This week, an official with the Financial Conduct Authority (FCA), an agency tasked with overseeing firms and markets in the U.K., compared her job to that of a juggler.

“Juggling is, at least metaphorically, a skill we regulators have to master,” said Sarah Pritchard, executive director, markets and international for the FCA. “Whether it is balancing the demands of consumers, markets or firms.”

Pritchard shared her analogy with attendees of TheCityUK International Conference 2024, an event that brought together industry leaders, policymakers and regulators from across the United Kingdom.

Included in the list of things she and her FCA colleagues must juggle, she said, is the need to encourage competition, advance operational objectives, support new technology and promote “responsible innovation”— all whole working to protect consumers and markets.

That’s a lot of juggling — and it might explain why the roster publications available on the FCA’s website include directives about borrowing, mortgage protections, social media standards, auto loans, insurance distributions, crypto assets, corporate sustainability requirements and more.

In other words, regulators in the U.K. — just like regulators in the U.S., Spain, Australia, and other countries — have a lot on their plate.

Consider just what one U.S. agency, the Consumer Financial Protection Bureau (CFPB), must monitor: banks, thrifts, credit unions, non-depository mortgage originators and servicers; payday lenders; consumer reporting; debt collection; international money transfers, automobile financing and more.

This extensive jurisdiction explains why the CFPB is now considering actions on online gaming, student loans, title insurance, credit card reward points and late fees, to name just a few.

None of this is to suggest that the FCA, the CFPB or any of the other industry watchdog isn’t doing important work. However, it’s worth remembering that when any industry practice — questionable or otherwise — captures the attention of regulators, it can lead to greater uncertainty for those industries. And as PYMNTS Intelligence recently found, uncertainty can cost businesses, especially smaller ones, millions.

In fact, according to CFOs surveyed for “The 2024 Certainty Project Report,” middle-market companies stand to lose roughly $20 million on average due to uncertainty and — and regulatory compliance is a major contributor to those losses.

“The 2024 Certainty Project Report” — which draws from surveys we conducted with 60 chief financial officers (CFOs) of companies that had annual revenues between $100 million and $1 billion last year, and which will spotlight other decision-makers in future editions — zeroed in the toll uncertainty takes on middle-market companies.

A reason for this focus: we found larger companies operate with a greater sense of certainty. CFOs at larger middle-market firms tell PYMNTS Intelligence that they have the resources needed to navigate market ups and downs, which is why 57% say they operate with high levels of certainty.

But smaller middle-market companies have to perform a far more demanding highwire act when negotiating uncertainty. Forty-seven percent of CFOs from smaller firms deal with considerable uncertainty, which is more than double the 21% faced by CFOs operating in the largest revenue bracket studied: $750 million to $1 billion. Overall, middle-market companies lose about 4.4% of their annual revenues due to uncertainty.

Over a 12-month period, smaller companies lose, on average, $21 million due to uncertainty, according to the CFOs we surveyed.

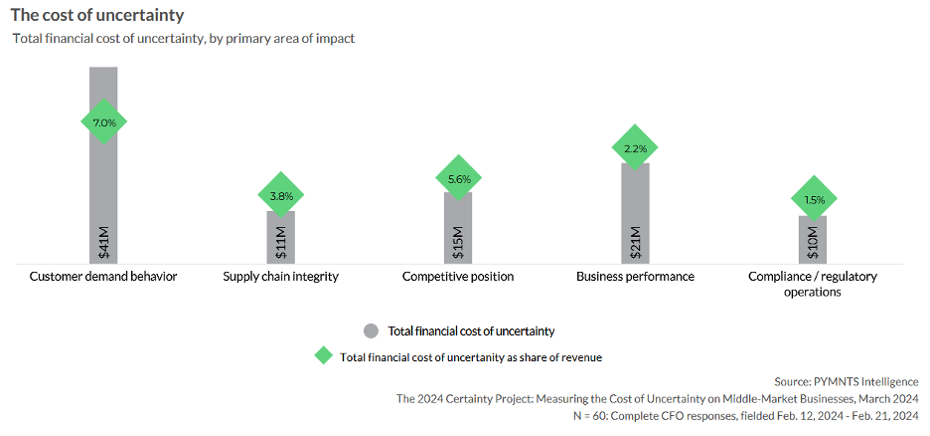

As the accompanying graphic illustrates, these CFOs cite a variety of factors that drove uncertainty in the last 12 months. For middle-market firms that identified shifting customer demand behavior as the primary driver of uncertainty, uncertainty cost 7% of revenue: approximately $41 million. If uncertain business performance was the lead issue, $21 million was lost on average.

And when compliance and regulatory uncertainty was the top issue, middle-market CFOs said uncertainty cost them $10 million on average.

While no one is denying regulators have a lot of plates in the air as they work to manage the many industries and organizations placed under their jurisdiction, it’s worth remembering that middle-markets firms are also performing juggling acts as they work to stay afloat. Keeping pace with changing regulatory requirements can make it even tougher to find the right kind of balance.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More