Building a trusted relationship with retail customers is the easiest way to ensure a healthy and dedicated business connection. Simply put, when businesses offer an array of payment options, including lease-to-own programs, brand affinity increases.

This according to a survey of over 2,200 consumers for the Finding Retail’s Invisibles: Leveraging Flexible Digital Payments To Reach Underserved Durable Goods Customers, a PYMNTS and Katapult collaboration, that show 75% of U.S. consumers who use a lease-to-own option said it was the only way they could afford to buy durable goods.

Read more: New Study Finds Strong Demand for Lease-to-Own Options Amid the BNPL Boom

In total, an estimated 79 million American consumers are unable to purchase durable, big-ticket items like furniture, appliances or tires without being given credit lines or other flexible payment options. The so-called “retail invisibles” are typically consumers with financial challenges that prefer to use 100% financing rather than cash as a way to acquire durable goods.

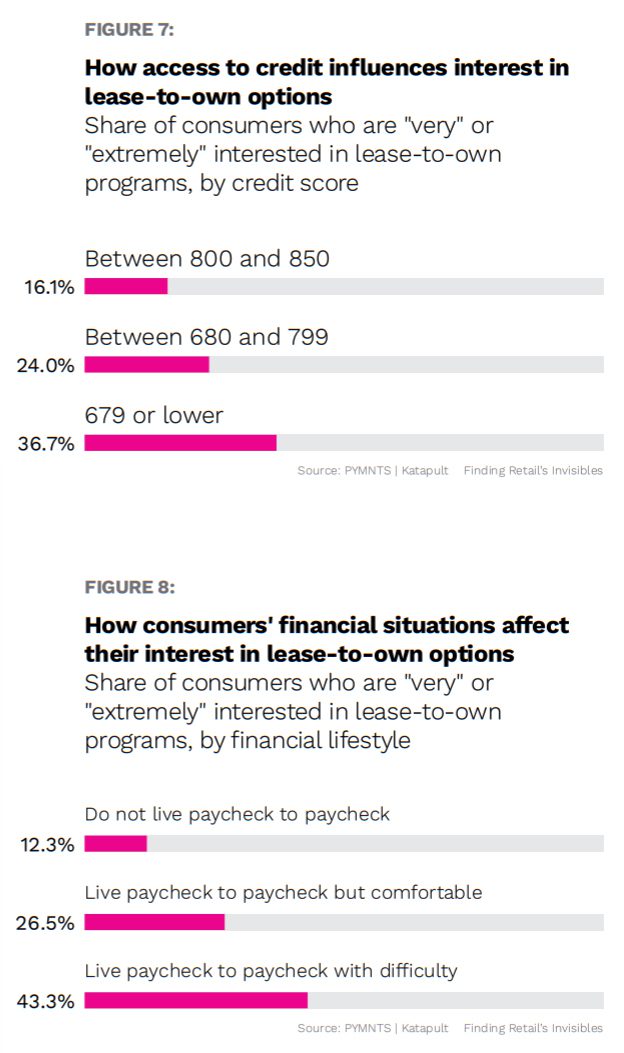

Lease-to-ownprograms help those with significant financial pressure or credit score challenges to obtain items they need immediately. In fact, 43% of consumers who live paycheck to paycheck are “very” or “extremely” interested in lease-to-own programs, while 37% of those with lower credit scores (679 FICO and below) were likely to do the same.

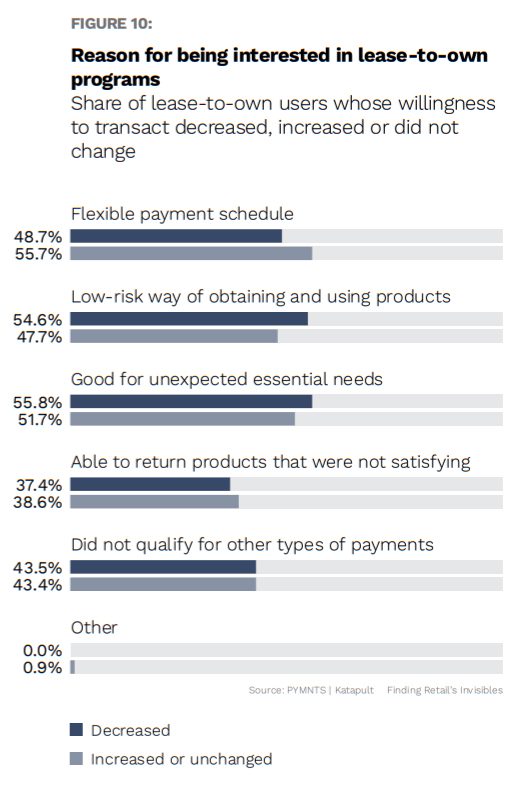

In addition to higher approval rates than traditional loans or buy now, pay later (BNPL) plans, the survey found that lease-to-own users most often cited the ability to make essential but unexpected purchases, the low-risk way of obtaining and using products, and the flexible payment schedule as leading factors that drove the use of lease-to-own programs.

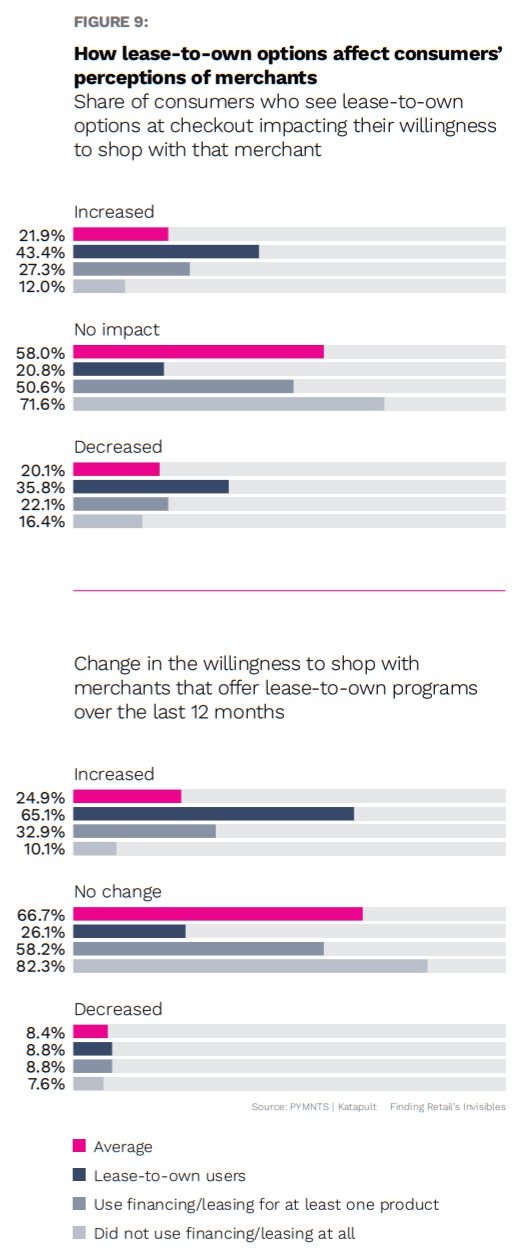

Providing lease-to-own options also affects consumer perceptions of merchants, as 22% of respondents said their willingness to shop was higher when merchants offered the plans, and 25% of consumers said their willingness to shop with these merchants had increased over the last 12 months.

Additionally, respondents who already tried lease-to-own programs had a much better perception than the full sample group, as 43% of those who used lease-to-own options saw their willingness to use them increase, and 65% said their willingness to use them had risen over the past 12 months.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More