The rise in stretched consumers has seen more banks and FinTechs looking to help them.

With weakened consumer buying power, a major theme of 2022, banks and FinTechs are increasingly investing in new ways to help so-called “cusp consumers” boost their credit scores and improve overall financial wellness with the help of programs that support — and report — responsible repayment behavior.

The latest example coming just last week (Dec 1) via news that Intuit — the parent company of Credit Karma — is buying fintech SeedFi is the latest in a series of announcements in recent weeks and months around shoring up consumer financial health in the face of a financial crisis that’s put a hurt on credit and savings.

On Dec. 2, consultancy Zventus announced the release of its FinTech-in-a-box solution to help legacy lenders create consumer lending products that better compete with those of nimbler FinTechs, expanding to the pool of consumer lending options.

In a press release, Zventus president Angel Alban said, “With so many challenges in today’s market, lender transformation is essential. Our FinTech-in-a-Box solution makes that transformation much more manageable, providing access to specialized skills that will drive innovation and growth in the mortgage and lending sectors.”

At the same time, Austin-based fintech StellarFi, which came out of stealth in the summer and is ramping up its offering for 2023, is partnering with TransUnion, Experian and Equifax to record timely bill payments on consumer credit reports to build FICO scores.

StellarFi’s model is to have consumers link bank accounts through its platform, recording each on-time paid bill which helps build scores.

In a November announcement that the startup had exceeded $1 million in annual recurring revenue, Lamine Zarrad, StellarFi founder and CEO said, “StellarFi offers versatility in credit-building payment options. On top of household bills, StellarFi members also have paid bills such as child support, medical co-pays, and Tesla Supercharger memberships to build credit. The opportunity to build credit through StellarFi is massive.”

Credit Rehab is Hot

To be sure, the commercial interest in credit rehab is hot right now as institutions look for new ways to respond to a changing economic environment that reflects the prospect of crimped borrowing demand due to rising interest rates.

With 61% of U.S. households, including six-figure earners living paycheck-to-paycheck, the push to help consumers regain lost spending power is likely to be long and arduous.

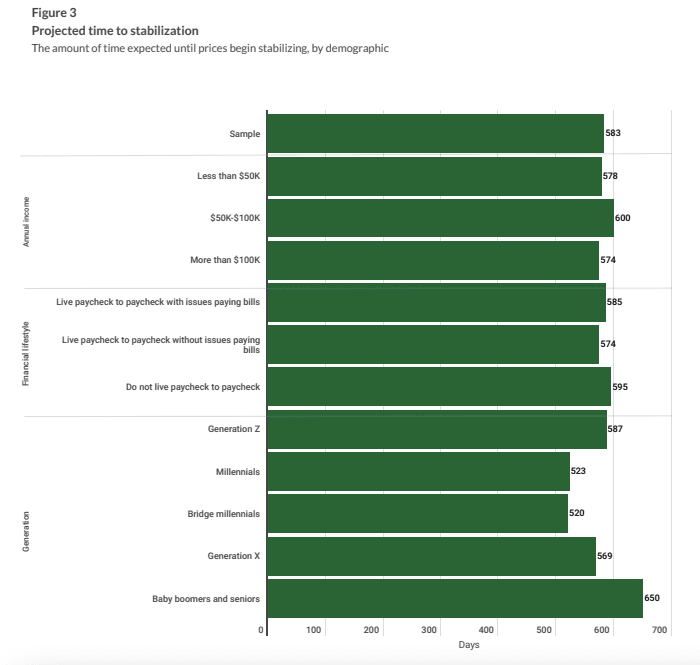

According to PYMNTS’ new report Consumer Inflation Sentiment: In It For The Long Haul, “The majority of consumers agree that we are only halfway through this high inflationary period. Overall, consumers think inflation will return to normal levels by June 2024, or about 20 months from now. Again, millennials are the most optimistic generational cohort, believing inflation will normalize by April 2024, four months sooner than baby boomers and seniors on average.”

Get Your Copy: Consumer Inflation Sentiment: In It For The Long Haul

While banks and FinTechs have their own business incentives to help bring more consumers to the table, the present reality of inflation has shown that 40% of consumers will finance their holiday shopping and millions more will sit it out altogether. It’s a reality that has raised the importance of growing the pool of creditworthy customers who have – and qualify for – buying power to ensure their seasonal retail spending can proceed.

For all PYMNTS retail coverage, subscribe to the daily Retail Newsletter.

We’re always on the lookout for opportunities to partner with innovators and disruptors.

Learn More