers and attracting new consumers requires implementing additional payment options.

CFOs in the healthcare, finance and insurance spaces recognize the demand for payment choice. Automating the formerly manual processes and adopting cutting-edge payment methods is important, and so is making sure your business offers a robust set of payment solutions and has up-to-date payment technology. Among the companies that have not yet invested in real-time payments, we found that 92% of healthcare companies and 86% of finance and insurance businesses plan to spend on the necessary systems and software.

Our increasingly digital economy demands that companies strategically invest in the right digital payment technologies to retain existing customers and expand their customer base.

To learn more about CFOs’ payment technology investment priorities, download the report.