Cash equivalents came on strong in the closely watched Cyber Five weekend that ended Monday (Nov. 28).

Faced with staggering inflation that pushed paycheck-to-paycheck households to the breaking point, consumers held back and then pounced on deals during the annual holiday sales event.

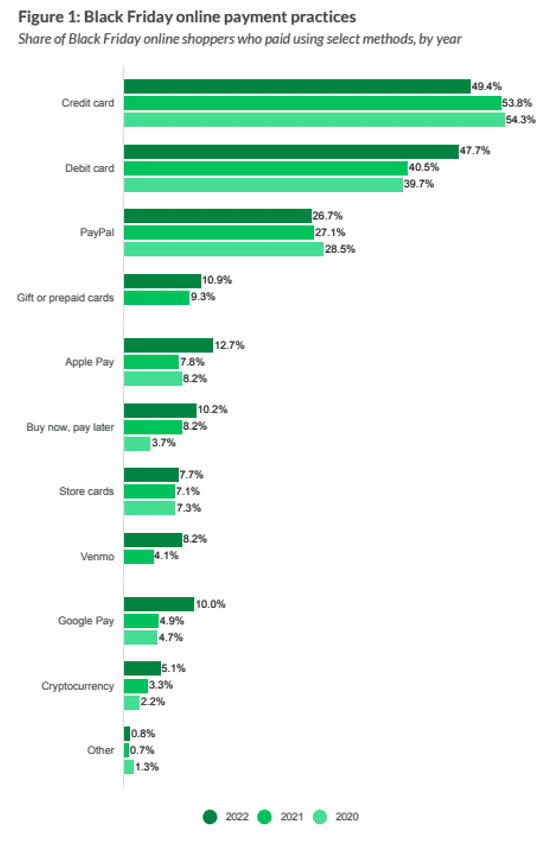

Importantly, while not off the table given the high use of credit cards and buy now, pay later (BNPL) installment plans, consumers increasingly used digital cash equivalents, like eWallets from Apple Pay and Google Pay, as well as debit cards and Venmo to avoid taking on debt in a shaky economy.

PYMNTS surveyed nearly 3,100 consumers Friday (Nov. 25) and Saturday (Nov. 26) for the report “Black Friday 2022: High Prices Reshape Holiday Shopping Habits” which found that 13% of shoppers paid with Apple Pay over the big seasonal kick-off weekend, up from 7.8% last year.

At the same time, the report noted that 10% of online shoppers paid via Google Pay, and 8.2% paid via Venmo, reflecting a doubling of the share these payment methods garnered just one year ago.

Advertisement: Scroll to Continue

In addition, the new survey found that all-time highs were also set for both BNPL and cryptocurrency use, which reached 10% and 5.1%, respectively, this year.

With the use of debit cards and cash alternatives like Apple Pay, Google Pay and Venmo showing 60% to 100% year-over-year share growth, consumer choice was tantamount to decisioning this year, where the data showed that one in three shoppers who wanted to buy something said they elected not to do so.

Price Watching

The trends were clear, as eCommerce sites and shopping platforms saw shoppers sit and wait for the right deal.

Jonathan Friedman, CEO of artificial intelligence (AI)-bargain hunting site Karma told PYMNTS that its roughly 4 million members were showing great patience this year, loading up online shopping carts then watching and waiting for prices to fall.

“There [was] a 78% increase in items saved in shoppers’ carts on Karma ahead of Black Friday, a strong indication that shoppers [were] biding their time and waiting for their items to go on sale before purchasing,” Friedman said in an email to PYMNTS.

“Shoppers want to be in control of when they buy and how they make their payments,” he added, noting the increased demand for convenience tools such as AI-based search, simplified coupon use, embedded payments and one-click checkout show consumers are also responding to convenience.

“Choices and patience are key for shoppers this holiday,” Friedman said.

See also: Shoppers Go Deep on BNPL and eCommerce as Holiday Shopping Ramps Up

Year of the Sales Events

As Cyber Five totals trickle out this week, widely published estimates place Cyber Monday ahead of Black Friday this year by more than $2 billion ($11.2 billion versus $9.1 billion) as consumers swarmed online looking for even deeper discounts than those that have been a fixture of all year.

Amazon double dipped with Prime Day in July and the Prime Early Access sale in October, while Walmart, Target and a host of other retailers did the same, blowing out excess 2021 inventory by slashing prices and appealing to inflation-flattened shoppers who were not buying.

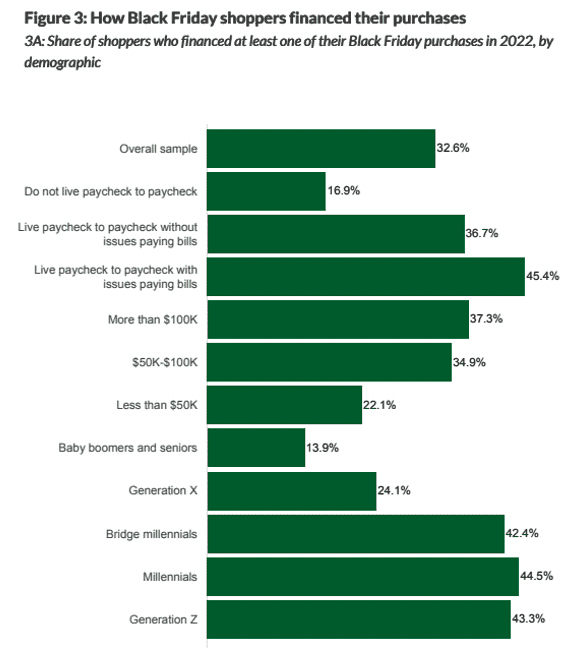

Even given the penchant for cash equivalents and the high number of paycheck-to-paycheck households struggling this year, many turned to financing their buys anyway.

“Consumers living paycheck to paycheck with issues paying their bills were the most likely to take out loans, extend their credit lines or opt for BNPL options to finance their Black Friday purchases,” the PYMNTS study found. “Forty-five percent of this group used one of these financing options to fuel their Black Friday shopping sprees — and on average, they used these methods to finance 58% of their purchases.”

For all PYMNTS retail coverage, subscribe to the daily Retail Newsletter.